While the legislation tells us what the law is, the ATO’s internal manuals tell their auditors exactly how to enforce it.

One of the most revealing documents for tax professionals is Practice Statement Law Administration PS LA 2011/8. It is the ATO’s internal rulebook for registering entities, managing Tax File Numbers (TFNs), handling GST registrations, and tracking taxpayers.

PS LA 2011/8 contain the instructions that the ATO staff must follow.

For accountants and financial planners, correctly registering a client’s entity with the ATO is a high-risk task. It is not just an administrative form; it is the moment the client steps into the ATO’s web. A simple mistake during ABN or TFN registration can trigger an audit before the client has made their first dollar.

Here are four critical rules from the ATO’s internal manual, how your accountant navigates them, and how building your legal structures correctly from day one protects your wealth.

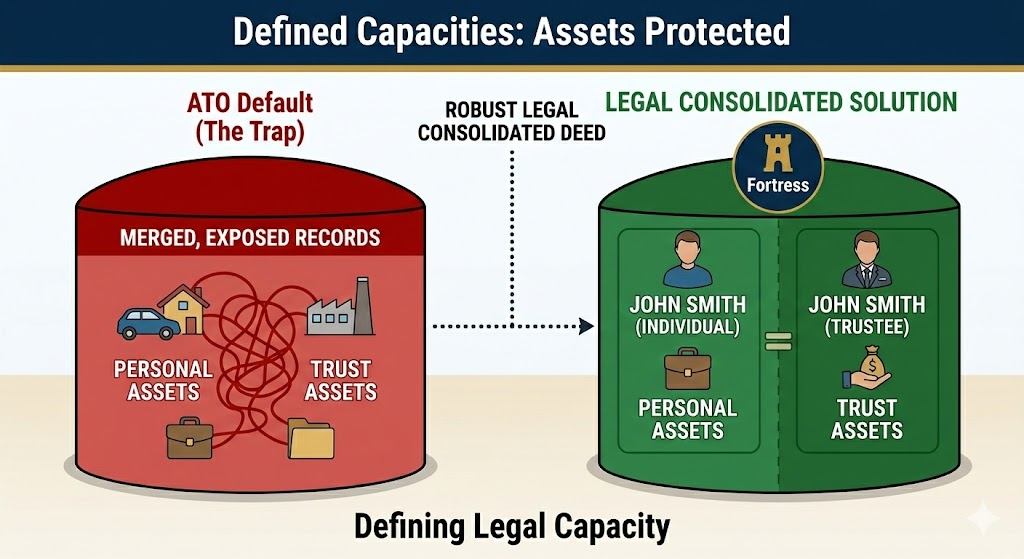

How the ATO Records an Individual Acting in Different Legal Capacities

The ATO’s AI data-matching systems are highly tuned to catch taxpayers who mix their personal affairs with their trust and company structures. PS LA 2011/8 explicitly instructs ATO staff on how to register and separate one person acting in multiple legal capacities.

For example, John Smith, the individual, is a completely separate taxpayer from John Smith acting as the trustee of a Family Trust or of a Bare Trust for a self-managed super fund. If an ABN or TFN application fails to explicitly define the correct legal capacity, the ATO systems can merge the records. Suddenly, a client’s personal tax return is entangled with their trust’s enterprise.

The Solution: Your accountant is your first line of defence in keeping these entities separate. But they need the right legal tools. When you build a Family Trust, Unit Trust, or Bare Trust at Legal Consolidated, you get the completed legal document with our comprehensive law firm cover letter. This letter gives your accountant and financial planner the exact best-practice wording to use when registering your new entity with the ATO, ensuring your personal assets remain legally walled off from the ATO’s reach.

Reconstituted Partnerships: Do You Need a New TFN and ABN?

When a partner retires or a new partner joins a partnership, the partnership is technically dissolved at law, and a new one is formed. So, does your accountant have to apply for a new TFN and ABN, and re-register for GST?

PS LA 2011/8 reveals the ATO’s internal approach to this headache. If there is a “continuity of enterprise,” the ATO may allow the reconstituted partnership to retain the same TFN and ABN. However, ATO staff are instructed to scrutinise these changes heavily. If your partnership agreement is weak or silent on succession, the ATO can strip the ABN, forcing your accountant to start from scratch and potentially triggering catastrophic Capital Gains Tax (CGT) events for the partners.

The Solution: A legally robust Partnership Agreement from Legal Consolidated protects the structure. It provides your accountant with the exact legal continuity they need to prove to the ATO that the enterprise remains intact, saving time, money, and compliance headaches.

When Can the ATO Backdate GST Registration?

We all know businesses must register for GST when their turnover hits the $75,000 threshold. But PS LA 2011/8 outlines the ATO’s terrifying ability to forcibly backdate a GST registration if they suspect “fraud or evasion.” If this happens, the ATO demands 1/11th of your gross revenue for past years as GST—even though you never collected it from your customers.

However, their internal manual also outlines how your accountant can use this GST backdating to a client’s advantage. If a company or Unit Trust spent six months incurring heavy set-up costs and legal fees before making a sale, your accountant can request to backdate the GST registration to the true commencement of the “enterprise.” This allows the client to claim back valuable input tax credits.

What are the ATO Rules for Appointing a Company Public Officer?

The Pty Ltd company appoints a Public Officer. This is part of the process of building a company on our law firm’s website. This person is personally answerable for the company’s tax compliance. If the company fails to lodge a return, the Public Officer is the one the ATO prosecutes.

What happens if the Public Officer goes overseas or falls ill? Most business owners have no idea that PS LA 2011/8 contains a specific concession allowing for the appointment of “alternate” or temporary Public Officers for a specified period of leave. A company POA adds to that protection.

The Solution: Your accountant will ensure a company’s corporate governance is airtight, but they rely on high-quality incorporation documents to do it. When you build a Company with Legal Consolidated, our documents understand the realities of ATO compliance, allowing your accountant to seamlessly manage the Public Officer requirements without leaving anyone personally exposed.

The Bottom Line: Backing Up Your Professional Advisers

The ATO is a highly sophisticated revenue-collecting machine. However, PS LA 2011/8 shows they have strict, limited processes for tracking every entity you operate.

Your best defence is an excellent accountant or financial planner, armed with legally rigorous documentation. We are the only law firm in Australia that provides legal documents directly online.

Whether you are building a:

- Company POA

-

or putting 3-Generation Testamentary Trusts into your Will

…we provide a tailored law firm cover letter with your document. This letter explicitly outlines the best practices for meeting the ATO’s different registration requirements. We build the legal fortress, and we hand your accountant the exact instruction manual they need to keep you safe.

Explanation and annotation of PS LA 2011/8

Below, we have published the LA 2011/8, with our law firm’s annotations in orange. Enjoy our free resources. We seek to educate; it is our highest goal:

[Law firm’s annotations in orange.]

