Update Family Trust to Exclude Foreigners

These are the two reasons why Family Trust Foreigner updates fail:

1. The problem of one update to remove foreigners from every state

Generic templates attempt to cover every Australian state in one Deed of Variation. This is dangerous. There is no such thing as a standard “Australian” exclusion of foreigners.

Every State Revenue Office has unique and contradictory rules. For example, NSW Revenue requires the exclusion to be irrevocable. Victoria applies a strict substantial interest test. The Northern Territory has no foreigner tax.

Trying to satisfy conflicting definitions in one Update Deed does not work. You only find this out years later when you suffer a State Revenue audit.

2. Making the foreigner clause conditional on a future event

Many non-legal providers use “dormant” clauses. These exclude foreigners only if the trust owns land.

This approach fails under N & G Grima Family Trust v Chief Commissioner of State Revenue [2025] NSWCATAD 149. The Tribunal states that “on/off” mechanisms fail the strict “no amendment” tests.

The Legal Consolidated solution to foreigner updates

We prepare a state-specific Deed of Variation. We ask which state the land is in. We apply the exact legislative rules for that jurisdiction. We prepare the Deed to be absolute and irrevocable. This precision is designed to withstand a state audit.

There are no foreigners in my Family Trust. I am a proud third-generation Australian!

State Revenue deems your Trust ‘foreign’. This is whether it is true or not.

Family Trusts are automatically deemed to have ‘foreign’ beneficiaries because the class of beneficiaries is so widely defined in a modern Family Trust. Most Family Trusts have over 400,000 beneficiaries.

Are the foreigner taxes in addition to the normal stamp duty and land tax?

Yes. Foreign person surcharges are additional taxes. They are levied on top of the usual stamp duty and land tax. These surcharges are extra costs you pay over and above the normal stamp duty and land tax.

What is a ‘foreign person’ in a discretionary trust?

What makes a person ‘foreign’? Each state answers that differently.

Generally, a human is a ‘foreign person’ if they are not:

-

- an Australian citizen; or

- the holder of a permanent Australian visa.

An entity (non-human) is a ‘foreign person’ if it does not ordinarily reside in Australia:

-

- is a foreign corporation (company) or

- the trustee of a foreign trust.

While not a legal definition and has no force of law, NSW Revenue helpfully explains:

“You are generally considered a foreign person, unless:

- you are an Australian citizen, or you have lived in Australia for 200 days or more in the 12 months prior to the taxing date of 31 December, and

- you are a permanent resident of Australia.”

Definitions of ‘Foreign Person’ in Australian Legislation

-

New South Wales:

- “Foreign person” as defined by the Foreign Acquisitions and Takeovers Act 1975 (Cth) (FAT Act), as modified by section 104J of the Duties Act 1997 (NSW). (Revenue Ruling G9 explains the definition.) Status as a ‘foreign person’ is determined when a liability for duty or land tax would arise.

- ‘Foreign person’ or ‘foreign trustee’ as defined in the Duties Act 1997 (NSW).

- ‘Foreign person’ as defined in the Land Tax Act 1956 (NSW).

-

Victoria:

- ‘Foreign natural person’, ‘foreign corporation’, or ‘foreign trust’ as defined in the Duties Act 2000 (Vic).

- ‘Absentee person’ as defined in the Land Tax Act 2005 (Vic).

-

Queensland:

- ‘Foreign person’ as defined in the Duties Act 2001 (Qld).

- An individual who is not an ‘Australian citizen’ or ‘permanent resident’, a ‘foreign company’ or the trustee of a ‘foreign trust’ as defined in the Land Tax Act 2010 (Qld).

-

South Australia:

- ‘Foreign person’ as defined in the Stamp Duties Act 1923 (SA).

-

Western Australia:

- ‘Foreign person’ as defined in the Duties Act 2008 (WA).

-

Tasmania:

- ‘Foreign person’ as defined in the Duties Act 2001 (Tas).

-

Australian Capital Territory:

- ‘Foreign person’ as defined in the Land Tax Act 2004 (ACT).

-

Northern Territory

- The Northern Territory has no ‘foreigner’ penalty tax or land tax. Well done, NT.

Why exclude Foreign Persons from your Family Trust?

