Six reasons to set up an Australian Partnership Agreement?

The partnership agreement is a contract between the partners. It agrees to the terms of the business. A Partnership Agreement deals with:

- financial reporting

- responsibilities of the partners

- each partner’s financial contribution – capital contributions

- a procedure for resolving disputes

- a procedure for ending or resigning from the partnership

- a partner’s share of the business’s tax losses is offset against other personal income. This is called the ‘flow through’ effect. In contrast, losses in companies and trusts are ‘trapped’.

What is the purpose of an Australian Partnership Deed?

A partnership is formed to share profits or losses between the partners. A partnership may have a set of rules. These are set out in a Partnership Deed. A Partnership Deed is a voluntary contract. It is between two or more persons. The partnership agreement shows how the partners share the partnership’s profit and capital.

In Australia, when two or more people team up for a business and share its profits and losses, they are automatically in a partnership. Unlike a trading company, a partnership is not a separate legal entity. This means each partner is personally responsible for what other partners do and any debts the partnership gets into. If you are in a partnership, your accountant will recommend that you build a partnership agreement.

Not having a written partnership agreement is dangerous

We all love the simplicity of a partnership. Indeed, many people are in ‘partnerships’ without their knowledge. However, undocumented partnerships are dangerous.

You have a friend. Together, you have a vision. You work together in your new business to make a profit. Congratulations, you are in a partnership.

Now that you are in a partnership, you need to document it. Build a Partnership Deed on our law firm’s website. Just press the Start Building above. There are hints that explain every question. And you can telephone us anytime to help you answer the questions.

If you do not document your partnership, you suffer risks and potential losses. You also risk joint and several liability with your partners.

Default Rules for Partnerships without Written Agreements

In Australia, without a partnership deed, the governance of business partnerships is controlled by the government. If you do not have a written partnership agreement, the rules and regulations governing your partnership default to this older, outdated state legislation. Five of the states have legislation that dates back to the nineteenth century.

Operating a partnership without a written agreement means that your business is subject to the general provisions in these laws, which do not reflect current practices or your specific intentions.

These default rules can vary significantly from state to state, making interstate business more complicated. Therefore, it is advisable to build a tailored written partnership agreement on Legal Consolidated’s website. Our Partnership Deeds contain terms and conditions that are aligned with the modern business environment, taxation rules and partnership goals. This provides both clarity and security for all partners. It minimises reliance on outdated statutory provisions.

A complete list of acts that control partnership agreements in Australia

In Australia, each state has its own legislation governing partnerships. What if you have no written partnership agreement? Then you have to rely on out-of-date legislation in each state:

Fake law firm websites claim to source legal documents from a law firm. However, they incorrectly reference the old acts in their Partnership Deeds. These old acts are permissive and should not control your Partnership Deed. Build your Partnership Deed directly from a lawyer’s website.

ACT – Partnership Act 1963

NSW – Partnership Act 1892

NT – Partnership Act 1997

QLD – Partnership Act 1891

SA – Partnership Act 1891

TAS – Partnership Act 1891

VIC – Partnership Act 1958

WA – Partnership Act 1895

Why should the Partnership Deed NOT rely on any Partnership Act?

Some Partnership Agreements from non-law firm websites rely on state-based Partnership Acts. This is wrong and lazy drafting.

Australia’s Partnership Acts are ‘permissive’. They provide a set of default rules. Legal Consolidated’s Partnership Deed completely overrides and replaces these outdated rules.

The state and territory Partnership Acts are antiquated. Most are based on a United Kingdom law from 1890. They were not designed for modern business.

For example, under these old Acts, the death or bankruptcy of a single partner automatically dissolves the entire partnership. This inflicts immediate stamp duty and Capital Gains Tax.

Further, relying on a specific state’s Act is risky for any business operating across Australia. If your Deed references the Victorian Act, what happens when you do business in Queensland? This creates legal uncertainty and potential disputes.

Legal Consolidated’s Partnership Deed is a standalone document. It contains all the rules for your partnership. This provides clarity and protection in every Australian state and territory.

Your Legal Consolidated Partnership Deed is the complete and modern rulebook for your business. It removes all reliance on these outdated and conflicting state laws, giving your partnership certainty and control.

What if I do not have a Partnership Agreement?

Are you running a business with someone else? You might be in a “partnership” in the eyes of the Australian Taxation Office (ATO), even if you do not have a formal agreement. This has serious consequences for your tax and legal obligations. An undocumented partnership is confusing and relies on handshake deals or assumptions.

Does the ATO have its own definition of a partnership?

The ATO has its own definition of a partnership, which is different to the undocumented partnership. For tax purposes, if you and at least one other person are receiving income jointly, you are likely in a tax law partnership.

However, the real confusion starts when you look at the general law.

Is Your Partnership Legally Sound? Jolley v Commissioner of Taxation

Determining whether you have a legally binding partnership is a complex issue if you do not have a Partnership Agreement. It is not as simple as just having a “partnership” ABN. The courts examine a combination of factors—a “mixed question of law and fact”—to determine if a true partnership exists.

This means both the ATO and the courts scrutinise your actions and your relationship with your business partners and third parties. The leading case, Re Raymond William Jolley v Commissioner of Taxation [1989] FCA 64, highlights this complexity. You cannot just hope you are in a partnership; you need to act like it by having a Legal Consolidated Partnership Agreement.

The ATO’s Partnership Checklist

The ATO’s own ruling, Tax Ruling TR 94/8, outlines what they look for to determine if a partnership exists. While the ATO’s view is not the final word on the general law, it is a good guide to the factors that matter.

The most important factor is your intention. Did you and your partners intend to go into business together? A written partnership agreement is the best way to prove this. While an oral agreement or a course of conduct may be sufficient, a signed, written agreement from a reputable law firm like Legal Consolidated is the gold standard.

But intention alone is not enough. Your conduct must back it up. The ATO will look for evidence like:

-

Joint Ownership of Assets: Do you own business assets together?

-

Business Name Registration: Is the business name registered in all the partners’ names?

-

Joint Bank Account: Do you have a joint business bank account that all partners can operate?

-

Active Involvement: Are all partners involved in running the business?

-

Capital Contributions: Have all partners contributed capital to the business?

-

Sharing of Profits: Are you all entitled to a share of the net profits?

-

Business Records: Do you maintain accurate and up-to-date business records?

-

Public Recognition: Do you present yourselves to the public as a partnership? This includes things like:

-

Invoices, receipts, and letterheads in the partnership name.

-

Contracts entered into in the partnership name.

-

Advertising in the partnership name.

