Different classes of company shares in Australia: why share rights matter

A company share is a bundle of rights. Those rights decide who:

- votes

- receives dividends

- gets back capital

- gets notices

- attends meetings

- participates if the company is wound up

This is why the company constitution matters. The constitution gives each class of shares its legal shape. While a company with only ordinary shares is most common, many family companies, investment companies, professional companies and adviser-built structures need more flexibility.

Different classes of shares allow the company to separate control from economic benefit. A person can hold voting power without receiving a special dividend class. Another person can receive dividends without controlling the company. An investor can hold priority rights without becoming the daily controller of the business.

Legal Consolidated Company Constitution: share classes used by advisers since 1988

Since 1988, we have provided Company Constitutions for Australian companies. Our Company Constitution is among the most widely used in Australia. Over 3,800 financial planners, accountants and lawyers build companies and update company constitutions with a Legal Consolidated Constitution.

Many law firms white-label our documents with their own corporate law firm logo. That is done by pressing a single button during the building process.

This article explains best practices in share rights, using the Legal Consolidated Company Constitution as an example. The key drafting is in Schedule A: Share Classes. Schedule A sets out different classes of shares and explains the rights attached to each class. You can see a full sample of our company constitution.

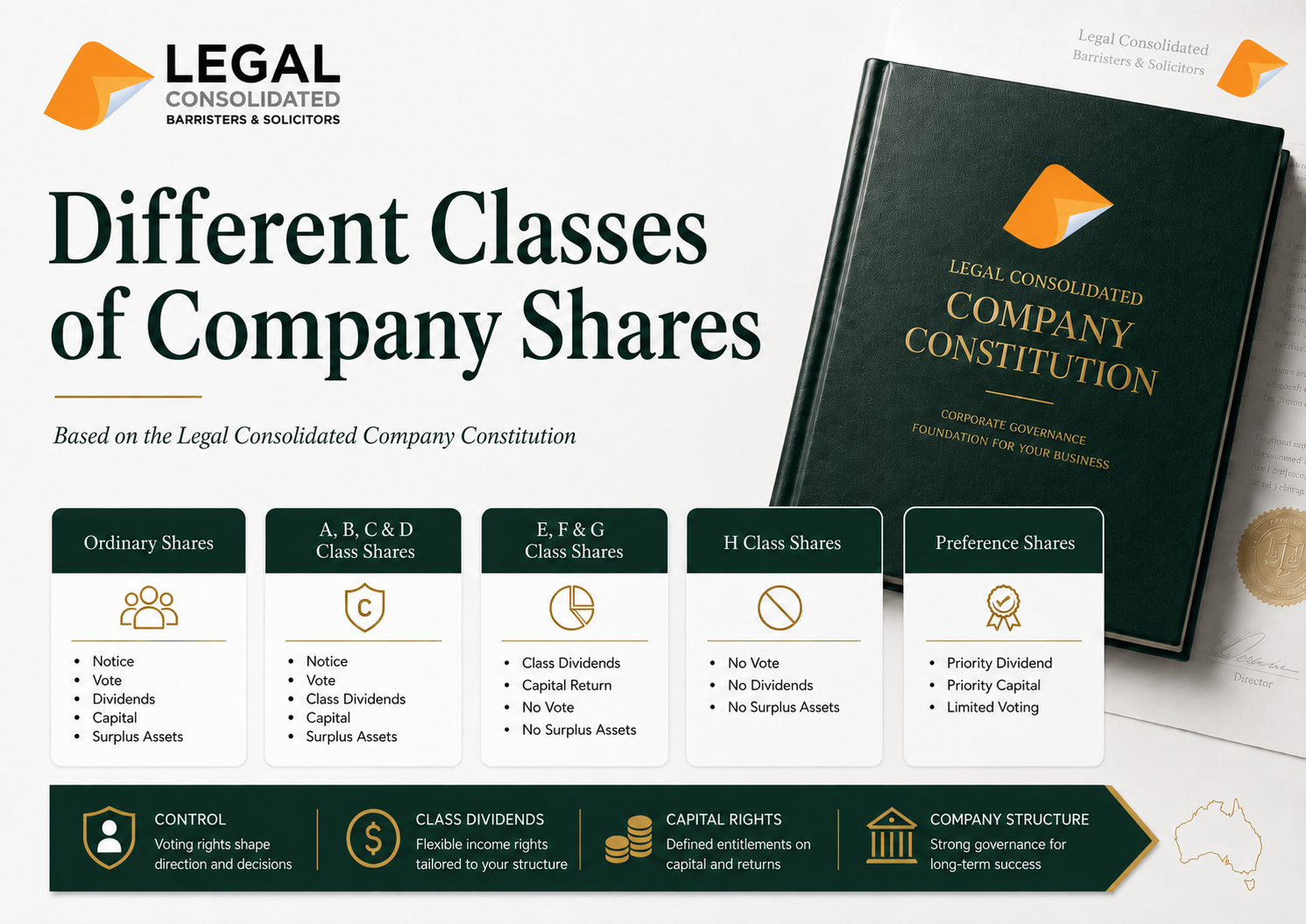

Share classes at a glance: voting, dividends, capital and common uses

| Share class | Voting and notice rights | Dividend rights | Capital and winding-up rights | Common use |

|---|---|---|---|---|

| Ordinary Shares | Notice, attendance and voting rights | Dividends declared for Ordinary Shares | Return of capital and surplus assets | Popular standard ownership and control |

| A, B, C and D Class Shares | Notice, attendance and voting rights | Dividends declared for that particular class | Return of capital and surplus assets | Voting shares with separate dividend classes |

| E, F and G Class Shares | No notice, no attendance and no voting rights | Dividends declared for that particular class | Return of capital, but no surplus asset participation | Dividend rights without voting control |