State governments impose tax surcharges when the Family Trust holds certain types of land. Each state defines land differently.

| State | Types of land that suffers the Surcharge Stamp Duty | Types of land that suffer the Surcharge Land Tax |

|---|---|---|

| QLD | Residential Property | All land that is already subject to Land Tax |

| NSW | Residential Property | Residential Property |

| ACT | N/A | Residential Property |

| VIC | Residential Property exemption if used for social or emergency housing |

All land that is already subject to Land Tax |

| TAS | Residential Property, Primary Production | Both Residential Property and primary production (farmland) |

| SA | Residential Property | N/A |

| WA | Residential Property | N/A |

| NT | N/A | N/A |

If you do not have affected land in that particular state, then you do not need to vary your Family Trust. You do not have to remove foreigners.

Does excluding foreign beneficiaries from a Family Trust trigger a ‘Resettlement’?

You suffer a ‘resettlement’ when you change a Trust so fundamentally that the old Trust dies. A new Trust begins. This triggers Stamp Duty and Capital Gains Tax on all your assets.

We seek to reduce the chance of a resettlement by applying these four methods:

1. How to reduce a resettlement when you vary your Family Trust to exclude beneficiaries

To reduce the chance of resettlement, best practice is to use a Standalone Deed of Variation. This Deed sits alongside your main Trust Deed. It does not replace it.

Template providers often rewrite your main Trust Deed to ban foreigners. This is dangerous. The more you interfere with the original Deed, the higher the risk of resettlement.

A safer approach is a standalone Deed of Variation to restrict the Trustee’s power rather than removing beneficiaries. This ensures continuity of the trust property and membership. We prepare the Deed of Variation to comply with the Commissioner of Taxation v Clark [2011] FCAFC 5. Our Deed seeks to maintain the trust’s continuity in compliance with the Federal Court.

2. Why State-Specific variations protect your Discretionary Trust

Generic templates try to ban foreigners nationwide in a single document. This requires massive, broad changes to your Family Trust Deed.

This creates risk. In Mercanti v Mercanti [2016] WASCA 206, broad attempts to vary a trust schedule failed because the amendment power was not sufficiently specific.

Accordingly, our Deed of Variation is limited to the specific laws of one state. For example, if the affected land is in Victoria, we restrict the Trustee only for Victoria. The rest of your Discretionary Trust remains undamaged. This precision supports the specificity requirements in Mercanti and also Provincial Insurance Australia Pty Ltd v Consolidated Wood Products Pty Ltd (1991) 25 NSWLR 541.

3. Avoiding the ‘Conditional Clause’ trap to remove foreigners

While rare after 2025, some deeds still contain “dormant” clauses that only activate the foreigner removal if you ever buy land. This ‘conditional’ approach is now dangerous, as evidenced by N & G Grima Family Trust v Chief Commissioner of State Revenue [2025] NSWCATAD 149.

As required for each particular state, pursuant to Grima, our Foreign variations are absolute and irrevocable.

4. Preserving the ‘Substratum’ of your Discretionary Trust

A variation must not destroy the underlying purpose, or ‘substratum,’ of the Trust. This is stated in Kearns v Hill (1990) 21 NSWLR 107.

We carefully prepare the amendment power to comply with Kearns v Hill. In that case, the Court confirmed that you can vary beneficiaries without destroying the trust, provided the substratum remains.

By limiting our variation to a single state, we seek to preserve the substratum of your Trust to the highest degree possible.

Does ‘holding’ land include ‘buying’?

According to what we are seeing, it does not matter how the Family Trust acquires, controls, or owns the real estate. This includes purchases, transfers, agreements for sale, declarations of trust, surrenders, and options (including put-and-call options).

However, according to the accountants and lawyers who build legal documents on our website, some states have been offering refunds and exemptions for new home developments. This is where the Australian developer companies are owned by foreign persons.

Why Use a Separate Deed to Exclude Foreigners?

Keeping the main family trust deed separate from the Deed of Variation to exclude foreign beneficiaries is essential. It ensures legal clarity, minimises risks, and maintains the flexibility of your trust.

1. Protecting the Original Trust Deed

The Exclude Foreigner Deed should be kept separate from the Family Trust Deed and other Deeds of Variation.