-

The Solution: A Legal Consolidated Partnership Agreement

As you can see, the rules are complex and messy. Relying on the ATO’s interpretation or “common sense” is a risky strategy that can lead to disputes with your partners and trouble with the tax man.

A professionally drafted Legal Consolidated Partnership Agreement removes doubt. It clearly sets out your intentions and obligations, ensuring you are compliant with both tax law and general law. It makes your accountant happy by providing clear documentation and gives you peace of mind.

Do not leave your business to chance. Even if you started your partnership many years ago, build a Legal Consolidated Partnership Agreement today and protect yourself and your business partners going forward.

Do legal Consolidated partnership deeds work throughout Australia?

Yes. As a national Australian law firm, our Partnership Deed works throughout Australia.

Advanced Family Trust Training Course by Adj Professor, Dr Brett Davies

A written partnership agreement reduces the risk

Our law firm’s partnership agreement reduces the joint liability. This is between you and your other partners:

- corporate governance is encouraged by a partnership agreement

- tighter rules between parties as to loans

- better documented fiscal restraint

- warranties and indemnities to protect individual parties

Because you built a Partnership Agreement with our firm, you can seek out your rogue business partner who bought a Ferrari under the partnership and sue him.

Is a Partnership a legal ‘entity’?

Neither a partnership nor a trust is a legal ‘entity’. In contrast, a human and a company are legal entities. Nevertheless, tax records are usually prepared for a partnership (and a trust). But generally, only the partners (or beneficiaries of a trust) pay tax on the revenue.

Are Partners employees?

Partners are not employees. Key legal obligations for employees do not apply to partners for this very reason. As your information correctly states, superannuation contributions and workers’ compensation insurance are not compulsory for partners because they are not legally considered employees of the business they own. Attempting to classify a partner as an employee in the agreement could create an expectation of these benefits and cause issues with the Australian Taxation Office and state revenue authorities.

However, a Partnership can enter into a separate Employment Contract or an independent Contractor’s Agreement with a partner. Your accountant may also recommend a Service Trust Agreement.

No, you should not make partners employees in the partnership agreement because, legally, they are business owners, not employees. The two roles are fundamentally different, and mixing them in the one document creates legal and tax confusion.

The Difference: Owner vs. Employee

A partner is a business owner. They contribute capital, have a right to control the business, and are entitled to a share of the profits. An employee works for the business in exchange for a salary. You cannot be both an owner of and an employee of the same partnership at the same time. Conflating these roles in the main partnership deed undermines the legal structure of the partnership itself.

Profit Share v Salary

The distinction is critical for accounting and tax purposes:

-

Partners receive a share of the profits. This is a distribution of the business’s net earnings.

-

Employees are paid a salary or wage. This is a business expense that is deducted before calculating the net profit.

Trying to define a partner as an “employee” in the governing deed confuses their entitlement as an owner (profit) with a business expense (salary).

Can a partnership employ a partner?

However, the Partnership Agreement should not stop the partnership from entering into an employment relationship with a partner or a person related to a partner.

Employ yourself: Individuals as partners cannot ’employ’ themselves. There is no salary packaging, workers’ compensation or employer-sponsored superannuation. Instead, build an:

if a partner wants to provide services to the partnership.

A Partnership Agreement should not try to document services or products supplied via a Partnership Deed. This includes a person or business related to the partner. Instead, build separate Employment Contracts or Independent Contractors Agreements.

Advantages of a Partnership Deed

- Simple– when compared to a trust or company

- Cost less to set up – than a company or a trust (where partners are all individuals)

- Inexpensive to run – no ASIC yearly fees like a company

- Less paperwork – no reporting obligations to ASIC

- Easy to understand

- Losses flow straight to the partner – losses are distributed to the partners; in contrast, losses are trapped in a family trust, unit trust and company

- Low regulation and privacy – companies are over-regulated by the government agency ASIC. Partnerships (like trusts) are less controlled by the government

Disadvantages of a business partnership contract

- The partners are jointly and severally liable. That is, each partner is liable not only for their share of the partnership debts. But also those of the other partners. At worst, one partner is liable for the entire partnership’s debts. It is unlimited liability. Even if a person only had a 10% partner’s share, he or she is responsible for 100% of the damage arising from the negligence if the other partners do not have the means to pay.

- Unless you are a Partnership of Family Trusts, there is no asset protection for each partner.

- Changing ownership is difficult. It usually requires a new partnership deed to be established. There may be transfer (stamp) duty and Capital Gains Tax issues. This is when you move assets from one partnership to another.

- When a partner dies, a new partnership is formed. So transfer duty and CGT may operate.

What is the biggest disadvantage of a partnership in Australia?

The primary disadvantage of a partnership in Australia is the unlimited liability to which partners are exposed. Each partner is jointly and severally liable for the debts and obligations of the business, meaning the personal assets of the partners are used to settle these liabilities. This extends even to wrongful acts committed by one partner, with all other partners potentially held accountable.

This level of financial and legal exposure exceeds that found in structures like corporations or unit trusts, where personal assets are generally protected behind the corporate veil. For example, in a limited liability company, shareholders’ exposure to debt is restricted to their investment in the company’s shares, even without a formal shareholders’ agreement.

A practical illustration of this risk involves the scenario where one partner might incur substantial debts on behalf of the partnership—such as purchasing a luxury vehicle like a Ferrari under the partnership’s name—and subsequently absconds. In such cases, the remaining partners are held fully responsible for the entire debt, a situation that is unlikely in corporate structures. This stark vulnerability makes the unlimited liability of partnerships a significant consideration for potential business partners in Australia.

The worst thing about a business Partnership? They suffer joint liability

One of your business partners buys a Ferrari in the partnership name. He drives into the sunset, never to be seen again. You are liable for 100% of that Ferrari’s payment.

Liability under a partnership is unlimited. In contrast, company shareholders are not exposed to the vehicle’s debt. The shareholder’s liability is limited. (This is the case even if you do not have a Company Shareholders Agreement.)

Do Partnerships pay income tax?

Unlike companies, partnerships are not taxed in themselves. Instead, you and your business partners pay tax separately on the profits made through the partnership.

Each partner gets their income based on their percentage interest in the partnership. They then add that income to their personal tax returns. This is called the partnership ‘flow through’.

While a partnership does not pay income tax, it is still required to lodge a partnership tax return each income year.

Can partners in a partnership claim losses on their personal income tax returns?

In a company, family trust and unit trust losses are, sadly, stuck in those vehicles. It is hard to get the losses out. They are quarantined. In contrast, a partner in a partnership merely carries any losses into their personal tax return. This is highly advantageous.

