Why refusing an inheritance destroys Age Pension planning

Take Mary as an example. Mary’s financial planner works hard to preserve her small Age Pension and the valuable Pensioner Concession Card.

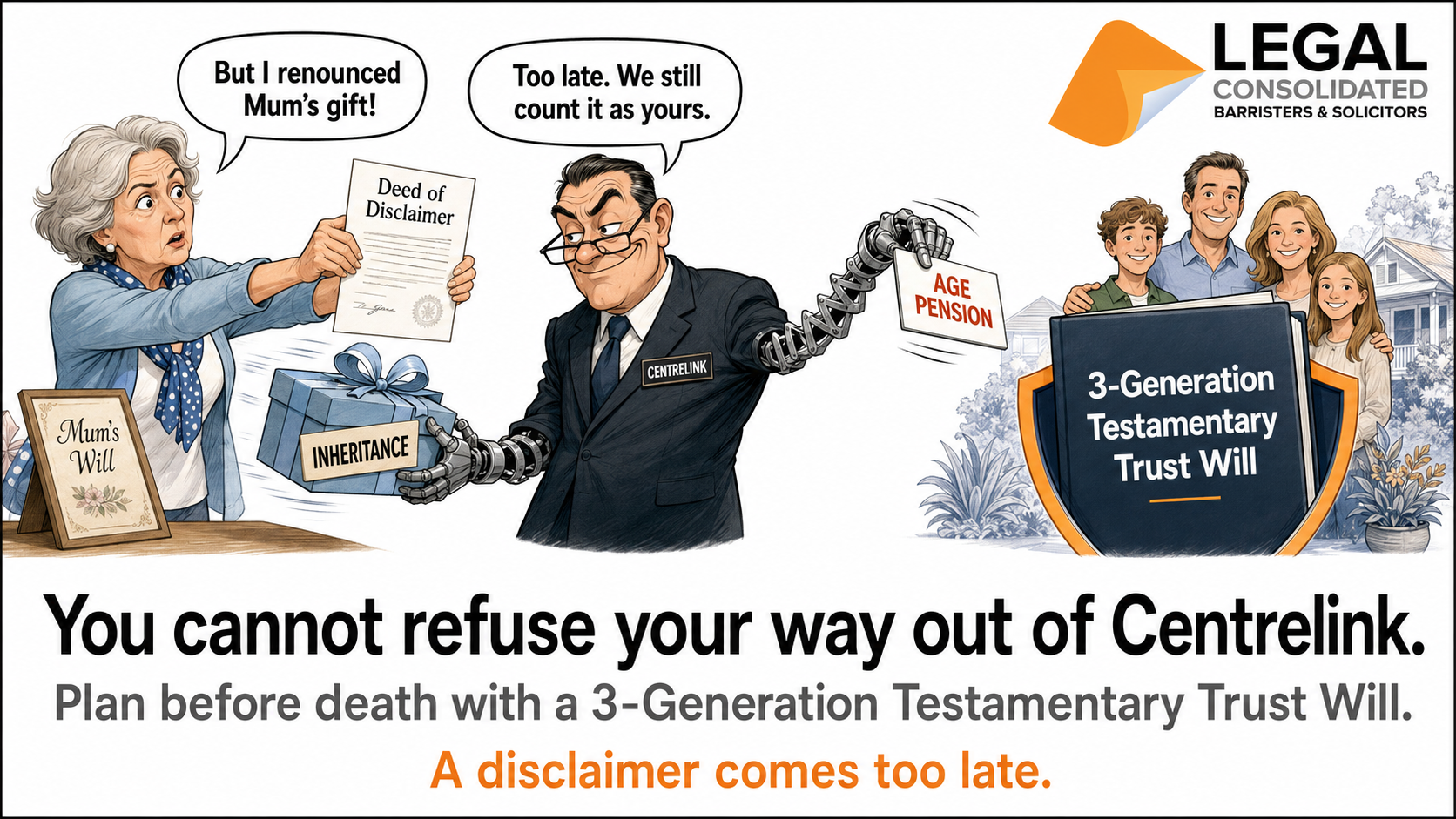

Mary’s mother dies and leaves the estate to Mary. Centrelink does not wait for Mary to transfer the assets into her name or bank account. Once Mary can receive the inheritance, Centrelink counts it as her asset. She loses her Age Pension and Pensioner Concession Card.

Mary does not need the money. She wants her children to receive it.

Mary signs a Deed of Disclaimer before Probate. Under a standard bloodline gift-over clause, Mary’s children receive the inheritance.

The disclaimer works under succession law. But it fails under Centrelink’s deprivation rules.

Does Centrelink treat a disclaimed inheritance as a gift?