| H Class Shares | No notice and no voting rights | No dividends | No surplus asset participation | Narrow technical shareholding with almost no economic rights |

| Non-Cumulative Redeemable Preference Shares | Limited voting rights in protective situations | Fixed non-cumulative dividend set at issue | Priority return of capital, but no surplus asset participation | Priority capital without unpaid dividends building up |

| Cumulative Redeemable Preference Shares | Limited voting rights in protective situations | Fixed cumulative dividend set at issue, with arrears and interest | Priority return of capital plus unpaid dividends, but no surplus asset participation | Priority capital where unpaid dividends accrue |

| All other classes | As adopted by the Board at issue | As adopted by the Board at issue | As adopted by the Board at issue | Later custom classes for future needs |

This is the benefit of a Legal Consolidated Constitution. We do not merely incorporate the company. We give the company a disciplined set of share classes from the start, with room to add more later.

Ordinary Shares in a company constitution: standard voting and ownership rights

Over 90% of shares are Ordinary Shares. They are popular and most common. The Legal Consolidated Constitution gives Ordinary Shares the right to:

- receive notice of any general meeting of the company

- attend and vote at all general meetings

- receive dividends, distributions, bonuses and other profits declared on, or accrued for, Ordinary Shares.

Ordinary Shares also carry capital rights.

On a winding up, or on a return of capital, Ordinary Shares have the right to a return of capital pari passu with other Ordinary Shares. This means every Ordinary Share is equal to every other Ordinary Share. If one Ordinary Share gets a dividend of $40,000, each other Ordinary Share gets $40,000.

They also participate in the distribution of surplus assets on a winding up of the company.

Ordinary Shares are usually suitable where voting, dividends, and capital rights are to be combined. For example, two business partners may each hold 50 Ordinary Shares. They both vote, both receive dividends declared on Ordinary Shares, and both share in the capital value.

The advantage is simplicity. The disadvantage is that all the main rights move together. Where a company needs different people to hold different rights, Ordinary Shares alone may be too blunt.