A partnership distributes its net income or loss to each partner. Each partner includes their share of the partnership income or loss in their assessable income.

So, partners in a partnership in Australia can claim their share of the partnership’s losses on their personal income tax returns. However, some specific conditions and rules apply. The partnership itself does not pay tax on its income; instead, each partner includes their share of the partnership’s profit or loss in their own tax return.

Any restrictions on a partner claiming losses on their personal income tax return?

To claim a loss, partners must meet the non-commercial loss rules. These are designed to prevent individuals from using business losses to offset other income unless their business activities are deemed to have a significant commercial purpose and potential for profit. These rules include income requirements and other tests to determine whether the losses can be claimed immediately or must be carried forward to future years.

If partners meet these requirements, they can use the losses to reduce their taxable income, potentially lowering their personal tax liabilities.

How does a partner in a partnership pay income tax

For example, this financial year, your partnership generated $3 million. You currently have three partners. They have this percentage interest in the partnership:

- 33 1/3% – add $750k to their tax return

- 50% – add $1.5m to his tax return

- 33 1/3% – add $750k to her tax return

How are the profits of a partnership taxed?

The profits of a partnership are divided among the partners. Each partner is individually responsible for paying income tax on their respective share of the partnership’s profits.

Can a family trust be a partner in a Partnership Agreement?

A family trust cannot act on its own. It operates through its trustee. This applies to any trust, including a Unit Trust. A trustee can be a human or a company.