Practice Statement Law Administration

PS LA 2011/8

| SUBJECT: | The registration of entities |

|---|---|

| PURPOSE: | This Practice Statement sets out the policy and procedures to be followed on a range of issues relating to the registration of entities, maintaining the client register and security of taxpayer data. It should be read in conjunction with Law Administration Practice Statement PS LA 2011/9 The registration of entities in the Australian Business Register. |

-

From 1 July 2015, the term ‘Australia’ is replaced in nearly all instances within the GST, Luxury Car Tax, and Wine Equalisation Tax legislation with the term ‘indirect tax zone’ by the Treasury Legislation Amendment (Repeal Day) Act 2015. The scope of the new term, however, remains the same as the now repealed definition of ‘Australia’ used in those Acts. This change was made for consistency of terminology across the tax legislation, with no change in policy or legal effect. For readability and other reasons, where the term ‘Australia’ is used in this document, it is referring to the ‘indirect tax zone’ as defined in subsection 195-1 of the GST Act.This document incorporates revisions made since original publication. View its history and amending notices, if applicable.

| This Practice Statement is an internal ATO document and an instruction to ATO staff. [The ATO employees are required to follow this.]Taxpayers can rely on this Practice Statement to provide them with protection from interest and penalties in the following way. If a statement turns out to be incorrect and taxpayers underpay their tax as a result, they will not have to pay a penalty, nor will they have to pay interest on the underpayment provided they reasonably relied on this Practice Statement in good faith. However, even if they do not have to pay a penalty or interest, taxpayers will have to pay the correct amount of tax provided the time limits under the law allow it. [The Courts are the final arbitrator, not Legal Consolidated or the ATO. However, if the ATO is wrong, then they will be ‘kind’.] |

[Dr Brett Davies comments: This is a crucial admission by the ATO. If you follow this internal manual, you get a “safe harbour” from penalties and interest. The ATO is bound by its own internal rules. This is exactly why, when you build an entity at www.legalconsolidated.com.au, our law firm cover letters are meticulously drafted to comply with these internal ATO guidelines. We provide your accountant with the exact arguments needed to defend your position if the ATO auditor comes knocking.]

BACKGROUND [of PS LA 2011/8]

1. We use unique identifiers to:

- enable the accurate identification of entities and persons for taxation law purposes

- record key information that will be accessed by multiple ATO systems and applications

- allow for the recording and management of taxpayer entitlements and obligations under income tax and other related laws

- create accounts for recording transactions within the tax system

- facilitate the sharing of information with other agencies as permitted or required by law.

2. Under taxation law, some registrations are compulsory in certain circumstances for different kinds of entities or persons. In other circumstances, registration is optional. There may be significant benefits to registration (such as not having tax withheld on interest earned from a financial institution).

3. For the purposes of this Practice Statement, consistent with relevant taxation law provisions, the term ‘person’ will be used in relation to a tax file number (TFN) registration. The term ‘entity’ will be used in relation to an Australian business number (ABN) registration and a goods and services tax (GST) registration or in discussing taxpayer obligations generally.

[Dr Brett Davies comments: Notice the subtle distinction here. A TFN attaches to a “person” (which includes a company or a trustee), but an ABN attaches to an “entity”. The ATO systems are easily confused if applied incorrectly. Our Legal Consolidated cover letters guide your accountant to ensure the right numbers are attached to the right legal vehicle, protecting your asset protection strategy.]

4. All legislative references in this Practice Statement are to the A New Tax System (Goods and Services Tax) Act 1999 (GST Act), unless otherwise indicated.

TERMS USED [of PS LA 2011/8]

5. The following terms are used in this Practice Statement:

Australian business number (ABN) – the entity’s ABN as shown in the Australian Business Register.

Australian Business Register (ABR) – the register established and maintained by the Registrar of the ABR. It may be kept in any form that the Registrar considers appropriate.

Australia – takes the same meaning as ‘indirect tax zone’ set out in section 195-1.

Applicant – in relation to an application for registration, means an entity or person specified in the application as the entity or person to be registered.

Approved form – takes the meaning set out in section 388-50 of Schedule 1 to the Taxation Administration Act 1953 (TAA). See Law Administration Practice Statement PS LA 2005/19 Approved forms for further information on approved forms.

Carrying on – in relation to an enterprise is defined in section 195-1 to include doing anything in the course of the commencement or termination of the enterprise.

Commissioner – means the Commissioner of Taxation.

Creditable acquisition – has the meaning given by section 11-5. An entity makes a creditable acquisition if

- •

- it acquires anything solely or partly for a creditable purpose

- •

- the supply of the thing to the entity is a taxable supply

- •

- it provides, or is liable to provide, consideration for the supply, and

- •

- it is registered or required to be registered.

Creditable importation – has the meaning given by section 15-5. An entity makes a creditable importation if

- •

- it imports goods solely or partly for a creditable purpose

- •

- the importation is a taxable importation, and

- •

- it is registered or required to be registered.

Creditable purpose – has the meaning given by section 11-15 in relation to creditable acquisitions and section 15-10 in relation to creditable importations.

Enterprise – has the meaning given by section 9-20. Further explanation of this term is contained in Miscellaneous Taxation Ruling MT 2006/1 The New Tax System: the meaning of entity carrying on an enterprise for the purposes of entitlement to an Australian Business Number.

Entity – in relation to GST registration and ABN registration has the meaning given by section 184-1. It means any of the following:

(a) an individual;

(b) a body corporate;

(c) a corporation sole;

(d) a body politic;

(e) a partnership;

(f) any other unincorporated association or body of persons;

(g) a trust;

(h) a superannuation fund.

Further explanation of this term is contained in MT 2006/1.

General law partnership – means an association of persons (other than a company or a limited partnership) carrying on a business as partners. Refer to paragraph 16 of Goods and Services Tax Ruling GSTR 2003/13 Goods and services tax: general law partnerships.

Government entity – has the meaning given by section 41 of the A New Tax System (Australian Business Number) Act 1999 (ABN Act) and means:

(a) a Department of State of the Commonwealth; or

(b) a Department of the Parliament established under the Parliamentary Service Act 1999; or

(c) an Executive Agency, or Statutory Agency, within the meaning of the Public Service Act 1999; or

(d) a Department of State of a State or Territory; or

(e) an organisation that:(i) is not an entity; and

(ii) is either established by the Commonwealth, a State or a Territory (whether under a law or not) to carry on an enterprise or established for a public purpose by an Australian law; and

(iii) can be separately identified by reference to the nature of the activities carried on through the organisation or the location of the organisation;

whether or not the organisation is part of a Department or branch described in paragraph (a), (b), (c) or (d) or of another organisation of the kind described in this paragraph.

GST – has the meaning given by section 195-1 and means goods and services tax that is payable under GST law.

GST branch – has the meaning given by section 54-5.

GST group – has the meaning given by section 48-5.

GST joint venture – has the meaning given by section 51-5.

GST turnover – means:

- •

- in relation to meeting a turnover threshold – has the meaning given by subsection 188-10(1), and

- •

- in relation to not exceeding a turnover threshold – has the meaning given by subsection 188-10(2).

Incapacitated entity – is an individual who is bankrupt, an entity that is in receivership or liquidation or an entity that has a representative as defined in section 195-1.

Input tax credit (ITC) – means an entitlement arising under sections 11-20 or 15-15.

Joint venture operator – of a GST joint venture, is the entity nominated to be the joint venture operator under paragraphs 51-5(1)(ea) or 51-70(1)(c).

Non-profit sub-entity – has the meaning defined in section 195-1.

Parent entity – is an entity that has a GST branch. For more information, refer to section 54-40.

Person – in relation to a TFN, is defined by section 202A of the Income Tax Assessment Act 1936 (ITAA 1936) to include a partnership, a company and a person in the capacity of trustee of a trust estate.

Proof of identity (POI) at registration – happens at registration or enrolment and involves the provision of documents as evidence of identity (such as a birth certificate, drivers’ licence or passport). For further information, refer to Chief Executive Instruction Identity management (link available internally only).

Proof of record ownership (PORO) – the provision of information related to a client record to give us assurance that the person making contact is authorised to access the information they are attempting to access. For further information, refer to Chief Executive Instruction Identity management.

Registrar – means the Registrar of the ABR. The Commissioner is the Registrar of the ABR.

Registration turnover threshold – has the meaning given by sections 23-15 and 63-25, and sections 23-15.01 and 23-15.02 of the A New Tax System (Goods and Services Tax) Regulations 2019.

Representative – has the meaning given by section 195-1 and means:

(a) a trustee in bankruptcy; or

(b) a liquidator [as defined in subsection 6(1) of the ITAA 1936]; or

(c) a receiver; or

(ca) a controller (within the meaning of section 9 of the Corporations Act 2001); or

(d) an administrator appointed to an entity under Division 2 of Part 5.3A of the Corporations Act 2001; or

(e) a person appointed, or authorised, under an Australian law to manage the affairs of an entity because it is unable to pay all its debts as and when they become due and payable; or

(f) an administrator of a deed of company arrangement executed by the entity.

