Dear Senators,

Submission to the Senate Inquiry into various aspects of:

Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 and Income Tax Rates Amendment (Tax Reform No. 1) Bill 2026

is submitted by Barbara Smith AM, Dr Ed Koken and Dr Brett Davies

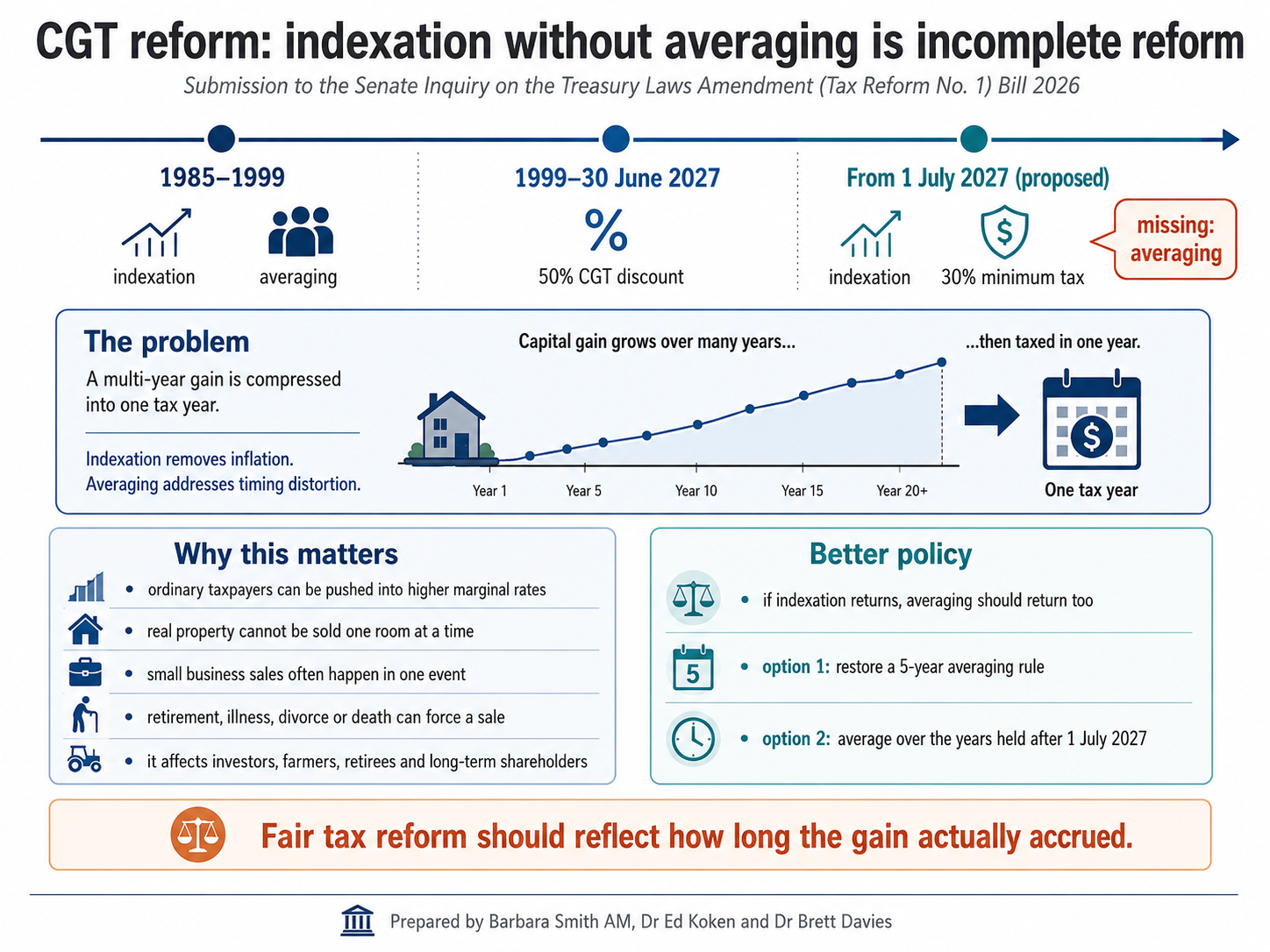

CGT discount and pre-CGT exemption replaced by indexation and minimum tax rate

Start date: 1 July 2027

The pre 1999 choice of indexing or 5-year averaging rules

In 1985, based on equity grounds, it was argued that ‘because real capital gains represent an increase in purchasing power similar to real increases in wages, salaries, interest or dividends, they should be included in any comprehensive definition of income’ (Australian Government 1985, page 77).

The capital gains tax arrangements introduced in 1985 applied to realised gains and losses on assets acquired after 19 September 1985. From 1985 to 1999, an indexation system was applied, so that only real, and not nominal, gains were taxed. An averaging system was also in place to reduce the impact of the progressive income tax on realised gains accrued over a period of years.