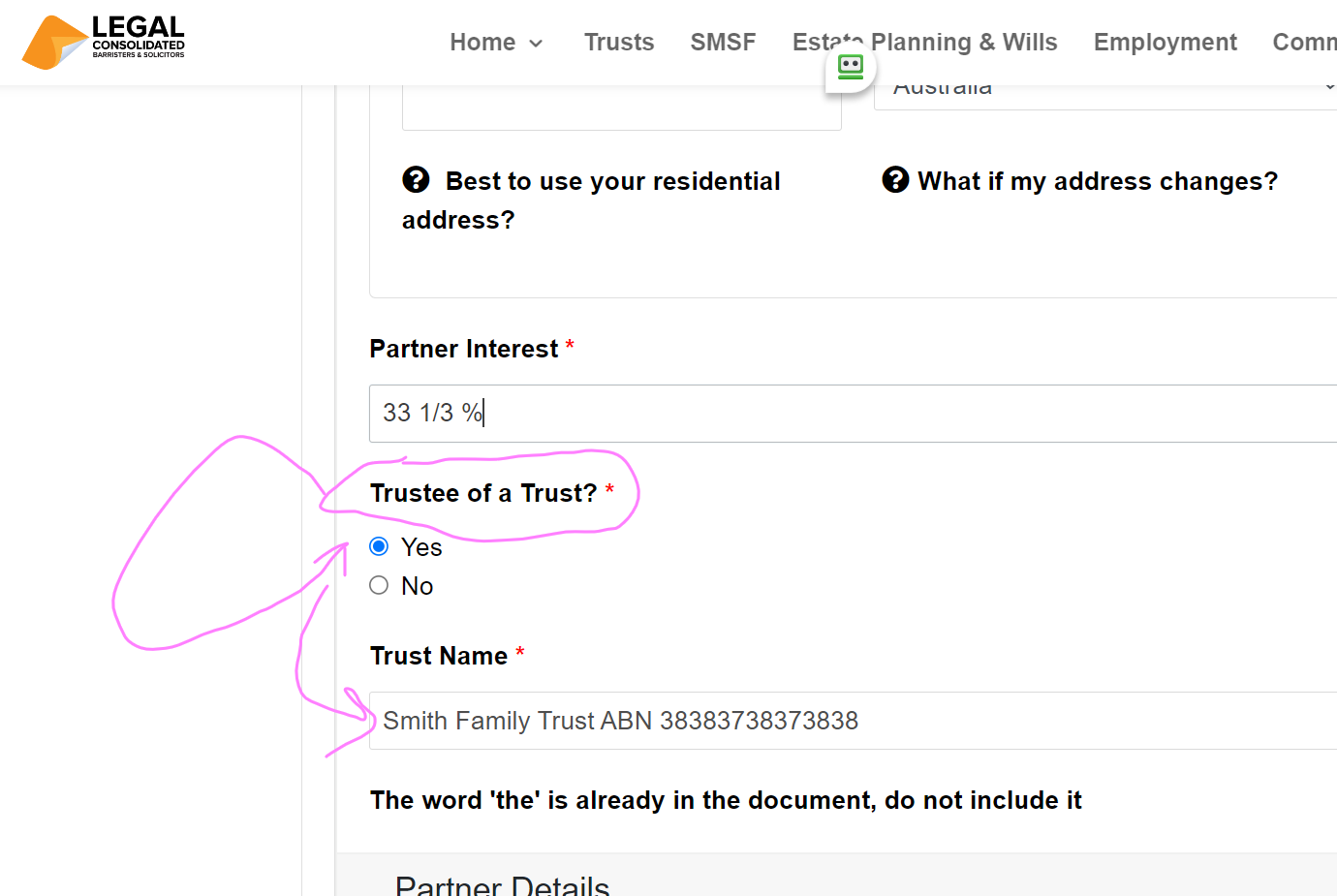

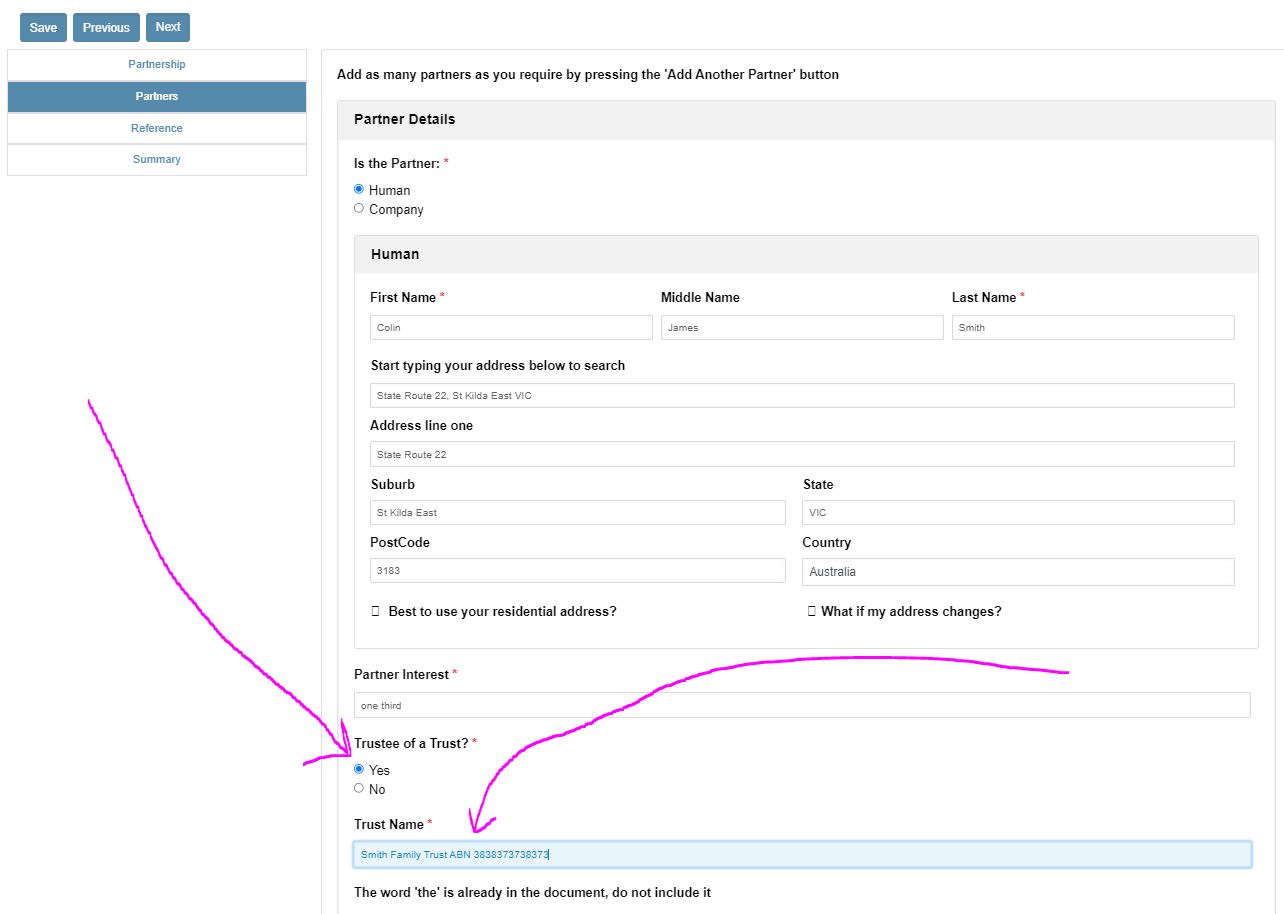

When you build your Partnership Agreement, the ‘partner’ is the trustee of the Family Trust. (It is not the Family Trust itself.) To bring notice to the world that the partner is merely acting as a trustee, press yes to the trust question.

Examples of a partner who is a trustee of a trust

Where a partner is a trustee of a trust:

- Acme Nominees Pty Ltd as trustee of the Smith Family Trust ABN 38383738373838

- Company Name (do not forget to add “Pty Ltd”)

Acme Nominees Pty Ltd - Company ACN (Australian Company Number)

123456789 - Trustee of a Trust?

Yes - Trust Name

Smith Family Trust ABN 38383738373838

- Company Name (do not forget to add “Pty Ltd”)

- Colin James Jeffereris as trustee of the Downton Family Trust ABN 383733049484847

-

James

-

Jeffereris

- Trustee of a Trust?

Yes - Trust Name

Downton Family Trust ABN 383733049484847

- Poplar Pty Ltd as trustee of the 23 Poplar Street Unit Trust ABN 876787678654

- Company Name (do not forget to add “Pty Ltd”)

Poplar Pty Ltd - Company ACN (Australian Company Number)

123456789 - Trustee of a Trust?

Yes - Trust Name

23 Poplar Street Unit Trust ABN 876787678654

- Company Name (do not forget to add “Pty Ltd”)

Is a Partnership a separate legal entity?

A partnership is not a separate legal entity. A human and a company are separate legal entities. However, trusts and Partnerships are not separate legal entities. However, the business partnership has its own Tax File Number (TFN). Each financial year, the partnership lodges a type of tax return. This is called a partnership tax return. Each partner is then taxed separately on their share of the profits.

Your partnership has its own TFN but does not pay income tax on the profit it earns.

Does a Partnership have its own Australian Business Number (ABN)

Speak to your accountant, as most partnerships are required to apply for an Australian Business Number (ABN). This is if they are carrying on an ‘enterprise’. This includes running a business for profit.

Does a Partnership have to register for its own GST?

The Partnership may also be required to register for the Goods and Services Tax (GST).

My Partnership started many years ago. Can I backdate the Partnership Agreement?

Many successful businesses start informally. Only later, as the business grows, do you realise the need for a written Partnership Agreement. But what if your partnership has already been operating for years?

It is illegal to backdate any legal document, whether it be a Family Trust Minute or Partnership Agreement. A contract is effective from the day it is signed and dated by all parties. Building a document today but dating it in the past is fraudulent and has severe legal consequences.

Is It Too Late to build a Partnership Deed for an existing partnership?

It is never too late. Even if your partnership has been operating for many years, build a Partnership Agreement today. A properly constructed agreement provides a legal “line in the sand,” replacing ambiguity with certainty from this point forward.

How Does a New Partnership Agreement Acknowledge the Past?

While the Partnership Deed is dated today, a Legal Consolidated Partnership Agreement is uniquely drafted to solve this problem. Our Partnership Agreement includes special clauses that ratify and confirm the past conduct and state of the partnership. This provides a clear, legal foundation for the future and prevents disputes about what was agreed upon “back then.”

Does the Partnership Agreement Document What We Own?

The answer is no. A Partnership Agreement is not the correct place to list business assets. Your balance sheet, prepared by your accountant each year, is the document that tracks the partnership’s assets and liabilities. Our Partnership Agreement is carefully designed to work seamlessly with the financial reporting prepared by your accountant.

How do I protect the Partnership from a departing Partner?

The single biggest threat to your business may be your own partner. Imagine this: your partner, who knows all your clients, trade secrets, and pricing, suddenly leaves. The following week, they open a competing business across the street, poaching your best clients and staff. Your business, which you have spent years building, is critically damaged overnight.

All partnership agreements should contain a Restraint clause.

‘Restraint of Trade’ in a Partnership Agreement

Your Legal Consolidated Partnership Deed is built with a powerful Restraint of Trade clause. This is your shield against a departing partner causing irreparable harm. It is a legally binding promise that, for a reasonable period after leaving, an ex-partner cannot:

-

Set up a Competing Business: Prevents them from opening a similar business in your local area, protecting your market share.