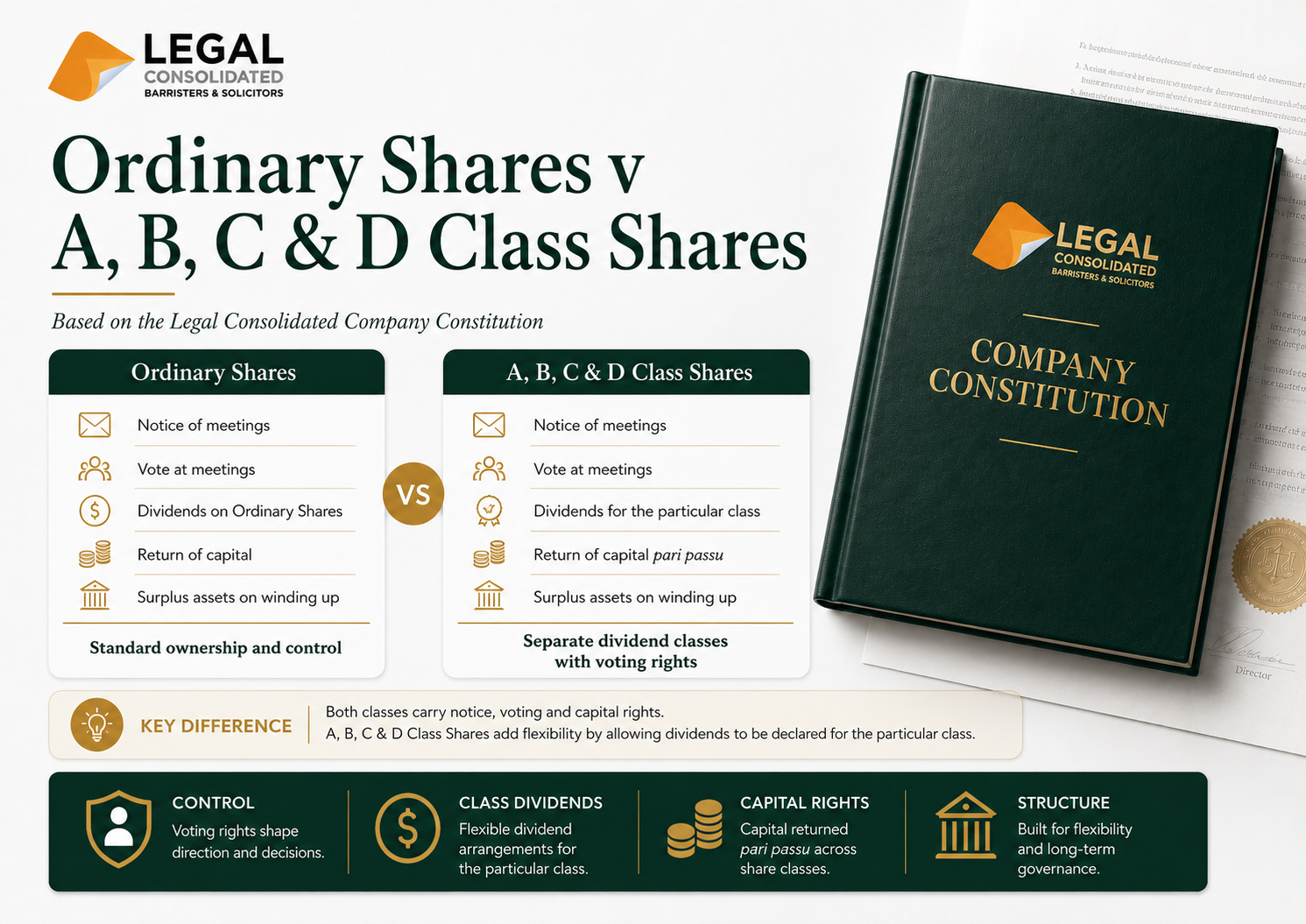

A, B, C and D Class Shares: voting shares with separate dividend rights

rights

The Legal Consolidated Constitution gives A, B, C and D Class Shares the right to receive notice of any general meeting. Holders of these shares can attend and vote at all general meetings of the company. They also have the right to receive dividends, distributions, bonuses and other profits declared on, or accrued for, that particular class of shares.