Yes. Centrelink treats a disclaimed inheritance as a gift for means-testing purposes.

The deprivation rules apply where a beneficiary:

- waives the right to an interest in a deceased estate;

- directs the executor to distribute the interest to another person; or

- gives the interest to another person after the estate is finalised.

The deprivation rules apply where the beneficiary receives no consideration, or inadequate consideration, for giving up the inheritance.

Department of Social Services, ‘Deprivation Related to Deceased Estates, Superannuation Funds and Separation’, Social Security Guide [4.1.5].

The statutory deprivation rules sit in the Social Security Act 1991 (Cth) pt 3.12 div 2, especially ss 1123–1124 and ss 1126AA–1127.

When does Centrelink count an inheritance?

Centrelink does not count the inheritance from the date of death. The beneficiary’s interest in the deceased estate is an assessable asset, but the law exempts it until the beneficiary receives it or is able to receive it. For example, the Will could be challenged.

Centrelink generally allows up to 12 months to administer the estate after the Will maker dies. If the estate is finalised earlier, Centrelink assesses the inheritance from the date the beneficiary receives it or is able to receive it.

If the estate remains undistributed after 12 months, Centrelink examines the cause of the delay. Where the beneficiary contributes to the delay, Centrelink treats the inheritance as available.

Department of Social Services, ‘Assessing Interests in a Deceased Estate’, Social Security Guide [4.6.5.80]; Social Security Act 1991 (Cth) s 1118(1)(j).

Does signing a disclaimer before Probate avoid Centrelink?

No. Signing the Deed of Disclaimer before Probate or before the estate is administered does not escape Centrelink’s deprivation rules.

Centrelink does not wait for the executor to transfer the inheritance into the beneficiary’s name or bank account. It looks at the interest the beneficiary gave up.

If Mary signs the disclaimer before she is able to receive the inheritance, Centrelink fixes the date of disposal as the later of:

- the date Mary signs the disclaimer; and

- the date Mary would have been able to receive the inheritance.

Delaying Probate does not turn a deprived asset into a protected asset. Avoiding physical receipt of the inheritance does not help either.

See the Department of Social Services, ‘Deprivation Related to Deceased Estates, Superannuation Funds and Separation’, Social Security Guide [4.1.5].

How long does Centrelink count a refused inheritance?

Centrelink still counts the inheritance you gave up for five years. During those five years, Centrelink still deems you to have recieved income on the inheritance as well.

Does a Deed of Family Arrangement avoid Centrelink gifting rules?

Renouncing is generally one person saying they do not want something. A Deed of Family Arrangement is where other members of the family get together to amend the dead person’s Will. A Deed of Family Arrangement changes how the estate passes. It does not erase the value that a beneficiary gives up.

If Mary agrees that her inheritance passes to her children and receives nothing of equal value in return, Centrelink treats her as disposing of the inheritance.

Centrelink does not care. The result does not change merely because:

- all beneficiaries agree;

- the executor agrees;

- the children receive the money directly from the estate;

- Mary never deposits the money into her bank account; or

- lawyers record the arrangement in a deed.

Centrelink looks at Mary’s enforceable interest in the estate. The name of the deed does not change the deprivation rules.

How does Centrelink treat a genuine estate settlement?

But what if there is a genuine attempt to challenge the Will? A genuine settlement of a bona fide estate claim is different. Centrelink treats the reduction as supported by adequate consideration where the executor accepts another bona fide claim against the estate and the beneficiary agrees not to sue over the reduction in the beneficiary’s inheritance.

Evidence remains critical. Centrelink expects material showing that the claimant held a reasonable prospect of success. That evidence often includes a legal opinion, mediation records or documents from an independent dispute resolution process.

Do not manufacture an estate dispute to preserve the Age Pension. That is litigation bait. It also leads to legal complications, tax costs, duty and family conflict.

Department of Social Services, ‘Deprivation Related to Deceased Estates, Superannuation Funds and Separation’, Social Security Guide [4.1.5].

How does a 3-Generation Testamentary Trust preserve Age Pension planning?

A disclaimer and Deed of Family Arrangement comes too late. The planning must occur while the Will maker is alive.

Without a 3-Generation Testamentary Trust Will your beneficiaries:

- suffer the Centrelink deprivation rules and lose their pensions

- suffer death taxes

- pay 32% tax on your Superannuation

- lose your money if they divorce or go bankrupt

Instead of leaving the inheritance directly to Mary, build a 3-Generation Testamentary Trust Will. It gives the beneficiaries the power to escape the deprivations rules.

The trust gives the trustee protective machinery sitting ready to use. It provides control levers that a direct gift does not provide.

Who controls a testamentary trust for Centrelink?