-

Steal Your Clients: Legally prevents them from soliciting the clients they built relationships with while working in your Partnership.

-

Poach Your Team: Safeguards your most valuable assets—your employees—by preventing a departing partner from enticing them away.

When you build a business, you are building goodwill. That goodwill has immense value. A Restraint of Trade clause protects the value of the business for the partners who remain. It ensures that a partner cannot simply walk away with a portion of that value without consequence.

Difference between a Partnership and a Joint Venture

Partnership – shares profit

- A Partnership shares profits or losses between its members. E.g. we made $500k in profit. Now we share that according to our Partnership Interest. (e.g. 1/3rd to me and 2/3rds to you)

Joint Venture – shares output

- A Joint Venture shares output. For example, we obtain oil and gas from the mining site. As agreed, you get the oil. And I get the gas. We take the output. (We do not share or take income or profit.)

Like a partnership, a joint venture is a relationship between two or more parties.

Joint venturers work together. So do partners in a partnership.

But unlike a partnership, each party retains its separate identity.

A joint venture is often formed for a specific one-time purpose.

And, therefore, unlike a partnership, joint ventures often have a short life. These are frequently short-term or one-off projects.

In a partnership, you carry on an ongoing business. A joint venture is more likely to be a single or isolated transaction.

In a partnership, you are jointly liable. But in a joint venture, liability is usually several rather than joint.

Similarly, one party does not have the capacity to bind another joint venturer.

Tax returns for a Partnership vs a Joint Venture

A partnership doesn’t pay tax on its income. Instead, each partner pays tax on its share of the partnership’s net income. However, in a partnership, you still prepare a partnership tax return. The partnership tax return is lodged with the Australian Taxation Office each year

In contrast, there is no requirement to prepare income tax returns for the joint venture.

The five differences between a joint venture and a partnership

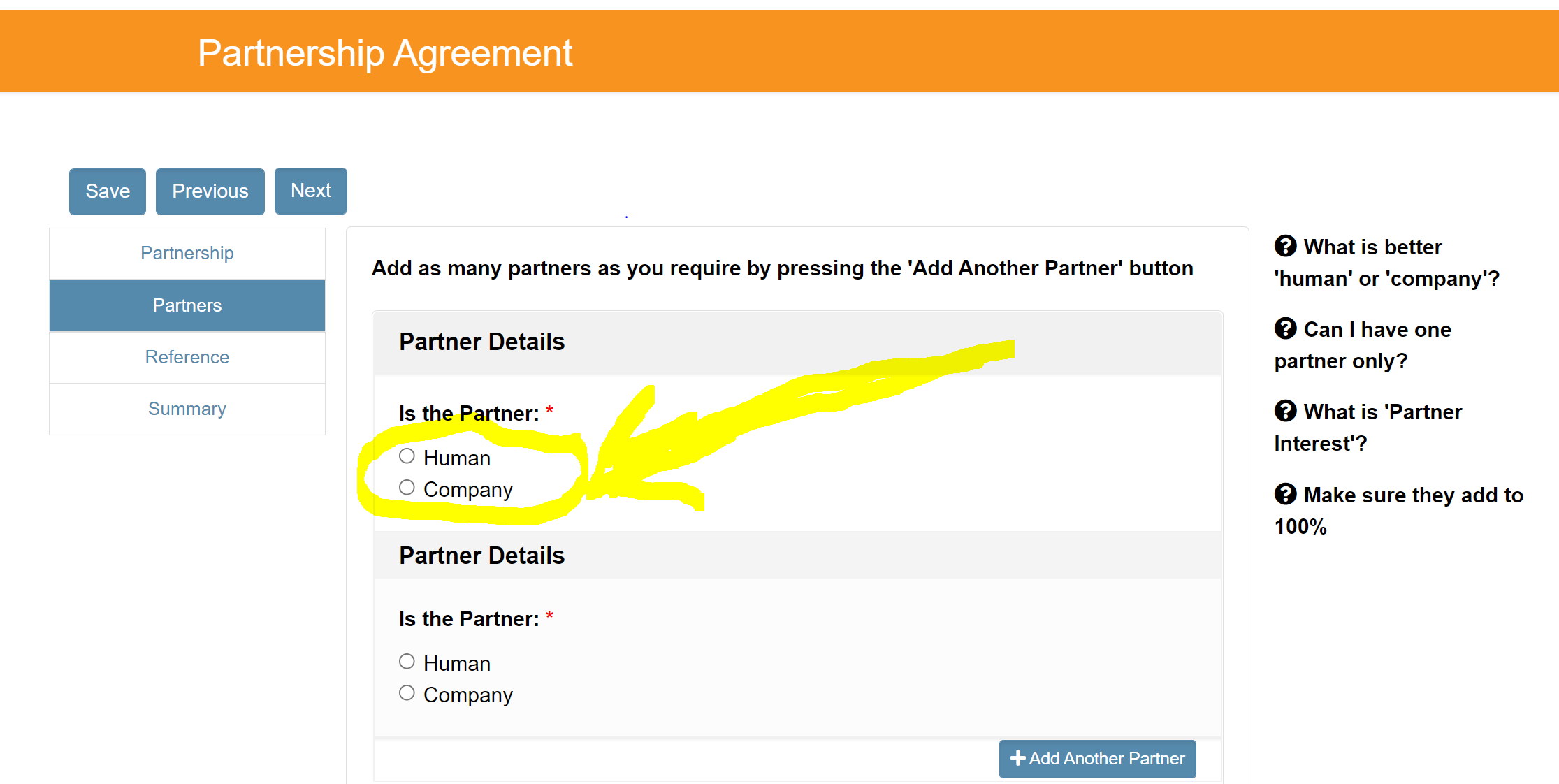

Can the partners be a combination of companies, humans and trusts?

Partners in a partnership deed are typically individuals (humans) or corporate entities (companies). Trusts, however, cannot directly be partners because they operate through trustees. A trustee, who may be either an individual or a corporate entity, acts on behalf of the trust. Therefore, when a trust is involved in a partnership, it participates indirectly through its appointed trustee. Examples of such arrangements include:

Hence, if a trust is to enter into a partnership, it must do so through its trustee, who is recognised as the partner in legal terms. This arrangement ensures that all legal and financial responsibilities are clearly defined and managed by the trustee on behalf of the trust.

If a family trust, bare trust or unit trust wants to own an interest in a partnership, then it does so through its ‘trustee’.