The important words are “that particular class of Shares”. They allow dividends to be declared by reference to a particular class, rather than treating all shareholders the same way. This is often useful in family companies and adviser-built structures.

For example, Mum may hold A Class Shares, Dad may hold B Class Shares and an adult child may hold C Class Shares. Each class has voting rights. But dividends can be declared for a particular class where the constitution, the Corporations Act 2001 (Cth), directors’ duties and tax advice allow it.

A, B, C and D Class Shares also carry capital rights. On a winding up or on a return of capital, they have the right to receive it pari passu with Ordinary Shares. They also participate in surplus assets on the winding up of the company.

E, F and G Class Shares: dividend shares without voting control

The Legal Consolidated Constitution treats E, F and G Class Shares differently. These shares have no right to receive notice of a general meeting. They also have no right to attend or vote at the company’s general meetings.

But E, F and G Class Shares can receive dividends. They have the right to receive dividends, distributions, bonuses and other profits declared on, or accrued for, that particular class of shares. This separates income rights from voting control.

For example, parents may wish to keep voting control of the company but allow an adult child to receive dividends declared for a particular class. The parents might hold Ordinary Shares or A Class Shares. The child might hold E Class Shares, which can receive dividends but do not carry voting control.

E, F, and G Class Shares also have a right to receive a return of capital. But they do not participate in the distribution of surplus assets on a winding up of the company. That difference matters when planning who receives value during the company’s life and who shares in the end value.

Person of straw – asset protection

A common asset protection strategy is the “person of straw and person of substance” approach. The person of straw holds little or nothing of value. That is deliberate. Valuable assets are kept away from the high-risk person.

Shares are valuable. That creates a problem. If the high-risk person becomes bankrupt, their trustee in bankruptcy may take control of those shares.

But there may still be tax reasons to distribute income to the high-risk person. For example, they may have lower marginal tax rates in a particular year.

This is where E, F and G Class Shares may help. They allow dividends to be paid to a particular class without giving that person voting control of the company.

For example, the company issues 10 F Class Shares to the high-risk person for $1.00 per share. The total issue price is $10. The company may then declare a dividend of $10,000 per F Class Share. The holder of the F Class Shares receives $100,000.

If that person later becomes bankrupt, the shares are still non-voting. They do not carry control of the company. On a winding up, the company only returns the paid-up capital on those shares. In this example, that is $10.

H Class Shares: no vote, no dividends and no surplus asset rights

H Class shares are rarely used. The Legal Consolidated Constitution gives H Class Shares very narrow rights. H Class Shares have no right to receive notice of any general meeting. They also have no right to vote at any general meeting.

H Class Shares do not receive dividends. They do not participate in a distribution of surplus assets on the winding up of the company. The issue of other classes of shares does not constitute a variation of the rights of the holders of H Class Shares. As they do not receive (passive) income, they are sometimes issued to children under 18 years of age.

The Constitution also gives the company specific powers over H Class Shares. It allows the company to deal with the transfer, cancellation and purchase of those shares in the way set out in Schedule A. The drafting is designed so that H Class Shares do not carry ordinary voting, income or surplus capital rights.

A practical example of H Class Shares:

A company needs a person, nominee or custodian to hold a technical shareholding for a limited structural reason. The company does not want that person receiving votes, dividends or surplus value. H Class Shares let that person appear as a shareholder, but with almost no economic or control rights. If the holding is no longer needed, the constitution contains wording to transfer, cancel or purchase those shares, subject always to the Corporations Act 2001 (Cth).