Subsection 995-1(1) of the Income Tax Assessment Act 1997 (ITAA 1997) adopts this definition.

Resident agent – has the meaning given in section 195-1 and means an agent that is an Australian resident.

Reviewable GST decisions – are defined and listed in section 110-50 of Schedule 1 to the TAA.

Tax file number (TFN) – has the meaning given by section 202A of the ITAA 1936 and means a number issued to the person by the Commissioner, being a number that is either

- •

- a number issued to the person under Division 2 of Part VA of the ITAA 1936 or a number issued to a person under sections 44 or 48 of the Higher Education Funding Act 1988, or

- •

- a number notified, before the commencement of section 202A of the ITAA 1936, to the person as the person’s income TFN.

Tax law partnership – has the meaning given in the second limb of paragraph (a) of the definition of partnership in subsection 995-1 of the ITAA 1997 and means an association of persons (other than a company or limited partnership) ‘in receipt of ordinary income or statutory income jointly’.

Tax period – is the period for which an entity that is registered or required to be registered must lodge a GST return. These periods may be quarterly, monthly, annually or, in limited circumstances, another tax period such as a substituted accounting period. See section 195-1.

Taxable importation – has the meaning given by sections 13-5 and 114-5.

Taxable supply – has the meaning given by sections 9-5, 78-50, 84-5 and 105-5.

TFN declaration – has the meaning given by section 202A of the ITAA 1936. Completion of a TFN declaration will ensure that a pay as you go (PAYG) withholding amount is withheld at the appropriate rate in certain circumstances, including receipt of salary and wages, dividends and interest.

[Dr Brett Davies comments: Welcome to the above ATO ‘dictionary’. Never assume a word in a tax manual means what it means in the real world. If you read this list closely, you will spot several dangerous traps and a few closely guarded ATO secrets:

1. Consider the definitions for Proof of Identity (POI) and Proof of Record Ownership (PORO). The ATO states these are governed by a “Chief Executive Instruction”. That’s right—the ATO is judging your identity and your right to access your own tax records based on a secret, internal set of rules they won’t even let the public read!

2. Notice how a TFN attaches to a “Person”, but an ABN attaches to an “Entity”? At law, a trust is not a person—it is a relationship. The ATO knows this, which is why they define “Person” to artificially include a “person in the capacity of trustee”. This is exactly where cheap, off-the-shelf trust deeds fail. If your deed doesn’t legally separate the individual from the trustee capacity, the ATO systems will mangle your ABN and TFN registrations, exposing your personal wealth.

3. The ATO defines “carrying on” an enterprise to include “the commencement or termination” of it. This means the moment you start paying legal fees to set up your business, or the moment you sell the very last desk in your liquidated office, the ATO considers you to be “carrying on” a business. You are in their net before your doors open, and long after they close.

When you build your Family Trust, Company, or SMSF at www.legalconsolidated.com.au, you aren’t just getting a document. You are getting a legal structure designed by tax lawyers who actually know how to navigate this ATO double-speak and protect you from their hidden rulebooks.]

STATEMENT [of PS LA 2011/8]

6. This Practice Statement sets out the policy and procedures you must follow in relation to:

• TFNs

• GST registration

• maintaining the client register.

7. Some aspects of this Practice Statement apply to all or many registration types. The introductory paragraphs and paragraphs 110 to 133 of this Practice Statement also apply to registration of an ABN.

8. The Commissioner (including in the role as Registrar of the ABR) is required to:

- • record and maintain registration details (including establishing and maintaining the ABR) using formal and informal information-gathering powers to seek information in order to verify and update registration entitlements and details

- • maintain the confidentiality of TFNs and other taxpayer information in accordance with taxation law confidentiality provisions, the Privacy Act 1988 (Privacy Act) and the Privacy (Tax File Number) Rule 2015 issued under the Privacy Act

- • notify entities and persons when making certain changes to registration details (for example, cancelling a registration).

9. The TFN registration is attached to a person (as defined). An ABN or GST registration is attached to an entity (as defined).

10. Where a registration imposes obligations or provides entitlements, the date of effect may be important. Most provisions allow the Commissioner to determine the date of effect for registration and cancellation. These are generally reviewable decisions.

[Dr Brett Davies comments: Read paragraphs 8, 9, and 10 very carefully. They reveal the sheer scope of the ATO’s surveillance and control over your wealth.

First, look at paragraph 8. The ATO explicitly instructs its staff to use “informal information-gathering powers”. The taxman is not just reading the forms your accountant submits; they are actively data-matching your bank accounts, property records, and corporate footprints to verify your structure. If your Family Trust or Company is built on a flimsy, non-lawyer template, it will collapse under this level of scrutiny.

Second, paragraph 9 highlights the critical legal distinction that catches out almost every unrepresented taxpayer: A TFN attaches to a “person”, while an ABN and GST registration attaches to an “entity”. The ATO loves it when you confuse the two. If you accidentally register John Smith the individual instead of John Smith as Trustee for the Smith Family Trust, the ATO systems merge the records, instantly ripping apart your asset protection. Our Legal Consolidated documents and law firm cover letters prevent this by explicitly defining your legal capacity from day one.

Finally, paragraph 10 contains the ATO’s loaded gun: “the Commissioner [determines] the date of effect”. If you leave the start date of your enterprise ambiguous, the ATO will happily backdate your registration to a time that triggers maximum tax and GST liabilities for you. You must control the narrative. When you build your structures with us, we give your accountant the exact legal ammunition needed to dictate the commencement date on your terms, keeping the ATO on a tight leash.]

EXPLANATION [of PS LA 2011/8]

TAX FILE NUMBERS

11. This section of this Practice Statement deals with TFNs. In particular, it contains a TFN overview and deals with:

- applying for a TFN

- •

- refusal to issue a TFN

- •

- maintaining TFN records and declarations

- •

- TFN declarations

- •

- TFN security

- •

- compromised TFNs.

TFN overview

12. The TFN is a unique identifier issued by us to a person (as defined).

13. TFNs are used for a variety of purposes, including:

- identifying an account

- •

- enabling interactions between the account holder and us

- •

- increasing the effectiveness and efficiency of ATO data-matching

- •

- preventing income tax evasion

- •

- facilitating the administration of various Australian Government laws, such as those relating to social security, child support, super and higher education loans.

14. A person can only have one TFN at any time. If a new TFN is issued, any previously issued TFN will cease to have effect.

15. We may issue a TFN without an application being made where it is necessary to perform a function under a tax law.[1] For example, we may issue a TFN to enable an assessment to be made following a compliance enforcement activity.

Applying for a TFN

16. An application for a TFN must be in the approved form and accompanied by evidence of the applicant’s identity.[2] PS LA 2005/19 sets out how we administer approved forms.

17. Generally, persons (as defined) lodging their first application for a TFN may:

- complete an online form and attend a personal interview and present POI at registration at selected Australia Post outlets

- •

- apply online using myID if they are an Australian citizen with a current Australian passport, or

- •

- complete and lodge a paper TFN application form (including POI at registration documentation).

18. Information about how to apply for a TFN can be found at Apply for a TFN.

19. Special arrangements are in place to assist particular individuals register. These are through:

- Centrelink or the Department of Veterans’ Affairs if applying for government benefits or a pension

- •

- online application on arrival in Australia if a permanent migrant or temporary visitor

- •

- a form designed specifically for Aboriginal and Torres Strait Islander people, or

- •

- specific processes for prisoners and applicants from detention centres.

20. Non-individual applicants may also apply for a TFN:

- online through the ABR website, or

- •

- via the approved paper application form.