In 1999, a capital gains discount was introduced to reduce the tax bias towards asset retention and to make Australia’s capital gains tax internationally competitive. Indexation was frozen as at 30 September 1999. For assets acquired before 11.45 am AEST on 21 September 1999, taxpayers may still choose indexation, but only with the cost base indexed up to September 1999. The CGT discount applies to eligible assets for which the CGT event occurs after 11.45 am AEST on 21 September 1999.

The current CGT discount rules

Before the 2026-27 proposed budget changes are legislated, the existing CGT discount has enabled individuals, trusts and complying superannuation funds to reduce their net capital gain made on disposal of an asset that has been held for more than 12 months.

The standard discount rates were set at:

- 50% for trusts and individuals

- 33 1/3% discount for complying superannuation funds.

As far as the authors are aware, the rationale behind these two different discounts has never been publicly explained. The public policy rationale usually given was simply to reduce lock-in, encourage investment, and make Australia more internationally competitive. However, to the authors’ recollection — and in particular to Smith, who served as a representative for the Australian Taxpayers Association on various ATO consultative committees at the time — the explanation given was simple. When an asset has been held for more than one year, the effective discounted rate of tax on the net capital gain is equalised to 10% for both superannuation funds and individuals as follows:

- The lowest marginal tax rate for an individual with an income between $5,401 and $20,700 was 20%, and so a 50% discount reduced the effective tax rate on a capital gain to as low as 10%.

- The tax rate on complying superannuation funds is 15%, and when that is reduced by 1/3rd, the effective tax rate is also 10% on the whole of the capital gain (superannuation funds do not have a tax-free threshold).

- The full amounts of realised capital losses are deducted from realised capital gains BEFORE the discount is applied.

Trusts do not get the 50% CGT discount in their own right in the same practical way as individuals

A trust can calculate a discounted capital gain, but the benefit of the discount is only passed through to individual beneficiaries who are entitled to discount treatment. A company beneficiary, for example, does not get the CGT discount.

The proposed 2026–27 Budget CGT rules

From 1 July 2027, the Government proposes to remove the 50% CGT discount and replace it with cost-base indexation for assets held for more than 12 months. A 30% minimum tax on net capital gains is also proposed. The Budget papers state that the reform applies only to gains arising after 1 July 2027.

The proposed rules apply across asset classes, including real property and shares. They are not confined to residential property. Reuters reports that the Bill passed the House of Representatives on 4 June 2026, but still requires Senate support.

Under the proposal:

- the 50% CGT discount continues to apply to eligible gains arising before 1 July 2027;

- pre-CGT assets remain outside CGT for gains arising before 1 July 2027;

- for future gains, pre-CGT assets are effectively reset by reference to their market value just before 1 July 2027;

- indexation is calculated by reference to CPI, broadly reflecting the system that applied before 1999;

- the reforms apply to individuals, trusts and partnerships; and

- rental property investors in new residential properties may choose between the 50% CGT discount and the new indexation/minimum-tax regime.

The missing averaging rule

The major defect in the proposal is what it leaves out.

The pre-1999 CGT regime did not rely on indexation alone. It also had averaging. Averaging reduced the unfairness caused when a capital gain accrued over many years but was taxed in one income year.

The proposed 2026–27 changes revive one part of the old system — indexation — but ignore the other part — averaging. That is not a minor drafting issue. It is a structural problem.

Without averaging, a taxpayer who sells a long-held asset is taxed as though the gain was earned in the year of disposal. That is artificial. It pushes ordinary taxpayers into higher marginal tax rates for one year, even though the economic gain was built over many years.

This is the harshest for non-divisible assets. Real property is the obvious example. A person cannot sell one room each year. A small business owner cannot always sell one slice of the business each year. A long-term shareholder may also sell because of retirement, illness, divorce, death, debt, or family need. These are not tax schemes. They are life events.

Why this is unfair to ordinary Australians

The omission affects more than high-net-worth investors. It catches salary and wage earners, small business owners, rental property investors, farmers, retirees and long-term shareholders.

It is not ethically correct to say that indexation alone taxes only “real” gains. Indexation removes inflation. But without averaging, the remaining real gain is still compressed into one tax year. That can create a tax rate that does not reflect the taxpayer’s ordinary income position over the period in which the gain accrued.

One taxpayer put the concern as:

“I missed the part where the wealth I created and leave to my children is suddenly a generational problem for them and requires taxing.”

Market consequences

Early market evidence suggests the proposal is already adversely affecting investor confidence in established residential property. If that continues, weaker prices and lower transaction volumes may reduce the stability of State revenue streams, including stamp duty and land tax. Residential property markets are already cyclical. A Federal tax change that discourages investment in established property may make those cycles sharper.

Better policy

On that basis, the fairer policy outcome is this:

If the Government proceeds with indexation, it must also restore an averaging mechanism for long-term capital gains. Indexation without averaging is incomplete reform. It taxes a multi-year gain as though it were one year’s income. That is not equity. It is timing distortion and not tax reform.