Non-Cumulative Redeemable Preference Shares: fixed priority return without dividend build-up

The Legal Consolidated Constitution includes Non-Cumulative Redeemable Preference Shares. These shares receive notices and vote at general meetings as if they were Ordinary Shares, but only in limited protective circumstances. Those circumstances include dividend arrears, a proposal to reduce capital, a proposal affecting the rights attached to the shares, a proposal to wind up the company, and a proposal to dispose of all the company’s business, property and undertaking.

The dividend right is fixed. The shares are entitled to a fixed, non-cumulative dividend at an annual rate determined by the directors on the date of issue. Importantly, the dividend ranks ahead of dividends paid on all other shares of the company on issue.

The capital right is also a priority right. On winding up or on a return of capital, the holder has the right to a return of capital in priority to all other shares of the company on issue. But the holder does not participate in any distribution of surplus assets.

An example is an investor who contributes capital and wants a priority return, but does not need unpaid dividends to accumulate year after year. The word “non-cumulative” is important. It means the preference dividend does not build up in the same way as a cumulative preference dividend.

Cumulative Redeemable Preference Shares: fixed priority return with dividend arrears

The Legal Consolidated Constitution also includes Cumulative Redeemable Preference Shares. These shares have similar limited protective voting rights to the Non-Cumulative Redeemable Preference Shares. The holder votes only in defined situations where the preference shareholder’s position is affected.

The dividend right is stronger. The holder has the right to a fixed cumulative dividend at a rate per annum determined by the directors at the date of issue. The cumulative dividend, plus arrears and interest, ranks in priority to dividends paid on all other shares of the company on issue.

The capital right also recognises unpaid dividends. Upon winding up or upon a return of capital, the holder has the right to receive the return of capital plus any unpaid dividends. The holder ranks in priority to all other shares, but does not participate in surplus assets.

An example is an investor who requires a fixed return that accumulates if not paid. This is materially different from a non-cumulative preference share. It gives the investor a stronger economic position, and the company needs to understand that before issuing the shares.

Redeemable Preference Shares under the Corporations Act 2001

The Legal Consolidated Constitution allows the company to redeem preference shares on the terms set out in Schedule A. For Non-Cumulative Redeemable Preference Shares, the company may redeem them by paying the aggregate issue price on or before 40 years from the date of incorporation. For Cumulative Redeemable Preference Shares, the redemption amount includes the aggregate issue price plus accrued unpaid dividends.

The statutory provisions are important. Redemption of redeemable preference shares is dealt with in the Corporations Act 2001 (Cth) ss 254J and 254K. The company must follow both its own Constitution and the Act.

Preference shares should not be issued casually. They are useful where priority rights are needed. They also carry legal, accounting and tax consequences that need to be understood before issue.

All other classes: adding later share categories to the company constitution

Schedule A ends with an important category: “All other classes”. The Legal Consolidated Constitution provides that all other classes have the rights and obligations adopted by the Board at the time of issue. This gives the company flexibility for future commercial needs.

No constitution can predict every future transaction. A company may later need an investor class, employee class, founder class, dividend-only class, growth class, or restructure class. The “all other classes” wording allows the Board to adopt rights and obligations for a later class, subject to the Constitution and the Corporations Act 2001 (Cth).

For example, a company may start as a family company and later admit a strategic investor. The investor may not fit neatly into Ordinary Shares, A–D Class Shares, E–G Class Shares or preference shares. The Board can adopt a new class with rights suited to that transaction.

This is another benefit of a Legal Consolidated Constitution. It gives the company named classes from the start, but it also allows later classes to be created when the company’s structure changes. That is better than forcing tomorrow’s commercial deal into yesterday’s share rights.

Voting rights in company share classes: who controls the company?

Voting rights are about control. Ordinary Shares vote. A, B, C and D Class Shares vote. E, F and G Class Shares do not vote. H Class Shares do not vote.

Preference shareholders vote only in limited protective circumstances. This is sensible because preference shareholders often hold priority economic rights rather than day-to-day control rights. They receive a voice when their position is affected, but they do not necessarily run the company.