Minors applying for a TFN

21. Generally, if a person applying for a TFN is:

- under 13 years old – their parent or guardian must sign an approved application form on their behalf

- •

- 16 years old or older – they must sign their own approved application form

- •

- 13 years old or older, but under 16 years old – either the minor or the parent or guardian can sign the application form.

22. Where a parent or guardian signs the approved application form, they must provide:

- POI at registration for themselves

- •

- POI at registration for the minor

- •

- documentation that proves their relationship with the minor.

[Dr Brett Davies comments: Why are you getting a TFN for a 12-year-old? If it is just for a part-time job, fine. But if it is to put shares or bank accounts in their name to save tax, you are walking into a massive trap, and paragraphs 21 and 22 show exactly how the ATO catches you.

Read paragraph 22. The ATO forces the parent to provide their own Proof of Identity (POI) to obtain the child’s TFN. This is not just administrative; it is sophisticated data-matching. The ATO is actively linking your child’s financial footprint directly to your own tax file.

Why do they care? Because under Australian tax law (Division 6AA), unearned income directed to a minor is hit with penalty tax rates of up to 66%! The ATO uses this parent-child POI link to hunt down families trying to hide passive income in their children’s bank accounts.

This is why your accountant or financial planner will strongly advise against holding investments directly in a minor’s name. It is an asset protection and tax disaster. Instead of exposing your child—and your own identity—to the ATO’s data-matching web, you use a legal structure.

When you build a Legal Consolidated Family Trust, Bare Trust, or a Will containing a 3-Generation Testamentary Trust, you are using the correct, legally robust vehicles to pass wealth to the next generation. We build the legal documents that allow your accountant to legally stream income and protect your family’s privacy, keeping you far away from the ATO’s penalty tax net.]

Applicant does not require connection with tax system

23. Entitlement to a TFN is not contingent on the applicant establishing that they need or intend to use a TFN. An application that meets all the process requirements will result in us issuing a TFN.

24. If an applicant has no need for a TFN or the application is made in error, we may suggest to the applicant that they withdraw their application. This is done because TFNs have a specific tax purpose and it is undesirable to have unnecessary TFNs in the tax system. However, the person is entitled to proceed with their application in these circumstances.

[Dr Brett Davies comments: Read paragraphs 23 and 24, and you will see a classic example of ATO overreach.

Under Australian taxation law, you are legally entitled to a TFN. Period. Paragraph 23 admits this: if you meet the process requirements, the ATO *must* issue the TFN. You do not need to prove you are about to start trading tomorrow.

But look at paragraph 24! The ATO explicitly instructs its staff to actively “suggest” you withdraw your application if they personally feel you don’t “need” it yet. Why? Because the ATO thinks having too many TFNs in their system is “undesirable” and messy for their administrators. They are literally instructing their staff to talk you out of your legal rights just to save themselves some database clutter.

An unrepresented taxpayer might get intimidated by an ATO officer’s “suggestion” and withdraw their application, delaying their business plans. But a brilliant accountant knows that the law overrides ATO administrative preferences. If your accountant is setting up a new Family Trust, Unit Trust, or Bare Trust for a future transaction, they need that TFN ready to go so you aren’t delayed when the deal of a lifetime lands on your desk.

Never let a bureaucrat bully you into abandoning your legal entitlements. When you build your legal structures at www.legalconsolidated.com.au, we provide a comprehensive law firm cover letter. This letter arms your accountant with the exact legal backing they need to push past the ATO’s pushback and say, “Issue the TFN, my client is entitled to it by law.”]

Refusal of TFN application

25. We may refuse an application for a TFN if:

- the application is not received in the approved form, or

- •

- we are not satisfied as to the person’s true identity.

26. We must refuse an application if:

- the person already has a TFN, or

- •

- an interim notice has been issued under section 202BD of the ITAA 1936.[3] These notices are issued when a TFN applicant provides the name and address of the payer of the applicant, and we give the payer a notice that a TFN application is pending in relation to the applicant. This notice is valid for 28 days. If such a notice exists, there is already a TFN application in process.

Maintaining TFN records and declarations

Inactive TFNs

27. In some circumstances, it is necessary for a TFN to be deactivated. This may occur where, for example, we have been advised that an individual has died, the individual has departed the country permanently or a person has been inadvertently issued with 2 or more TFNs.

28. In certain circumstances, it is necessary to deactivate and replace a TFN, such as where the security of private information associated with the TFN has been compromised (see paragraphs 37 to 41 of this Practice Statement).

29. Deactivated TFN records are retained for record-keeping purposes.

TFN declarations

30. The TFN declaration form is an approved form[4] that is completed in a 2-stage process. The payee gives their completed form to their payer, who in turn countersigns the form, retains a copy and sends the original to us.[5] The payer and payee are both required to sign declarations to state that the information in their part of the form is true and correct.[6]

Lodging TFN declarations electronically

31. Payers who lodge their TFN declaration reports to us electronically may also receive a payee’s TFN declaration form electronically, including the payee’s electronic signature. Our requirements for an acceptable electronic signature are set out in fact sheet TFN declaration – approved electronic payee to payer process.

TFN security

32. A TFN is an important identifier used in administering the tax and superannuation systems, as well as some government services such as child support and personal assistance programs, and should be kept secure and confidential.

33. A person may not request or require another person to quote their TFN except as permitted by section 8WA of the TAA. However, person A may voluntarily disclose their TFN to person B (who is not authorised to request it), but person B may not record, use or disclose the TFN except as allowed by section 8WB of the TAA. Sections 8WA and 8WB apply to all types of persons, not just to us or other government officials.

34. Failure to maintain the security of their TFN and related personal information can adversely affect a TFN holder, including the TFN being used for fraudulent purposes such as identity theft. We recommend that persons:

- not store their TFN in their purse or wallet or on their mobile phone

- •

- shred or destroy documents when disposing of documents containing TFN details

- •

- install up-to-date anti-virus software on their computer or mobile phone

- •

- only provide their TFN to persons who are authorised to ask for it (such as us, their tax agent, financial institution or employer)

- •

- ensure that the tax agent they use to complete or lodge their tax return is registered, by checking the Tax Practitioners Board website (tpb.gov.au).

35. The Privacy (Tax File Number) Rule 2015 regulates the collection, storage, use, disclosure, security and disposal of individuals’ TFN information. It is legally binding and is available on the Office of the Australian Information Commissioner’s website (oaic.gov.au).

36. Under the Privacy (Tax File Number) Rule 2015, individuals cannot be compelled to quote their TFN but there may be consequences if they choose not to (for example, not being able to access certain Australian Government assistance benefits or having an assessment delayed). We are required to inform individuals of this when we ask them for their TFN.

Compromised TFN

37. We may classify a TFN as compromised if an unauthorised party has obtained the TFN. A TFN may also be compromised if an unauthorised party has access to sufficient information to obtain the TFN. A compromised identity may occur if an unauthorised third party has obtained personal identification details, such as a person’s name, address and date of birth.

38. A compromised TFN or identity may be caused by a range of circumstances, including one or more of the following:

- theft

- •

- loss or accidental disclosure

- •

- our error (for example, incorrectly matched records may lead to a taxpayer’s TFN being included in material provided to an unintended third party).