The trustee of the trust holds the partnership interest under the Partnership Deed. But this interest in the partnership is held in trust for the trust. The trustee is not the true or beneficial owner. Instead, the true owner is the trust. The trustee is just the ‘legal’ owner. The ‘beneficial’ owner is the trust. So even though the partnership interest is in the trustee’s name, the true owner is the trust. For example:

1. Example of a human as trustee of a trust holding an interest in a partnership

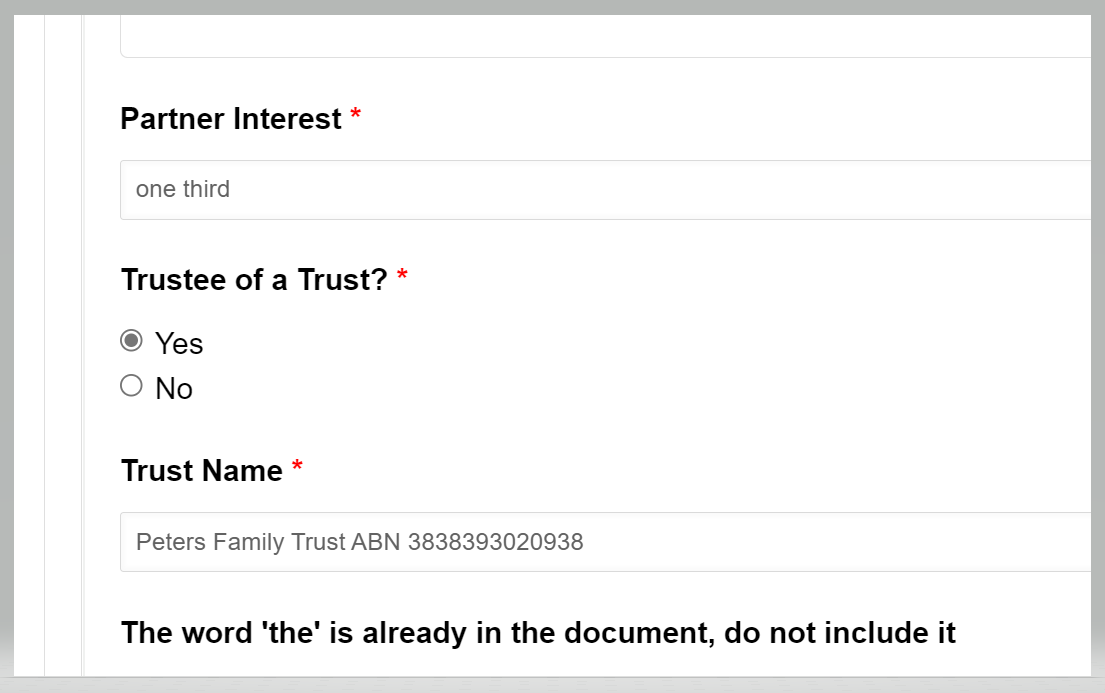

Colin is the trustee of the Peters Family Trust. The Peters Family Trust will be a partner in a new Partnership Agreement. But Family Trusts (like all trusts) can only operate through a trustee. Therefore, although the true or beneficial owner is the Peter Family Trust, the trustee, being Colin, holds the legal ownership of the partnership interest. E.g. Colin holds a one-third interest in the Partnership in trust for the Peters Family Trust ABN 3838393020938.

Even though the partnership interest is held in Colin’s name, the trust is the beneficial owner. The Family Trust is responsible for the income that comes from the partnership. Colin does not pay tax on the partnership income. The Peters Family Trust is responsible for the partnership income.

2. Example of a company as a trustee holding an interest in a partnership

Koko Nominees Pty Ltd is the trustee of the Koko Family Trust. The Koko Family Trust is going to take up an interest in a partnership. But trusts cannot hold assets in their own name. Trusts operate through ‘trustees’. A trust needs a trustee. The trustee holds the assets on trust for the family trust. In this instance, the partnership interest is owned by Koko Nominees Pty Ltd atf the Koko Family Trust.

Example of a partnership that has partners who are companies, humans and trusts:

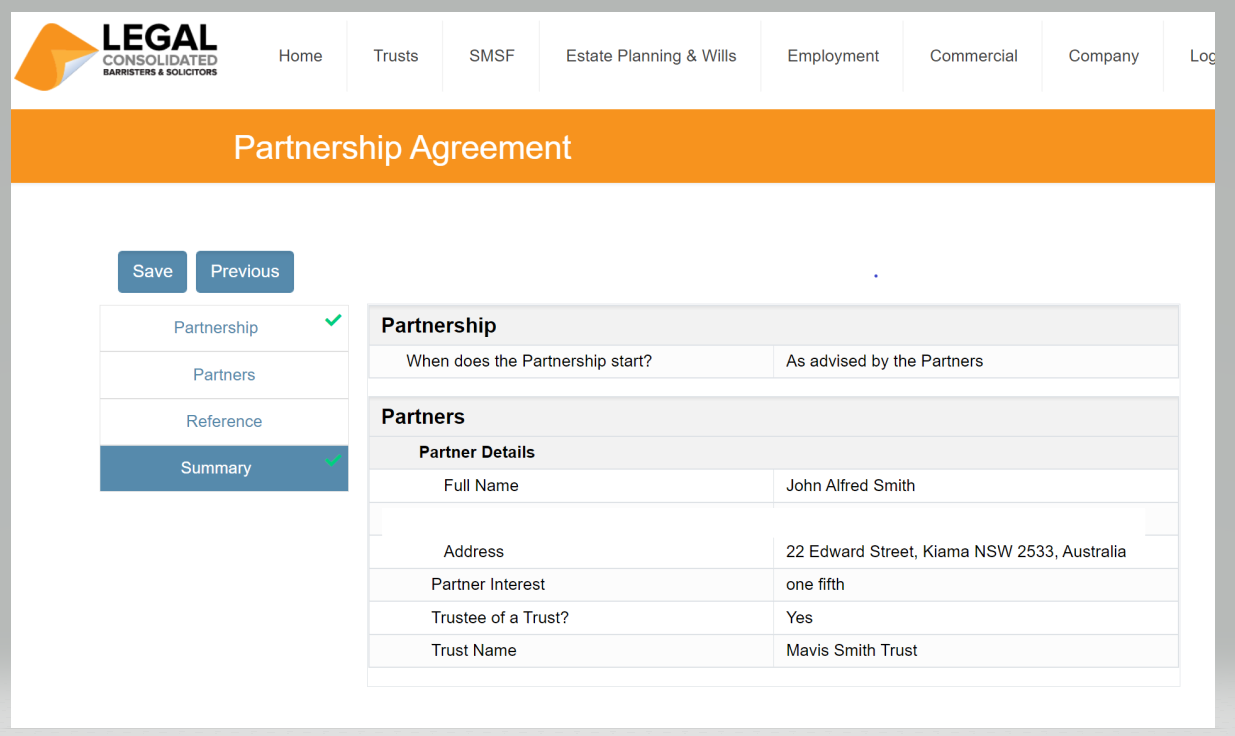

- John Alfred Smith (holding his interest as bare trustee for his mother Mavis) – 25%

- Mary Chan – 20%

- Cologne Nominees Pty Ltd (as trustee of the Cologne Family Trust) – 30%

- Fighting Fit Pty Ltd – 25%

In this example, Mary and Fighting Fit Pty Ltd hold their interest in the partnership for themselves – absolutely. They are both the ‘legal’ and ‘beneficial’ owners.