-

Alternative solutions

A capital gains tax liability arises where there is a real capital gain in the value of the asset between acquisition and disposal. The acquisition price and certain expenses (the cost base) are adjusted by the rate of inflation if the taxpayer owns the asset for at least one year. An averaging system should apply to prevent an individual from being taxed on capital gains at a marginal rate higher than that applicable to their other income. Assets acquired before 20 September 1985 are subject to capital gains tax that accrues from 1 July 2027.

Before 1999, Australian law addressed this problem through the CGT 5-year averaging rules.

A practical solution is to average the taxable capital gain over five years for marginal tax rate purposes. Alternatively, the gain could be averaged over the number of years the asset was held after 1 July 2027, once the asset has been held for more than 12 months. By doing this, the tax on the capital gain is still paid in the financial year of sale, but the average marginal rate should reflect how many years the gain actually accrued.

While the 50% discount is simple, indexation with averaging is fairer. It better protects lower-income taxpayers, small business owners, rental property investors, long-term shareholders and retirees. These taxpayers may realise one large gain after years of saving, risk-taking and capital building. They should not be forced into an artificially high tax bracket merely because the capital gain is realised in one income year.

Negative gearing

Negative gearing associated with a residential rental property refers to the situation where expenses, including interest, council rates, land tax and other state government charges, real estate agent fees, repairs and other outgoings, are greater than the rental income earned from the asset. Sometimes negative gearing is intentional from the outset when a large mortgage is taken out, but other times it arises unexpectedly following interest rate rises, increases in council rates, and excessive increases in state government imposts.

With proposed tax reforms pushing individual investors and trusts toward new residential builds to access negative gearing and CGT discounts, there is a massive risk that investors will make poor decisions based purely on tax incentives and push up the prices of small new apartments that would otherwise be purchased by young people as their first home. First-home buyers may also be crowded out of smaller new apartments. Some young buyers purchase a first home, rent it out for a period, and continue living with parents while they reduce debt. They may now be competing against tax-driven investors who are pushed into the same new-build market.

As a general rule, land is the appreciating component of residential property. A physical building, however, is a depreciating asset; it suffers wear and tear, requires ongoing maintenance, and eventually becomes obsolete. Land is a finite resource, especially in desirable locations, and its value usually grows over time due to population demand, scarcity, and infrastructure development.

New builds, especially off-the-plan apartments and house-and-land packages in outer suburbs, often have a weaker land-to-asset ratio. A larger part of the price reflects the building, developer margin, marketing costs and sales commissions. The tax deductions may look attractive. The proposed rules may push investors into new builds for tax reasons, even where the underlying investment is poor.

The broader economic impact

As Geoff Wilson, Chairman of Wilson Asset Management, has warned, the proposed CGT changes are not a fairness measure. They are a tax on risk, enterprise and long-term wealth building. They punish business owners, investors and families who have saved, built and taken commercial risk. They discourage capital formation. They encourage capital to move offshore. They weaken investment, jobs and growth. Australia should not dress up class warfare as tax reform. A tax system that punishes success ultimately punishes the workers, retirees and families who depend on a strong private economy. Business leaders should not whisper about this reform. They should say plainly what it is: destructive tax policy that must be stopped before it damages investment confidence further.

Comments on the cause of the housing affordability problem

It is unlikely, as the government hopes, that these proposals will help young people get into home ownership. Part of the problem is that 12% of their gross salary and wages are forced into superannuation funds where they cannot be accessed for the next 40 or more years. Additionally, HECS debts for university courses and increasing rents — often driven by imposts from all levels of government and Reserve Bank interest rate increases — heavily constrain their cash flow. Combined with a shortage of available rental properties (partly blamed on excessive immigration), these factors make it virtually impossible for young people to save for a home deposit.

About the Authors

Barbara Smith AM

Barbara Smith AM is a tax, accounting and superannuation specialist. She holds a Master of Tax Studies from Monash Law School and a Master of Business by publication from the Phillip Institute of Technology. Her published Master of Business work led to a parliamentary inquiry and changes to tax law. Smith held a Tax Agent’s licence for 40 years, lectured in tax, financial planning and accounting for 16 years, and was Technical Director of the Australian Taxpayers Association, later Taxpayers Australia, for 10 years. She has written, or jointly written, over 30 books and manuals on tax, accounting and superannuation.

Dr Ed Koken

Dr Ed Koken is an academic, author and specialist in taxation, superannuation and financial planning. He has written and presented extensively on SMSFs, tax compliance and retirement planning. His work combines technical tax analysis with practical guidance for accountants, advisers and trustees.

Dr Brett Davies

Dr Brett Davies is a solicitor, tax lawyer and partner of Legal Consolidated Barristers & Solicitors, a national Australian law firm. He has practised as a lawyer since 1994 and has lectured in tax, superannuation, estate planning and business law since 1999. He is an Adjunct Professor of Law and regularly writes on trusts, SMSFs, estate planning, tax structuring and asset protection.

Current Joint work

Barbara Smith AM, Dr Ed Koken and Dr Brett Davies are authors of Keep it Super Simple: SMSF Essentials.