39. Remedial action may include implementing additional security measures for that taxpayer record or replacing the TFN.

40. In determining what remedial action, if any, should be undertaken, we will consider the facts and circumstances, such as:

- the likelihood of fraud, that is, the known or anticipated intent by the third party to defraud (for example, this would be higher where records are deliberately stolen from a tax agent’s office, compared to where records are lost in a natural disaster where they are likely destroyed)

- •

- whether the TFN has been associated with, or used by, another person

- •

- potential impacts on us, such as revenue risks or reputational risks arising from failure to take timely remedial action or to identify fraudulent activity

- •

- the cost and inconvenience to the taxpayer of any proposed remedial action

- •

- the likely effectiveness of the possible remedial action, including considering

- –

- if the remedial action will provide long-term sustainable resolution to the issue (for example, if a third party is known to have obtained, from a theft or disclosure, sufficient information to pass our PORO requirements, simply issuing a new TFN may not be appropriate or adequate action)

- –

- whether the remedial action for a prior compromise has been previously implemented and not succeeded, in which case, an alternative approach may be required

- –

- whether it is likely that the compromise will recur, regardless of the solution

- •

- the taxpayer’s preferences – although the decision to take remedial action is taken by us, the taxpayer’s preferences will be considered. However, there may be situations where a taxpayer would prefer to have their TFN replaced but we decline to do so, or some unusual cases where we insist on doing so.

Example 1 – identity theft, replacing TFN

41. Peter has a large share portfolio. A record of his TFN is stolen from his tax agent’s office by thieves targeting identity information. Peter would prefer not to replace his TFN as he would have to inform all the companies in which he holds shares. However, we decide that, as the thieves were specifically searching for identity information, the inconvenience to Peter is outweighed by the risk of the TFN being misused.

[Dr Brett Davies comments: TFN identity theft is rampant, but the ATO is notoriously reluctant to issue a new TFN because it makes a mess of their data-matching systems. In Example 1, the ATO forced a new TFN on Peter, but in many cases, taxpayers have to fight the ATO tooth and nail to get a compromised TFN cancelled. Never accept the ATO’s first “no”. Protect your structures—especially your Family Trusts, Unit Trusts, Bare Trusts and a corporate trustee of a trust—by fiercely guarding your entity TFNs. Identity theft can ruin the pristine asset protection moat we build for you.]

GST REGISTRATION

42. This section deals with GST registration. In particular, it contains a GST overview and deals with:

- applying for GST registration

- •

- cancelling GST registration

- •

- GST groups

- •

- GST joint ventures, and

- •

- GST branches.

Applying for GST registration

43. Entities that carry on an enterprise and have a GST turnover of $75,000 (or $150,000 for non-profit bodies) or more are required to register for GST.[7] Entities that carry on an enterprise with a turnover of less than $75,000 (or $150,000 for non-profit bodies) may register for GST if they choose. It is the entity that is registered for GST, not the enterprise.

44. If an entity is registered or required to be registered, they must pay GST on any taxable supplies and taxable importations that they make. They are also entitled to ITCs for creditable acquisitions and creditable importations.

Registering for GST

45. We must register an entity for GST if[8]:

- an application for registration has been made in the approved form, and

- •

- they are satisfied that the entity is carrying on an enterprise or intends to carry on an enterprise from the date specified in the application.

46. We must also register an entity if we are satisfied that the entity is required to be registered, even if the entity has not applied for registration.[9]

47. An entity may choose to register for GST if it[10]:

- is carrying on an enterprise and its GST turnover is below the registration turnover threshold, or

- •

- intends to carry on an enterprise from a particular date.

48. If an entity is required to be registered, it must apply in the approved form to us within 21 days after becoming required to be registered.[11] If an entity is entitled to be registered but not required to do so, it may apply at any time.

49. MT 2006/1 considers the meaning of the terms ‘entity’ and ‘enterprise’ in relation to entitlement to an ABN. The principles in MT 2006/1 apply equally to the terms ‘entity’ and ‘enterprise’ in the GST Act (see Goods and Services Tax Determination GSTD 2006/6 Goods and services tax: does MT 2006/1 have equal application to the meaning of ‘entity’ and ‘enterprise’ for the purposes of the A New Tax System (Goods and Services Tax) Act 1999?).

50. Carrying on an enterprise includes doing anything in the course of commencement of that enterprise.[12] Activities undertaken in the commencement of an enterprise may include feasibility studies involving genuine business activities where, from the scale and nature of these activities, it is clear that there has been serious contemplation of developing an enterprise. However, the mere intention by an entity to commence an enterprise is not commencement activity.

51. We will require POI at registration to establish the identity of the applicant and its associates (where appropriate) when an entity applies for GST registration. There is no express provision for the Commissioner to seek information necessary to establish the identity of the applicant and its associates. However, the approved form provisions in the TAA empower the Commissioner to determine the information and additional statements or documents that an approved form will require. This can extend to any information which has a reasonable connection with the purpose for which it is sought (such as information to identify an applicant seeking GST registration).

Registration date of effect

52. An entity’s registration will take effect from the date specified in its registration application, unless we specify another date.[13]

53. Where an entity registers for GST on the basis that it intends to carry on an enterprise, the date of effect of registration must not be earlier than the date the entity specifies in its application as the date from which it intends to carry on the enterprise.[14]

54. We must notify the entity in writing of[15]:

- the date of effect of the registration

- •

- the registration number, and

- •

- the tax periods that apply to the entity.

55. The Registrar of the ABR must also enter the date of effect of the entity’s GST registration in the ABR.[16]

56. Where an entity that has an ABN applies for a GST registration or an entity applies for ABN and GST registration at the same time, the GST registration number will be the same as the ABN, even though they are separate registrations.

Backdating GST registration

57. We may backdate an entity’s GST registration, subject to the following limitations[17]

- Where no registration application is made, the date of effect cannot be before the day on which the entity became required to be registered.

- •

- Where the entity applies for registration, the date of effect cannot be before the date the entity specified in the application, unless we are satisfied that the entity was required to be registered as of an earlier date.

58. If an entity’s GST registration is backdated, it will result in the entity being required to pay GST on taxable supplies and taxable importations made from that earlier date. The entity will be entitled to claim ITCs on creditable acquisitions or importations from the earlier date, provided the appropriate documentation is held.[18] However, for tax periods that commence on or after 1 July 2012, we cannot backdate the date of effect to a date that is more than 4 years before the date on which we decide the date of effect of the entity’s registration.[19]

[Dr Brett Davies comments: Here is the ATO’s secret weapon against your wealth. They can backdate your GST registration up to four years if they think you’ve been dodging the system. Suddenly, you owe 1/11th of your gross turnover for the last 48 months—money you never collected from your customers or clients! Conversely, a clever accountant can use this rule to your advantage, backdating registration to claim heavy set-up costs. Our Legal Consolidated company and trust cover letters guide your accountant on exactly how to position your “commencement of enterprise” date to the ATO to avoid this trap.]

GST-only registration

59. An entity qualifies for an ABN by carrying on an enterprise in Australia, whereas an applicant for GST registration need only carry on an enterprise.[20] Non-resident entities that are carrying on an enterprise, although not in Australia, may apply for GST registration but are not entitled to an ABN because they are not carrying on an enterprise in Australia.

60. There are a number of situations where entities are registered for GST without having an ABN. The most common examples of this are

- •

- non-residents entitled to ITCs – if an entity is not carrying on an enterprise in Australia or making supplies connected with Australia, it will not be entitled to an ABN

- •

- GST audit cases where the entity is not registered for GST but is required to be. The entity can be registered for GST whether or not it applies but cannot be registered in the ABR unless it applies.

61. Where an entity is entitled to GST registration but not to an ABN, it will be provided with a GST registration number for use when meeting its GST obligations.

Example 2 – registered for GST without an ABN

62. Ray Source is a livestock breeder in the United States of America. He buys 3 brood mares in Australia and pays GST on purchase. He exports the horses to his ranch in Kentucky and seeks registration for GST to claim ITCs. As he is carrying on an enterprise, he can register for GST. As Ray is not carrying on an enterprise in Australia, and not making supplies connected with Australia in the course of an enterprise he carries on elsewhere, he is not entitled to an ABN.