But John and Cologne Nominees Pty Ltd are only ‘legal’ owners. They only hold the partnership interest as trustees. They hold their respective partnership interests on trust for the beneficial owner.

How to build a Partnership of family trusts

A partnership owns an asset or business. The partners share the ‘profit’. That all sounds good. But there is ‘joint and several liability’. If one partner makes a mistake, all other partners are liable 100% each for that mistake. The Legal Consolidated Partnership Deed seeks to reduce that risk. But that only works up to a point.

Another way to reduce the effects of ‘joint and several liability’ is having a partnership of family trusts. (A ‘family trust’ and a ‘discretionary trust’ are the same thing.) Instead of having a group of individuals or companies as partners, each partner is a Trustee of a Family Trust. Each partner in the partnership is a family trust.

If the Partner holds the Partnership Interest for another person or in trust, then:

1. Press ‘yes‘.

2. Type in the name of the trust. And also type in the ABN if the trust has one.

What is a partnership of discretionary trusts?

A partnership of discretionary trusts is a partnership structure where each partner is a trustee of a discretionary trust, often called a family trust. This structure contrasts with a typical partnership of individuals. In the latter, individuals themselves enter the partnership directly. In a partnership of discretionary trusts, however, it is the trusts that are represented in the partnership through their trustees.

In such arrangements, trustees—who may be individuals or companies—act on behalf of the trusts to manage their obligations and entitlements within the partnership. This setup separates personal and trust liabilities and assets, providing an extra layer of legal and financial protection for the trustees. It is better asset protection.

Further, a partnership of discretionary trusts also includes other types of partners, such as individuals or corporate entities, broadening the scope and versatility of the partnership. Under the Legal Consolidated Partnership Deed, this flexibility is legally permissible and can be strategically advantageous for managing diverse assets and investments across different entities within the same partnership framework.

Example of a Partnership of Family Trusts

Each partner has its own Family Trust. For asset protection, they likely use the Family Trust as a partner in this partnership. They probably would not use the Family Trust for other purposes. The three partners are:

- Kale Nominees Pty Ltd is the trustee of the Smith Family Trust. (Corporate trustee)

- Modern Kay Pty Ltd is the trustee of the Jones Family Trust. (Corporate trustee)

- Mary Bikic is the trustee of the Mary and Colin Family Trust. (Human trustee)

(It is strange that Mary (a human) is the trustee of this particular Family Trust. The partnership of a family trust structure is to protect individuals from exposure to a failed business. It is an asset protection strategy.

Sure, humans are often trustees of family trusts. However, this is usually only the case if the Family Trust is a ‘safe house‘. Perhaps Mary has no assets. She may be following the ‘woman of straw and man of structure‘ asset protection strategy.)

So, for example, the first partner, Kale Nominees Pty Ltd, holds its interest in the partnership on trust. This is for the family trust called the Smith Family Trust.

The 3 partners of the partnership are Kale Nominees Pty Ltd, Modern Kay Pty Ltd and Mary Bikic. That is what the world sees when the partnership transacts with others.

Asset Protection in a Partnership of Family Trusts

Yes, each family trust, as a partner, remains ‘jointly and severally’ liable for partnership debts. However, the only asset the family trust owns is a percentage interest in the partnership. So if the partnership goes down, you do not lose any of your other assets. Your non-partnership assets and personal assets are protected.

Tax Benefits of a Partnership of Family Trusts

Share the Partnership profit with family: If you personally own an interest in the partnership, then all income you get, you pay tax on. You cannot share that tax burden with your spouse or family. However, they may be subject to lower marginal tax rates. And you do not want to ‘waste’ those lower tax rates.

In contrast, the family trust distributes its percentage of the partnership profit as it sees fit. It can be distributed to your son this financial year, who is on maternity leave and is on a low tax rate. Next year, the family trust will distribute the partnership profit to just your spouse.

The trustee of each trust distributes the trust’s share of the partnership income among the trust’s beneficiaries as it wishes.

Three disadvantages of a partnership of discretionary trusts

A partnership of family trusts faces three challenges:

- It is more complex than a partnership, company or family trust. (Like LEGO® pieces, to end up with a partnership of family trusts you bolt these entities on top of each other to get your partnership of family trusts).

- It is expensive to set up. Each partner needs both a corporate trustee and a family trust deed.

- While financial planners, finance brokers and accountants understand the structure, less qualified people, such as bankers and government departments, may not understand how they operate.

How to set up a partnership of family trusts

- Build a company (to be the trustee of a family trust)

- Build a family trust (make the company the corporate trustee)

- Repeat the above two steps for each partner

- Build the Partnership Deed by pressing the blue Start Building button above. Each partner is the trustee of the family trust

Example of a partnership of discretionary trusts

John, Fred and Muriel want a partnership of family trusts. John incorporated a company on Legal Consolidated’s website called “John Australia Nominees Pty Ltd”. Once he gets the Certificate of Incorporation of the company, he builds a family trust. He calls the family trust ‘Avis Family Trust’ after his dead grandfather’s name. (John can call his family trust anything he likes.) Fred and Muriel do the same.

Now, with the three companies, they then build a Partnership Deed. The three partners are the three companies. “John Australia Nominees Pty Ltd” and Fred and Muriel’s companies.

Company vs partnership of family trusts

For a business between strangers, commonly, your accountant recommends one of three structures:

- Unit Trust; or

- Company to operate in its own right; or

- a partnership of family trusts

This is where the business is more than one family. If it is just Mum and Dad running the company, then you only need a corporate trustee for a family trust.

Income. It is often easier to distribute tax-free (pre-tax dollars) through a partnership of discretionary trusts and unit trusts. This is compared to a company.