The main trust deed is the foundation of your family trust. A separate Deed of Variation preserves its integrity, avoiding errors or unintended consequences from direct amendments.

2. Managing Irreversible Changes

Excluding foreign beneficiaries is an irreversible action. If circumstances change — for example, a family member gains or loses foreign status — it is easier to address these changes without rewriting the original deed. A separate document allows for targeted amendments without risking the validity or effectiveness of the family trust.

3. Ensuring Legal Compliance

Each Australian state and territory has unique laws for excluding foreign beneficiaries. Maintaining a separate deed helps with compliance with these jurisdictional requirements without unnecessary changes to the core trust. This is especially critical for trusts holding property across multiple states. (Legal Consolidated does not recommend a Family Trust hold more than one property. It should never hold properties across state borders.)

4. Reducing Legal Risks

Separate documentation avoids ambiguity and reduces the risk of disputes, as seen in cases like Oswal v FCT [2014] FCA 812. It ensures the trust’s validity and compliance.

5. Simplifying Administration

Future updates to the trust are easier when the exclusion of foreign beneficiaries is isolated in a separate Deed of Variation.

A separate Deed of Variation protects your trust’s integrity, reduces risks, and ensures compliance.

Multiple Properties in a Family Trust do not work for the Foreign Ownership Rules

Owning multiple properties in a single Family Trust creates problems with the foreign ownership rules. State laws constantly change, and some property owners have executed over 16 Deeds of Variation to remove foreign beneficiaries from their Family Trust.

Each Exclude Foreign Beneficiaries Deed modifies the same Discretionary Trust. These Deeds irrevocably exclude any ‘foreign person’ from benefiting under the Family Trust.

When multiple amendments, such as Deeds of Variation, are made to a single Family Trust, the risk of conflict between these amendments increases. Each amendment alters the terms of the Trust, and over time, the cumulative changes may contradict or undermine one another.

For example, one amendment may irrevocably exclude foreign beneficiaries, while another might introduce terms that unintentionally allow a class of beneficiaries with indirect foreign ties. Inconsistent definitions, overlapping terms, or conflicting priorities in the amendments can lead to legal disputes, administrative confusion, or even make the Trust unenforceable in certain aspects.

These conflicts complicate the Trust’s operation, jeopardise compliance with state laws, and expose the property owner to penalties and legal challenges. Therefore, relying on a single Family Trust to hold multiple properties is risky and inefficient compared to establishing separate Trusts for each property.

Why not make every Family Trust free of foreigners?

Reducing your class of beneficiaries reduces the value of the Family Trust. A Family Trust should have the widest group of beneficiaries possible. Removing foreigners from the class of beneficiaries damages the Family Trust. It makes it less valuable.

Therefore, only fetter your Family Trust to remove foreigners when necessary. And then, do not use that ‘damaged’ Family Trust for any other purpose. Build a second family trust if you want to buy a second piece of land in the same state. And then build a third Family Trust if you want to buy land in another state.

Build a fourth family trust on Legal Consolidated’s website to hold cash and buy shares — and ensure this Family Trust remains undamaged. There is no need to restrict foreigners in this fourth family trust because it does not own real estate.

The Deed to remove foreigners is irrevocable, and the damage is permanent. This certainty prevents state revenue officers from imposing the penalty stamp duty and land tax imposts. But if you or your family ever live outside of Australia, you stop being beneficiaries of your own trust. What if all your bloodline ends up living overseas?

Warning: only amend your Family Trust for foreigners if you have to

Accountants and financial planners often panic about the “foreigner surcharge” for stamp duty and land tax.

They rush to amend every Family Trust deed to exclude “foreign persons”.

This is a mistake.

Amending the Family Trust for foreigners does irreparable damage

When you amend a Family Trust to exclude foreigners, you damage the trust. You are restricting the class of beneficiaries. You are removing your ability to distribute to family members who might move overseas in the future.

You should only damage your Family Trust if you truly have to. You only do it if that specific trust will hold ‘land’ (as defined differently in each state) that imposes the surcharge.

Do ‘foreign persons’ in my Family Trust change from time to time?

My Family Trust does not own real estate

The state land tax and stamp duty foreign penalty taxes are for land owners. If your Family Trust does not own land, there is no need to harm it by a Deed of Variation to exclude foreigners.