The difference between a voting share and a non-voting share is not cosmetic. If a person should not influence company control, then issuing voting shares to that person creates unnecessary risk. If a person should receive income but not control, E, F and G Class Shares may be more suitable.

This is why advisers look closely at share rights before issuing shares. The question is not only “how many shares?” The better question is “what rights should this person hold?”

Dividend rights in company share classes: who receives company profits?

Dividend rights decide who can receive profits declared by the company. Ordinary Shares receive dividends declared for Ordinary Shares. A, B, C and D Class Shares receive dividends declared for that particular class. E, F and G Class Shares can also receive dividends declared for that particular class, even though they do not vote.

H Class Shares receive no dividends. Preference Shares receive fixed dividends on the terms set at the time of issue. Non-Cumulative Redeemable Preference Shares have a fixed non-cumulative dividend, while Cumulative Redeemable Preference Shares have a fixed cumulative dividend with arrears and interest.

The company must still comply with the law before paying dividends. The relevant provision is Corporations Act 2001 (Cth) s 254T. Directors must also consider their duties, the company’s position and the tax consequences before declaring dividends.

The constitution gives the rights. The directors still carefully exercise their duties and obligations and make the decision. The accountant then helps ensure the decision works from a tax and accounting perspective.

Capital rights in company share classes: who receives value at the end?

Capital rights decide who receives capital back and who participates in surplus assets. Ordinary Shares and A, B, C, and D Class Shares have return-of-capital rights and surplus-asset rights. E, F, and G Class Shares have return-of-capital rights but no surplus-asset participation.

H Class Shares have no surplus asset rights. Preference Shares have priority return-of-capital rights but do not participate in surplus assets. Cumulative Redeemable Preference Shares also protect unpaid dividends on return of capital or winding up.

These differences are important. A shareholder may receive dividends during the life of the company but not share in surplus assets at the end. Another shareholder may vote and participate in growth value, but not rank ahead for capital.

Capital rights are often ignored when a company is first incorporated. That is a mistake. The end position should be understood before the first shares are issued.

Best practice for different classes of shares

Best practice starts with the rights, not the number of shares. Ask who should vote, who should receive dividends, who should receive capital, who should share in surplus assets and who should rank first. Once those questions are answered, the share class follows.

This is especially important in family companies. Parents may want control. Adult children may need dividend rights. Investors may want priority capital. A later restructure may need a custom share class.

A Legal Consolidated Constitution gives advisers a strong starting point. Schedule A sets out the main share classes and their rights. It also allows later classes to be adopted by the Board at the time of issue.

Good share drafting is quiet when things are going well. It becomes valuable when control, dividends, capital, or succession matters. That is why share classes should be considered at the start.

Build a company with different classes of shares

When you build a company or update the Company Constitution with Legal Consolidated, read the hints as you work through the questions. Consider who should hold voting rights, dividend rights, capital rights and priority rights. Speak with your accountant about the tax and accounting consequences of the proposed share structure.

When you reach LOCK AND BUILD, telephone Legal Consolidated. We can discuss the questions and the document with you. You then finalise the company and receive the Company Constitution and supporting documents immediately.

Update your existing company constitution for different share classes

Many non-Legal Consolidated company constitutions do not contain suitable share class drafting. They may not properly deal in A, B, C, and D Class Shares, non-voting dividend shares, H Class Shares, redeemable preference shares, or later custom classes. That limits what the company can do.

A company can update its constitution. This is often considered when the company has grown, new shareholders are introduced, advisers want different dividend classes, investors are admitted, or succession planning becomes important. Tax, duty, accounting and Corporations Act issues must be considered before changes are made.

Legal Consolidated builds updated company constitutions. The updated Constitution can give the company a better share rights framework for the future. It is better to have the rights clearly set out before they are needed.

Upgrade company rules |

|

|---|---|

| Upgrade Company Constitution – also allows for single director company | |

| Replace Old Memo and Articles of Association – upgrade from Replaceable Rules | |

| Replace Lost Company Constitution | |

| Replace Replaceable Rules |