Entities subject to special rules for GST registration

63. A government entity is not required to be registered even if it is carrying on an enterprise and its GST turnover meets the registration turnover threshold.[21] However, a government entity may apply for registration even if it does not meet the usual criteria for registration. That is, it may apply to be registered even if it is not an entity and is not carrying on or intending to carry on an enterprise.[22]

64. Some kinds of non-profit entities may choose to have some (or all) of their separately identifiable branches treated as separate entities for GST purposes. A non-profit sub-entity may be registered for GST if the criteria set out in section 63-5 are met, even if the non-profit sub-entity is not carrying on, or not intending to carry on, an enterprise.[23]

65. If an entity supplies taxi travel as part or all of its enterprise, it must register for GST irrespective of its GST turnover.[24] Taxi travel is travel that involves transporting passengers, by taxi or limousine, for fares.[25]

66. The representative of an incapacitated entity must register for GST in that capacity, if the incapacitated entity is registered or required to be registered.[26]

67. A resident agent of a non-resident is required to be registered if the non-resident is registered or required to be registered.[27]

[Dr Brett Davies comments: Welcome to the ATO’s double standards: one rule for the King, and another for the peasants.

Read paragraph 63 and try not to laugh. If your private Company or Family Trust crosses the $75,000 turnover threshold, the ATO will ruthlessly hunt you down, force you into the GST net, and backdate your taxes. But a Government department? The ATO says they don’t have to register at all, even if they are making millions. Worse, a government entity can choose to register even if it does absolutely nothing—just so it can claim back the juicy GST input tax credits!

And then look at paragraph 65. The government protects its massive revenue from the transport industry by declaring that if you drive a taxi or an Uber, the $75,000 threshold vanishes. You are taxed on the very first dollar you earn.

The ATO stacks the deck against private enterprise. The government writes exemptions for itself while tightening the screws on your business. This is why going into business with a cheap, non-lawyer template is corporate suicide. You are fighting an opponent that literally rewrites the rules in its own favour.

When you build your Company, Family Trust, Unit Trust, or Partnership at www.legalconsolidated.com.au, you are arming your accountant with legally rigorous, law firm-certified documents. We build the strongest possible legal fortress around your wealth so your accountant can fight the ATO on a level playing field.]

GST branches

68. We must register a branch of a parent entity as a GST branch if[28]:

- (a)

- the parent entity is registered for GST and applies in the approved form for registration of the branch, and

- (b)

- we are satisfied that the branch maintains an independent accounting system and can be separately identified either by the nature of its activities or by its location, and

- (c)

- we are satisfied that the parent entity carries on, or intends to carry on, an enterprise through the branch, from a particular date specified in the application.

69. A branch cannot be registered as a GST branch if the parent entity is a member of a GST group.[29]

GST groups

70. Two or more entities may form a GST group if[30]:

- each of the entities satisfies the membership requirements of the group

- •

- each of the entities agrees in writing to forming the group

- •

- one of the entities notifies us, in the approved form, of the formation of the group

- •

- the notifying entity is nominated in that notice to be the representative member of the group, and

- •

- that entity is an Australian resident.

71. If a group’s representative member nominates to us a date for forming, changing or dissolving the group, but does so after the day by which they were required to give to us a GST return for the period within which the nominated date falls, they must apply for approval of the backdated date of effect.[31]

72. If a GST group is formed or entities leave or join an existing GST group part way through a tax period, the entities will be responsible for their own GST obligations for the relevant period during which they are not in the GST group.[32]

GST joint ventures

73. Two or more entities may become participants in a GST joint venture if[33]:

- the joint venture is for the exploration or exploitation of mineral deposits, or for a purpose specified in the A New Tax System (Goods and Services Tax) Regulations 2019

- •

- the joint venture is not a partnership

- •

- each of those entities satisfy the participation requirements of a GST joint venture (see section 51-10)

- •

- each of the entities agree in writing to the formation of the joint venture as a GST joint venture

- •

- one of the entities, or another entity, is nominated in that agreement to be the joint venture operator of the joint venture

- •

- the nominated joint venture operator notifies us, in the approved form, of the formation of the joint venture as a GST joint venture, and

- •

- the nominated joint venture operator is not a party to the joint venture agreement, that entity must be registered for GST and account for GST on the same basis as the participants in the joint venture.

Refusal of GST registration

74. We may refuse an entity’s application for GST registration if they are not satisfied that the entity is carrying on an enterprise or intends to do so from a particular date specified in the application. However, special rules apply to some entities such as non-profit sub-entities and government entities, which may register regardless of whether they meet these criteria (see paragraphs 63 to 67 of this Practice Statement).

75. We may also refuse an application if it is not in the approved form, including the provision of POI at registration information required by the approved form. For a non-individual applicant, POI at registration may include the TFN or proof of the identity at registration of some individuals who are associates of the entity (for example, the directors of a company).

76. We must notify an entity in writing of a decision to refuse to register the entity.[34] A decision to refuse to register an entity is a reviewable GST decision.[35]

[Dr Brett Davies comments: Why would the ATO ever refuse to let you register for GST? Surely they want your tax dollars? The danger lies in paragraph 75. The ATO uses GST registration as a Trojan horse to map out your entire family and corporate structure.

When your accountant applies for GST for your new Company or Unit Trust, the ATO has the power to demand the Proof of Identity and TFNs of “associates”—which includes company directors, partners, and potentially trust beneficiaries. If you use a cheap, non-lawyer template that poorly defines who actually controls the entity, you give the ATO a free pass to go on a fishing expedition through your entire family’s tax history.

Furthermore, paragraph 74 states that they can refuse registration if they don’t believe you are actually “carrying on an enterprise” (e.g., they think your business is just a hobby for claiming tax deductions). How do you prove you are running a real enterprise? With legally rigorous documentation. When you build your company, partnership, or trust at www.legalconsolidated.com.au, you are generating law firm-quality documents that explicitly prove your commercial intent from day one, shutting down the ATO’s excuses to reject your registrations.]

Cancelling a GST registration

77. An entity must request cancellation of their GST registration within 21 days of ceasing to carry on an enterprise or if it did not commence carrying on an enterprise.[36] An entity ceases carrying on an enterprise when it concludes doing everything in the course of terminating its enterprise.

78. Failure to cancel a registration may result in a penalty of 20 penalty units.[37]

79. If a registered entity is entitled to be registered for GST but is no longer required to be registered (for example, its GST turnover has dropped below the registration turnover threshold), it may apply to have its registration cancelled.

80. An entity that is required to be registered for GST cannot cancel its GST registration. (For a more detailed explanation of the terms ‘entity’ and ‘enterprise’, refer to MT 2006/1 which applies in both the GST and ABN context).

81. Cancellation of the GST registration will also result in the cancellation of fuel tax credit, luxury car tax and wine equalisation tax registrations.

82. If an enterprise which has been carried on by an entity continues but is undertaken by a new entity, the old entity must cancel its registration unless it is carrying on another enterprise. This includes entities with associated individuals in common, such as a partnership whose partners then become directors of a company which proceeds to carry on the enterprise. The new entity may apply for a new registration. This is because it is the entity that is registered for GST, not the enterprise.

[Dr Brett Davies comments: Selling your business, retiring, or finally upgrading your risky legal structure? The ATO has set a strict 21-day trap for you, and it is armed with fines.

Read paragraph 78. If you shut down an enterprise and forget to tell the ATO within 21 days, they can hit you with a fine of 20 penalty units. As of the current penalty unit rates, that is thousands of dollars in a pure “lazy tax”.

But the real danger for business owners is hidden in paragraph 82. The ATO explicitly states that GST registration attaches to the *entity*, not the *business itself*. This is the number one mistake unrepresented taxpayers make when restructuring. If John and Mary run a café as a Partnership, and their accountant wisely advises them to upgrade their asset protection by transferring the café into a new Company owned by a Family Trust, the old Partnership MUST cancel its GST registration within 21 days. The new Company must apply for a brand new one. You cannot just “hand over” the ABN and GST registration to the new structure, even if the same people are running the show.