If you do, one day, decide to buy land, then it is prudent to do so in a separate Family Trust. You should have a separate Family Trust for each piece of land you want to buy.

What is ‘residential’ land for the land tax and stamp duty surcharge?

Farms are exempt from the foreigner tax in NSW

In NSW, residential land includes:

- parcels of land on which one or more dwellings are situated;

- strata lots;

- utility lots, and

- parcels of vacant land that are zoned for residential purposes.

NSW land used for primary production is excluded from this additional surcharge. (See section 10AA.)

However, Tasmania imposes foreigner surcharges on farms

As you can see, every state is different. For example, unlike NSW, Tasmania imposes a foreign surcharge duty on acquisitions of primary production land.

Victoria and Queensland define land wider for the family trust foreigner surcharge taxes

Victoria and Queensland apply a wider definition of land. (However, in Victoria and Queensland, an exemption may be available for organisations significantly contributing to their state economy.)

Western Australia has its unique definition of land for the land tax and stamp duty foreign taxes in family trusts

Residential property is defined in section 205E of the Duties Act to mean:

(a) land in Western Australia that is capable of being, or is intended to be, used solely or dominantly for residential purposes

(b) vacant or substantially vacant land in Western Australia that is zoned solely for residential purposes or

(c) any estate or interest in land as described in (a) or (b).

However, these definitions are changing and being reinterpreted constantly. Do not rely on the above. It is general information only. Legal Consolidated is giving no legal advice on these issues. We do not review your document or advise on whether your family trust owns land within these foreigner surcharge taxes.

Where relevant, why does Legal Consolidated not state that ‘commercial’ property is exempt?

We do not know what ‘residential’ and ‘commercial’ mean for the particular property that your Family Trust is about to buy.

You are right. ‘Commercial’ property is not meant to be caught in this web of conflicting laws in some states. But what you think is ‘commercial’ may, at a stretch, end up being ‘residential’ as well. For instance, a property primarily used for business could have a residential component, such as apartments above shops. Additionally, some mixed-use properties, despite their commercial activities, might be classified as residential for tax purposes depending on state laws and the specific usage proportions.

Whereas the Victorian Revenue Office states:

‘Residential property does not include commercial residential premises, a residential care facility, a supported residential service or a retirement village and which may lawfully be used in that way.’

In some states, such as Queensland, land tax applies to all properties (including residential and commercial); however, stamp duty applies only to residential property.

Legal Consolidated is not providing advice on this. You need to speak with your lawyer and accountant about your specific circumstances.

An example where it is difficult to tell if the land is ‘farmland’ or ‘commercial’

In Wylarah Pastoral Co Pty Ltd ATF Tallong Family Trust v Chief Commissioner of State Revenue [2024] NSWCATAD 366, the New South Wales Civil and Administrative Tribunal (NCAT) examined whether a 9.3-hectare property qualified for a land tax exemption. This is under section 10AA of the Land Tax Management Act 1956 (NSW). The taxpayer claimed the land was used primarily for maintaining cattle, seeking exemption as primary production land.

The Tribunal acknowledged that activities such as pasture improvement, fencing, road enhancements, fertiliser application, and installing water systems constituted “use” of the land under section 10AA(3). However, it determined these were preparatory works, not the land’s dominant use. The property was concurrently used as a rental residence, and the Tribunal found that this residential use outweighed the preparatory agricultural activities. Consequently, the land did not meet the criteria for exemption as primary production land.

This case underscores the complexities in classifying land use for tax purposes, especially when properties serve multiple functions. To qualify for primary production exemptions, the dominant use of the land must be for agricultural activities, not merely preparatory steps. Property owners should carefully assess land usage and maintain clear evidence of dominant agricultural activities to meet exemption requirements.

Is there power to change my Family Trust to remove foreigners?

Your family trust deed must allow this Deed of Variation. Some family trust deeds contain a broad power of amendment and variation. However, those without or with limited variation powers must be carefully reviewed. Legal Consolidated does not provide that service. If you are unsure, seek accounting and legal advice.

Further, some states (e.g. NSW) recognise that some family trusts cannot be amended and will review the family trust on a case-by-case basis. (See, for example, NSW Commissioner’s Practice Note CPN 004 version 2.)