Tax relief on sale. It is also easier for the partners of a partnership of trusts and Unit Trust to access concessional capital gains tax (CGT) treatments. This includes the small business CGT concessions. This is compared to a company.

Independence. Each partner’s trust is effectively independent of the others. It is even possible to have partners that are not discretionary trusts, such as unit trusts, companies and humans.

Australian Farming Partnership structures

Traditionally:

- Family land is purchased in Family Trusts and Unit Trusts. This is with a corporate trustee.

- In contrast, the day-to-day farming operations are carried out through a (trading) partnership. E.g. mum, dad and the children that remained on the farm.

Example of a farming partnership

The four farming blocks have been purchased over the last 55 years. This is the name of four separate Family Trusts. Each has its own corporate trustee for asset protection. Or the farming lands are purchased in a Unit Trust (with a special type of Unit Trust corporate trustee) if the children become part owners of the farm earlier than their parents’ death. (We do not recommend that. The children get it soon enough when you are dead. No point rushing it.)

Everyone working on the farm, along with their spouses, is made a partner. Or they each form a Family Trust. And their Family Trust becomes one of the partners.

The Partnership leases the property from the Family Trusts. This is via a Lease Agreement. The Lease fee is often just a peppercorn rent, for example $10,000 per year.

When one of the farmers dies, the old Partnership is dissolved. And you build a new Partnership Deed. And whoever is left, plus the grandchildren who are interested in coming on, sign the new Partnership Agreement.

In other words, when people exit partnerships, either through death or retirement, or enter partnerships, such as through the addition of new partners like spouses and children, the old partnership dissolves and a new one is created.

Farming trusts generally own few assets

Apart from a header and a few trucks, there are generally no assets of value in the partnership. Therefore, there is no CGT and very little stamp duty on the transfer from one Partnership to the next over the following 200-300 years.

You do not put into the farming trading partnership:

- off-farm assets (e.g. homes in the city)

- the farming land itself

Which primary producers use partnerships?

This is the standard way your accountant and adviser set up your structure. This is true no matter what primary production you engage in:

- Broadacre cropping

- Intensive livestock farming

- Dairy

- Fishing

- Viticulture

- Horticulture

- Aquaculture

Running a farm? Partnership vs company

Rather than a partnership, why not trade via a company?

However, companies have poor structures in which to conduct farming business. They are not eligible for a range of primary production concessions:

- cannot use Financial Risk Management strategies – FMDs

- are ineligible for primary production averaging

Plus, farming companies suffer income tax issues:

- You cannot stream income

- For you cannot stream CGT to one person, imputation credits to another, and income tax to a third person

- companies pay tax at a rate of up to 30 cents on the dollar

- If the company is of a size where it is a base rate entity, the company tax rate is 25%. This applies to most family-run businesses: https://www.ato.gov.au/rates/

changes-to-company-tax-rates/

- If the company is of a size where it is a base rate entity, the company tax rate is 25%. This applies to most family-run businesses: https://www.ato.gov.au/rates/

- do not easily get Capital Gains Tax relief

- loans restrictions on loans to shareholders and their associates

However, companies can be helpful as trustees of your Family Trust and Unit Trust. As a mere corporate trustee, the company does not trade in its own right. It trades on behalf of the trust structure and trust beneficiaries.

Tax File Number, GST, ABN and bank accounts for an Australian Partnership

A Partnership Agreement is a contract. It governs a business relationship between two or more individuals (or corporations) that are working together.

A partnership is not a separate legal entity. It is not like a company. But it still has a tax file number (TFN). A Partnership, while not usually paying tax itself, still lodges a yearly tax return. Instead, each partner is taxed separately on their share of the profits.

A partnership is entitled to an Australian business number (ABN) if it is carrying on an enterprise in Australia. For example, running a business for profit comes within the definition of enterprise in the GST Act.

Your partnership (just like a trust) is not a separate identity for tax. However, you may still need to register for TFN, GST, ABN and PAYG. You can do this for free on the ATO website.

After a Partnership deed is signed, a partnership bank account is opened.

Does the Partnership Agreement mention AASB 15 “Revenue from Contracts with Customers”?

As of 1 July 2021, non-listed companies are no longer allowed to prepare Special Purpose Financial Statements (SPFs). Instead, they prepare the arduous General Purpose Financial Statements (GPFS). Small proprietary companies where 5% of their shareholders request GPFS to be ready are included in the definition of companies that comply with this requirement.

This requirement also applies to SMSFs, Trusts, and Partnerships, but only where the founding Deed makes mention of AASB 15 in its definition of income.

Happily, Legal Consolidated documents do not reference AASB 15 in the definition of income.

Further, no Legal Consolidated documents require compliance with the arduous AASB 15.

Free legal advice when building your Partnership Deed

Legal Consolidated does not give legal advice on which business structure is best for you. That is a question that your accountant and financial planner should consider. They know your circumstances. We do not know your circumstances.

Start building your Partnership Deed for free on our law firm’s website. Read all the free hints. Educate yourself. When you have answered as many questions as possible, you or your adviser can telephone us to review and discuss your answers. However, please start the Partnership building process before contacting the law firm.

Partnership vs Other Business Structures

Partnership Agreement vs Family Trust

- Family Trust Deed – watch the free training course

- Family Trust Updates:

- Everything – Appointor, Trustee & Deed Update

- Deed ONLY – only update the Deed for tax

- Guardian and Appointor – only update the Guardian & Appointor

- Change the Trustee – change human Trustees and Company Trustees

- The company as Trustee of Family Trust – only for assets protection?

- Bucket Company for Family Trust – tax advantages of a corporate beneficiary

Partnership Agreement vs Unit Trust

- Unit Trust

- Unit Trust Vesting Deed – wind up your Unit Trust

- Change Unit Trust Trustee – replace the trustee of your Unit Trust

- Company as Trustee of Unit Trust – how to build a company designed to be a trustee of a Unit Trust

Partnership Agreement vs Corporate Structures

- Incorporate an Australian Company – best practice with the Constitution

- Upgrade the old Company Constitution – this is why

- Replace lost Company Constitution – about to get an ATO Audit?

Partnerships vs Independent Contractors Agreements

- Independent Contractor Agreement – make sure the person is NOT an employee

- Service Trust Agreement – operate a second business to move income and wealth

- Law firm Service Trust Agreement – how a law firm runs the backend of its practice

- Medical Doctor Service Trust Agreement – complies with all State rules, including New South Wales

- Dentist Service Trust Agreement – how dentists move income to their family

- Engineering Service Trust Agreement – commonly engineers set up the wrong structure

- Accountants Service Trust Agreement – complies with ATO’s new view on the Phillips case