This is why a brilliant accountant is worth their weight in gold. When your accountant helps you build a Legal Consolidated Company, Family Trust, or Unit Trust to protect your wealth, our documents cleanly and legally execute the transfer of the enterprise. We then provide a comprehensive law firm cover letter that gives your accountant the exact roadmap to safely cancel the old ATO registrations and set up the new ones, keeping you far away from the ATO’s penalty regime.]

Example 3 – registering for GST, entity or enterprise

83. Catherine and Peter are carrying on an enterprise as partners and the partnership is registered for GST. They change their business structure by incorporating and becoming directors of a Corporations Act company that is carrying on the same enterprise as previously carried on by the partnership. As it is the entity which is registered for GST, not the enterprise, the company will need to apply for GST and the partnership, if it is not carrying on another enterprise, must cancel its registration.

84. Similarly, if Catherine and Peter sell the enterprise to a partnership between Lisa and Anthony, Lisa and Anthony will need to register for GST. Catherine and Peter, if they are not carrying on any other enterprise, will need to cancel their GST registration.

[Dr Brett Davies comments: This is a massive, highly dangerous trap! If a partner retires or dies, the ATO considers the partnership dissolved at law. You instantly lose your ABN, your TFN, and potentially trigger a massive Capital Gains Tax (CGT) event. The ONLY way to save the business is with a legally binding “continuity clause”. Off-the-shelf partnership templates often fail here. The Legal Consolidated Partnership Agreement explicitly includes bulletproof continuity and succession clauses to satisfy paragraph 115, saving your business from an ATO-induced collapse.]

85. If an entity applies in the approved form to cancel its GST registration and we are satisfied that the entity is not required to be registered:

- if the entity has been registered for at least 12 months, we must cancel the registration[38], and

- •

- if the entity has been registered for less than 12 months, we may cancel the registration.[39]

86. We must also cancel the entity’s GST registration, even if the entity has not applied for cancellation, if they[40]:

- are satisfied that the entity is not carrying on any enterprise, and

- •

- believe on reasonable grounds that the entity is not likely to carry on any enterprise for at least 12 months.

87. We must notify an entity of any decision made in relation to cancelling the entity’s GST registration. If we decide to cancel the registration, the notice must specify the date of effect of the cancellation.[41] Cancelling an entity’s registration or refusing to cancel an entity’s registration is a reviewable GST decision.

Date of effect of cancellation of GST registration

88. We must decide the date on which the cancellation of a GST registration takes effect. The date of effect of cancellation may be any day occurring before, on or after the day on which we make the decision to cancel the registration.[42]

89. We will not cancel the registration with effect from a date on which the entity was required to be registered and will not usually do so from any date when the entity was operating as if it were registered for GST.

90. When an entity that was required to be registered applies to cancel its registration, we will ordinarily accept the cancellation date the entity chooses, provided that the entity:

- was not required to be registered after that date

- •

- was entitled to be registered before that date

- •

- has been registered for 12 months, and

- •

- has at that date ceased operating on a GST-registered basis.

91. When an entity that is registered but was not required to be registered (a voluntary registration) applies to cancel its registration:

- if we are satisfied that the entity has never operated on a GST-registered basis, we may accept the application to cancel the GST registration from a retrospective date chosen by the entity

- •

- if the entity has operated on a GST-registered basis but has ceased doing so before the application to cancel registration is made, we may accept the entity’s application to cancel its GST registration from the start of the tax period which commences on or after the date it stopped operating on a GST-registered basis

- •

- if the entity is still operating on a GST-registered basis at the time of the application to cancel registration, the date of cancellation will generally not be retrospective. We will negotiate a prospective date if the application does not state one.

92. The date of effect of cancellation effect is a reviewable GST decision.[43]

93. We will be satisfied that an entity has stopped operating (or never operated) on a GST-registered basis from a certain date if, from that date or an earlier date, the entity:

- did not hold themselves out to other businesses as being registered for GST

- •

- did not issue any tax invoices or adjustment notes

- •

- did not claim any ITCs, special transitional credits or indirect transitional credits, and

- •

- has made a declaration to us that satisfies all of the above points.

Dissolving GST groups or removing group members

94. The representative member may notify us in the approved form that a GST group is dissolved or that one or more of the entities is removed from the group. If a group’s representative member ceases to be the representative member, the new representative member must notify us within 21 days of becoming a representative member. The GST group will be dissolved unless a new representative member is nominated with effect from the day after the previous representative ceased to be the representative member.[44]

95. A GST group member that becomes incapacitated may be removed from the group by the representative member or the representative of the incapacitated member. If the representative member becomes an incapacitated entity and it does not cease to be a group member, it ceases to be the group representative member unless all other group members are incapacitated entities.[45]

96. Under section 27-39, an incapacitated entity’s tax period ceases at the end of the day before incapacitation, which generally means that the incapacitated member has a tax period different to those applying to the other members and therefore breaches one of the membership requirements. However, the representative member may elect that the tax periods of the other GST group members will end at the same time as that of the incapacitated member thereby allowing the incapacitated member to remain in the group.[46] The election must be made in the approved form within 21 days after the member becomes an incapacitated entity.[47]

[Dr Brett Davies comments: GST grouping is a brilliant strategy your accountant uses to save your business massive amounts of cash flow. It allows your related Companies and Unit Trusts to trade with each other without charging GST. But paragraphs 94 to 96 expose a terrifying ATO trap: the domino effect of liquidation.

Look at paragraph 94. The ‘representative member’ is the head of your GST group. If that head entity changes, you have exactly 21 days to notify the ATO. Miss that deadline? The ATO automatically dissolves your entire GST group. Suddenly, every single transaction between your internal companies is subject to 10% GST. That is a catastrophic, unexpected tax bill.

But the real secret trick is buried in paragraphs 95 and 96. What happens if one of your subsidiary companies goes into liquidation, receivership, or administration (what the ATO calls an “incapacitated entity”)? The ATO states that the incapacitated company’s tax period instantly changes. Because it no longer has the same tax period as the rest of the group, it breaches the grouping rules. If your accountant does not lodge a highly specific election within 21 days, the ATO uses this technicality to tear the group apart.

This is exactly why you need a brilliant accountant monitoring your corporate health, armed with bulletproof legal structures. When you build your Company, Unit Trust, or Family Trust at www.legalconsolidated.com.au, you are giving your accountant the highest quality legal foundation to manage these complex grouping rules. We build the fortress, but your professional adviser mans the walls, ensuring a single insolvency doesn’t trigger an ATO raid on your entire corporate group.]

Cancelling GST branches

97. We must cancel the registration of a GST branch if[48]:

- the entity has applied for cancellation of registration in the approved form, and

- •

- the branch had been registered for at least 12 months at the time of the application.

98. An entity must apply for cancellation of registration of its GST branch if it is not carrying on an enterprise through the branch.[49] It must lodge the application within 21 days of ceasing to carry on an enterprise through the branch.[50]

99. We must also cancel the registration of a GST branch, even without an application being made, if satisfied that the entity[51]:

- is not carrying on an enterprise through the branch, and

- •

- will not carry on an enterprise through the branch in the following 12 months.