So, it is doubly important that you always lodge a request for a private ruling in that particular state of your unsigned Deed of Variation to exclude beneficiaries.

Does the Family Trust owe ‘foreigners’ money? Unpaid Present Entitlements (UPEs)

After this deed to remove foreigners is signed, those entitlements cannot be paid.

The order of signing the two separate Deeds is as follows:

- sign all the Deeds of Forgiveness to forgive the UPEs first and

- then sign the Deed of Variation to Exclude Foreigners.

Get rid of UPEs Before Excluding Foreigners

Living in London, young William is a ‘foreigner’ under the law. His Dad’s family trust owes him an Unpaid Present Entitlement (UPE).

Before Dad can sign the Deed to Exclude Foreigners, William must forgive the UPE. Dad drafts a Deed of Debt Forgiveness and emails it to William to sign.

John wants to buy some real estate through his family trust. He needs to sign a Deed to Exclude Foreigners. However, John’s family currently owes his son Williams some money. This is called an Unpaid Present Entitlement (UPE).

William now lives in London and is deemed a foreigner by the relevant state.

William must forgive the debt before his Dad signs the Variation to Exclude Foreigners Deed. His accountant builds a Legal Consolidated Deed of Debt Forgiveness. It is emailed to William, who signs it and emails it back. John now signs the Deed of Variation to Exclude Foreigners.

Get State Revenue approval BEFORE signing Family Trust Variation to remove Foreigners

Before signing your Family Trust variation to exclude foreigners, you must obtain a private ruling from the relevant revenue office. This ruling confirms that your planned changes comply with the law.

Pre-approval is Essential for your Family Trust update

Do not sign the Deed of Variation to remove foreigners without written approval from the Revenue Office. Submit an unsigned copy of the Family Trust Deed to remove Foreigners.

Steps to Signing the Family Trust Deed of Variation to Exclude Foreigners

Sign the deed only after receiving written confirmation from State Revenue. This ensures your deed meets all legal requirements. Only then sign the Deed of Variation.