Centrelink looks beyond the names written in the Will. It examines who holds effective control of the trust.

Centrelink considers:

- who appoints and removes the trustee;

- who vetoes the trustee’s decisions;

- who directs or influences the trustee;

- who changes the trust rules;

- who supplied the trust assets;

- the beneficiary’s associates; and

- who receives the practical benefit of the trust.

If Mary controls the testamentary trust, Centrelink attributes the trust’s assets and income to her. The Will and the family’s conduct must tell the same story.

Department of Social Services, ‘Determining a Controlled Private Trust’, Social Security Guide [4.12.1.20]; ‘Testamentary Trusts’, Social Security Guide [4.12.3.30]; Social Security Act 1991 (Cth) ss 1207C, 1207P, 1207V and 1207X.

A pensioner named in an existing Family Trust faces a different problem. The trust deed, control positions, tax consequences and duty consequences require review before building a Family Trust Update to exclude the pensioner as a beneficiary.

Does appointing an accountant as Appointor avoid Centrelink?

No. Appointing the beneficiary’s accountant, financial planner or lawyer as Appointor does not, by itself, solve the Centrelink problem.

Where a professional acts as Appointor, Centrelink generally attributes control to the person who instructs that professional about the trust. If Mary tells the professional what to do, Centrelink follows the instructions back to Mary.

The control separation must be genuine. The adviser’s name on the document does not protect Mary where she still pulls the control levers.

Department of Social Services, ‘Determining a Controlled Private Trust’, Social Security Guide [4.12.1.20].

Why does a non-tax-effective Will create an Age Pension trap?

A financial planner may work for years to preserve a client’s Age Pension and Pensioner Concession Card. A brittle direct gift in a non-3-Generation Testamentary Trust Will undoes that work when the inheritance becomes assessable.

The accountant builds the tax structure. The financial planner builds the financial strategy. The 3-Generation Testamentary Trust Will preserves that work.

A direct gift leaves the pensioner beneficiary with two bad choices:

- accept the inheritance and lose the Age Pension; or

- refuse the inheritance and face Centrelink’s deprivation rules.

A 3-Generation Testamentary Trust Will gives the trustee protective machinery sitting ready to use. It also protects estate wealth where a beneficiary:

- receives Centrelink;

- needs a Divorce Protection Trust because of divorce or separation;

- needs a Bankruptcy Trust because of bankruptcy;

- qualifies for a Special Disability Trust;

- is under 18 years of age;

- is a spendthrift; or

- does not need an immediate distribution.

The trustee must administer the trust properly. No Will overrides the Social Security Act 1991 (Cth).

Build Centrelink flexibility into the Will before death

Once the Will maker dies, the planning window is closed. The beneficiary may reject the inheritance, but the beneficiary cannot force Centrelink to ignore the value given away.

The Legal Consolidated 3-Generation Testamentary Trust Will builds the flexibility into the Will before death. It does not rely on a post mortem disclaimer after death.

The Will contains protective machinery for Centrelink, divorce, bankruptcy, vulnerable beneficiaries, capital protection and tax flexibility. The machinery sits dormant until the family needs it.

Start the free educational building process. No credit card is required.

- Press START BUILDING FOR FREE.

- Answer the questions one page at a time.

- Read the free legal hints.

- Watch the free training videos.

- Review your answers.

- Press LOCK & BUILD when you are ready to purchase.

You receive the completed legal documents and the law firm’s cover letter within minutes.

START BUILDING FOR FREE: COUPLES ESTATE PLANNING BUNDLE

The Couples Estate Planning Bundle suits married couples, de facto couples and life partners. It includes two 3-Generation Testamentary Trust Mirror Wills and four Powers of Attorney.

START BUILDING FOR FREE: SINGLES ESTATE PLANNING BUNDLE

The Singles Estate Planning Bundle suits single, separated, divorced and widowed Will makers. It includes one 3-Generation Testamentary Trust Will and two Powers of Attorney.

Related Centrelink estate planning guides

Centrelink problems also arise through Family Trusts, company debts, family loans and Powers of Attorney. These Legal Consolidated guides explain the related risks and legal documents.

- Remove a Centrelink beneficiary from a Family Trust

- Why Centrelink attacks grandparents named in Family Trusts

- Can a beneficiary disclaim a Family Trust distribution?

- Forgiving a company debt to obtain the Age Pension

- Special Disability Trusts and Centrelink deprivation

- Documenting loans from children to parents

- Build an Enduring Power of Attorney

- Build a Company Power of Attorney

- Build a 3-Generation Testamentary Trust Will

Written by Adjunct Professor Dr Brett Davies, Partner, and Madeleine Baxter, Solicitor, Legal Consolidated Barristers & Solicitors.