100. The date of effect of cancellation of the registration of a GST branch may be any date occurring before, on or after the day on which we make the decision.[52]

101. Cancellation of an entity’s registration will automatically cancel the GST registration of its branch or branches, with the same date of effect.[53]

102. Refusing to cancel a branch’s GST registration, cancelling a branch registration without an application and deciding the date of effect of cancellation of a GST branch are all reviewable GST decisions.[54]

Registration requirements for representatives of incapacitated entities

103. A representative of an incapacitated entity is required to be registered for GST in their capacity as a representative, if the incapacitated entity is registered or required to be registered.[55] If more than one representative is appointed over the assets of the incapacitated entity, each representative will be required to register, unless the representatives are appointed jointly, in which case there is a single registration for the joint appointment. If the incapacitated entity is registered or required to be registered, the tax periods applying to the representative in that capacity are the same tax periods that apply to the incapacitated entity.[56]

104. We must cancel the registration of a representative of an incapacitated entity if they are satisfied that the representative is not required to be registered in that capacity. We must notify the representative of the cancellation.[57]

105. When a representative ceases to be a representative of the incapacitated entity, they must notify us in the approved form within 21 days.[58]

106. The Commissioner (in their capacity as Registrar of the ABR) will allow the representative of an incapacitated entity to use the incapacitated entity’s existing ABN for transactions conducted in its capacity as the representative of the incapacitated entity. We will set up a new running balance account under the incapacitated entity’s ABN for each representative to cover post-appointment liabilities and entitlements. However, a trustee in bankruptcy will need to apply for a separate ABN in respect of each appointment as trustee under the Bankruptcy Act 1966.

Other notifications required of representatives

107. A liquidator must give written notice to us of their appointment within 14 days after becoming liquidator.[59]

108. A receiver must give written notice to us within 14 days after taking possession of the assets of the entity in receivership.[60]

MAINTAINING THE CLIENT REGISTERS

109. This section of the Practice Statement deals with maintaining the client registers. In particular, it deals with:

- registration of partnerships consisting of one entity or person acting in different legal capacities

- •

- registration requirements where an entity or person restructures

- •

- change of sex code

- •

- registration for minors (making decisions and signing forms)

- •

- recording names on the client registers

- •

- public officers.

Registration of partnerships consisting of one entity or person acting in different legal capacities

110. An entity (as defined) or person (as defined) can act in a number of different capacities. For example, in addition to their individual capacity, an individual may be a trustee of one or more trusts. In each of those capacities, the individual is taken to be a different entity or person. This also applies where the trustee is a company.

111. The Commissioner (including when acting as Registrar of the ABR) may accept an application for registration from a partnership (for a TFN, ABN, GST or other role registration) if satisfied that the entities involved are together proprietors of the relevant business or assets that are being used to carry on a business or to derive income jointly. The partnership can be either a general law or tax law partnership and must be comprised of:

- 2 or more entities or persons being an individual or company in their own right and that individual or company as trustee of one or more trusts, or

- •

- 2 or more entities or persons being an individual or company as trustee of 2 or more trusts.

Example 4 – one individual with multiple roles

112. Margaret as an individual and Margaret as trustee for the Scanlan Family Trust are partners in an enterprise. There is only one natural person (Margaret) involved, but she is there in 2 capacities (individual and trustee). The Registrar will register the partnership.

[Dr Brett Davies comments: The ATO calls this the ‘Multiple Personalities’ rule. This is where most cheap, non-lawyer templates fail completely. The ATO systems frequently merge John Smith the individual with John Smith the trustee of the Smith Family Trust. This is an asset protection disaster, exposing personal wealth to business risk. When you build a trust with Legal Consolidated, our documentation and cover letters strictly define the legal capacity of the trustee. We force the ATO to respect the legal wall between your personal assets and your trust.]

Reconstituted partnerships

113. Where a partner exits a general law partnership (the partnership) and the assets and liabilities of that partnership are taken over by the continuing partners (and any new partners) and the partnership business is continued without any apparent break, a technical rather than a general dissolution has occurred. This is known as a reconstituted partnership.

114. A reconstituted partnership, providing the conditions in paragraph 115 of this Practice Statement are met, can continue to use the same TFN, GST registration or ABN as the pre-reconstitution partnership. The partnership will only be required to complete one tax return for the income year in which the reconstitution took place. The reconstituted partnership treatment only applies to general law partnerships, not to tax law partnerships.

115. All of the following conditions must be satisfied if a reconstituted partnership wishes to continue to use its existing TFN, GST registration or ABN:

- •

- There must be at least one continuing partner who is a member of the partnership prior to and following the reconstitution.

- •

- There must be an express or implied continuity clause agreed to by the continuing, incoming and outgoing partners. This includes a clause in the partnership agreement, a statement signed by the partners or an oral agreement by the partners.

- •

- The following must be satisfied

- –

- substantially all of the partnership assets remain with the continuing partnership

- –

- the nature of the enterprise remains substantially unchanged

- –

- the client or customer base remains substantially unchanged

- –

- the business name or name of the firm remains unchanged.

- ‘Substantially’ means largely or considerably. This is taken to mean more than 50%, though each case will need to be decided on its own facts.

- •

- When lodging the partnership tax return, the following details must be supplied

- –

- the date of the dissolution

- –

- the date of the reconstitution

- –

- the names of the new, continuing and retiring partners

- –

- the TFN or address and date of birth of all new partners

- –

- details of the changes if the contacts authorised to act on behalf of the partnership have changed.

116. If all of the conditions set out in paragraph 115 of this Practice Statement are not met, the original partnership will be dissolved and a new partnership created. In this case:

- •

- the new partnership will be required to register for a new TFN, GST registration and ABN

- •

- the former partnership will be required to cancel their GST registration and ABN if they are not carrying on any other enterprise

- •

- the new partnership will be required to lodge a tax return for the period from the date of its formation to the end of the income year

- •

- the former partnership will be required to lodge a tax return from the beginning of the income year to the date of dissolution.

Registration requirements where an entity or person restructures

Government entities

117. Government entities at the Commonwealth, state, territory and local level may undergo a variety of structural changes that include but are not limited to:

- •

- the merging of 2 bodies

- •

- a change in the type of entity (for example, a change from one type of government body to another

- •

- the whole or part of an entity being absorbed by another entity.

118. Such restructures are commonly referred to as ‘machinery of government changes’.

119. Machinery of government changes give rise to questions as to whether the entity or entities emerging from a restructure need to apply for new registrations or roles, such as TFN, ABN, GST, PAYG withholding, fringe benefits tax and fuel tax credits, or may instead continue the registrations and roles of the pre-change entity.

120. Where it is evident that an entity emerging from a machinery of government change is to be treated at law as a continuation of the pre-change entity, the TFN, ABN and other roles of the pre-change entity continue unaltered with only a change to the entity name. Relevant evidence is found in the primary or delegated legislation, administrative orders or gazettal notice. The legislation should contain specific transition, transfer and savings provisions which provide that the new entity is to be treated as if it were the former entity such that the new entity has all the rights, entitlements, liabilities and obligations of the former entity.

121. Where there is no such evidence, an entity emerging from a machinery of government change must apply for new registrations.

122. Where it is evident that a government entity continues, in fact, after the machinery of government change, there is no new and former entity for which there is a need to establish continuity. Such cases do not need to be treated in accordance with this Practice Statement and the entity may continue to use their existing registrations. An example of the continuation of an entity in fact is where a State Governor gives notice in their state’s Gazette that an existing department has been renamed and had some functions added or taken away (sometimes referred to as having its ‘designation altered’) under the relevant state Public Sector Management Act (or equivalent). In this example, no new primary or delegated legislation has been passed. Rather, powers under the existing statute have been used to restructure a department without abolishing it.

Registrations and sex code

123. When registering an individual, we will record the individual’s sex or gender as described in the primary POI documents. In cases where an individual seeks to change the record of their sex or gender, they are required to provide one of the following documents specifying their preferred sex or gender:

- •

- a statement from a registered medical practitioner or a registered psychologist, or

- •

- a valid Australian Government travel document, such as a valid passport, or

- •

- an amended state or territory birth certificate, or

- •

- a state or territory gender recognition certificate or recognised details certificate showing a state or territory Registrar of Birth, Deaths and Marriages.

124. Sex reassignment surgery or hormone therapy are not pre-requisites for the recognition of a change of sex or gender in our records.