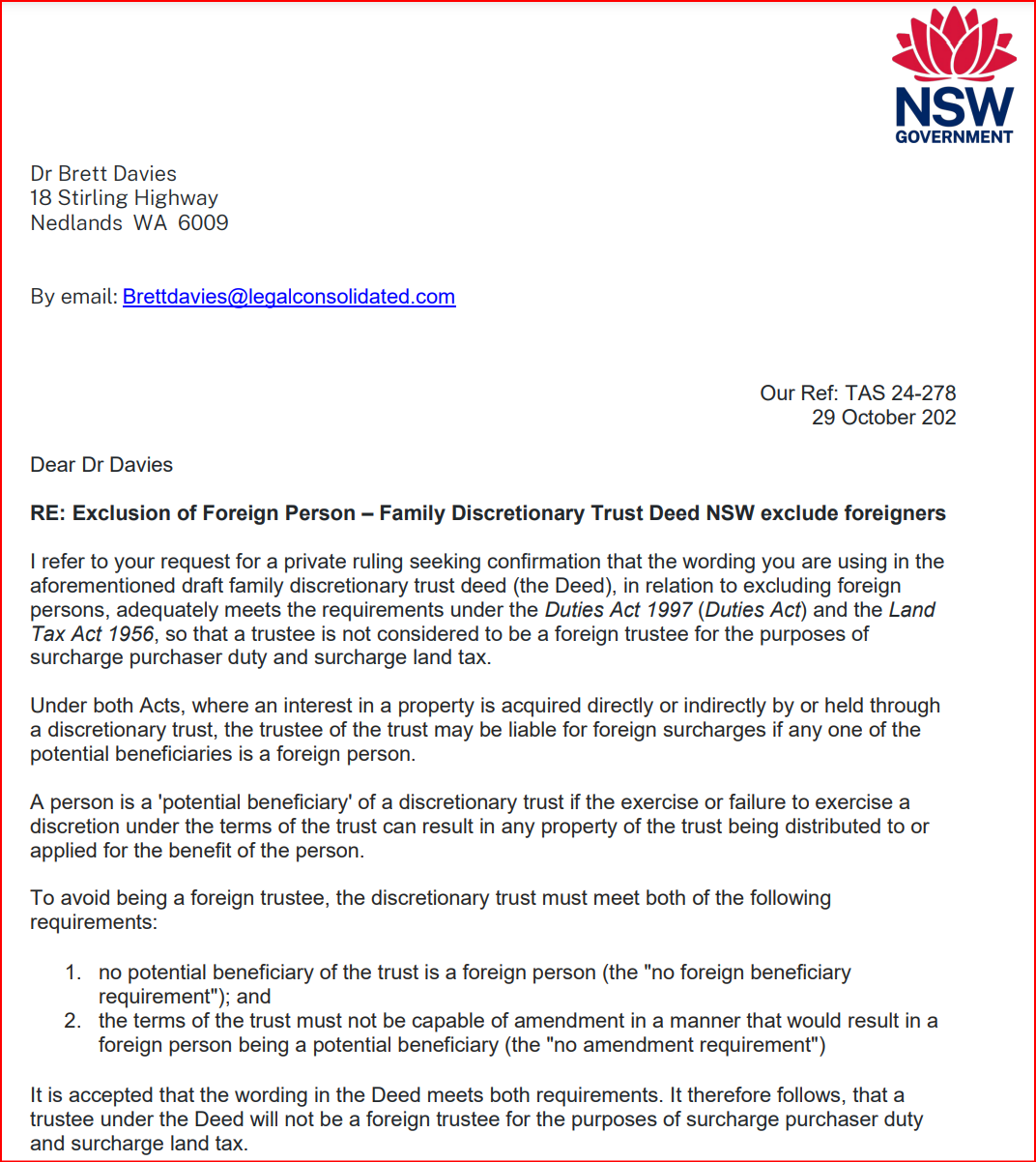

How do I apply for a Private Ruling with the local revenue office?

This is a sample of a Private Ruling.

Every Family Trust Deed is different.

Before relying on a Deed of Variation to Exclude a Beneficiary, you must get a ruling for your own Family Trust.

Private rulings for each state (other than the Northern Territory, as the NT does not have these taxes.)

- New South Wales

- Victoria

- Start form: https://www.sro.vic.gov.au/request-private-ruling

- Email: technicaladvice@sro.vic.gov.au

- Queensland

- Start form: https://qro.qld.gov.au/duties/private-ruling/

- Email: duties@treasury.qld.gov.au

- Western Australia

- Start form: https://apps.osr.wa.gov.au/portal/0/home (create an account first)

- Email: online email or telephone on 08 9262 1400

- South Australia

- Start form: https://www.revenuesa.sa.gov.au/forms-and-publications/information-circulars-and-revenue-rulings

- Email: revenuesa@sa.gov.au or telephone on (08) 8226 3750

- Tasmania

- Australian Capital Territory

- Start form: https://www.revenue.act.gov.au/self-assessment-tools-and-forms/forms/land-tax-notification-form

- Email: https://www.revenue.act.gov.au/contact-us (online) or telephone (02) 6207 0028.

Must the removal of foreigners be permanent and irrevocable?

RRS Holdings Aust Pty Ltd ATF RRS Holdings Trust v Chief Commissioner of State Revenue

In RRS Holdings Aust v Chief Commissioner of State Revenue [2024], NSWCATAD 352, the trustee owned residential properties in New South Wales. The trust was classified as a foreign person under section 5A of the Land Tax Act 1956 (NSW). This classification resulted in liability for surcharge land tax for the 2021, 2022, and 2023 tax years.

The trustee attempted to avoid this liability by amending the trust deed. A new clause was inserted stating that foreign persons were not entitled to any income or capital from the trust. However, the New South Wales Civil and Administrative Tribunal (NCAT) ruled that this amendment did not satisfy section 5D(3) of the Act. The amendment failed because it did not irrevocably prevent foreign persons from being potential trust beneficiaries.

The tribunal’s decision highlights a critical issue: excluding foreign persons in trust deeds must be permanent and irrevocable. Any clause that can be later reversed or modified does not meet the required standard under section 5D(3). As a result, the trust remained classified as a foreign person and was liable for the surcharge land tax.

This case serves as a warning to trustees of family trusts and discretionary trusts. If the trust holds or plans to hold property, it is essential to ensure that any exclusion of foreign persons in the trust deed is structured to be irrevocable. Failure to do so leads to adverse financial consequences, including ongoing liability for surcharge land tax.

Jemag Pty Ltd ATF The Nawar Family Trust v NSW State Revenue

You are diligently managing your Family Trust, thinking all is well—until the state revenue office slaps you with a hefty surcharge land tax bill. That is what happened to Jemag Pty Ltd, the trustee of the Nawar Family Trust. See Jemag Pty Ltd ATF The Nawar Family Trust v Chief Commissioner of State Revenue [2024] NSWCATAD 392.

The Nawar Family Trust owned a residential property in Sydney. Everything seemed fine until NSW State Revenue pointed to Section 5D of the Land Tax Act 1956 (NSW) and declared the Nawar Family Trust liable for surcharge land tax.

Why?

Because lurking among the Trust’s potential beneficiaries were members of Mr Nawar’s wife’s extended family—relatives living in Egypt, classified as foreign persons. These folks were not just distant cousins; they were part of the broad class of eligible beneficiaries to whom the trustee could distribute income or capital. Worse still, the Trust’s Deed was not amended.

If your Family Trust has even the possibility of a foreign beneficiary, the state assumes the worst: you are a “foreign trustee” and —penalty taxes like surcharge land tax hit you. For the Nawar Family Trust, this meant a costly lesson in trust management. The Tribunal did not budge: the trustee’s discretion to distribute to those Egyptian relatives sealed the deal. No exclusion of foreigners? No mercy from the taxman.

It is a wake-up call for anyone with a Family Trust holding land in Australia. The states are relentless, presuming every Family Trust has foreign ties unless you prove otherwise. Proving otherwise means taking action now. That’s where our Deed of Variation to Exclude Foreigners can help.

At a later time, can I reverse the Family Trust variation to remove ‘foreigners’?

The [NSW] Chief Commissioner will not be satisfied that there is no scheme or arrangement to avoid tax, where the amendment of the trust deed to remove the trustee’s power to make a distribution to a foreign person is not irrevocable.

Does a Deed of Variation work retroactively?

Q: I just got a big stamp duty and land tax penalty bill. Is there a document I can sign that works in the past to retrospectively exclude foreigners? Can I retroactively exclude foreigners?

A: At least in NSW, you cannot. Once you incur these costs, you cannot undo them by changing the trust deed retrospectively. You must prepare and amend trust deeds according to state laws before any property transactions. Legal Consolidated holds the view that other states would follow NSW in this approach.

In the case of Chloe Adolphi Pty Ltd as trustee for The Chloe Adolphi Family Trust v Chief Commissioner of State Revenue [2024] NSWCATAD 48, the Trust sought to amend its trust deed by deed of rectification to exclude foreign beneficiaries retroactively. The Trust was established in April 2021 and acquired NSW property in May 2021 without excluding foreign persons.

A rectification deed was signed in December 2022, but the court held that such a deed could not retroactively alter the trust’s status to avoid past liabilities. Therefore, a deed of rectification signed today cannot operate retroactively.

The Family Trust must be amended before acquiring residential property to escape foreign surcharges. See, for example, the Victorian State Revenues’ comment:

‘…persons considering purchasing residential property can ensure that they are not liable for the foreign purchaser additional duty by … amending the [Family Trust] trust deed so that there are appropriate restrictions on foreign persons as potential beneficiaries (e.g. include an express exclusion clause for foreigners). Importantly, any amendment will have to be done prior to the dutiable transaction completing (i.e. prior to settlement).’ [italic inserted by Legal Consolidated]

Rather than sign this Deed, can I stop distributing it to foreigners?

Merely choosing not to distribute to foreign beneficiaries does not stop the surcharge. This approach is ineffective because the applicable law evaluates whether a trust faces these surcharges based on including foreign persons in the trust deed, regardless of actual distributions.

The surcharges still apply even where the discretionary trust has no foreign controllers and has never been distributed to a foreign beneficiary

What if the ‘foreigner’ is also an Appointor, Trustee or Default Beneficiary?

If a ‘foreign person’ holds the role of appointor, trustee, or director/shareholder of a company, they exercise significant control over the trust’s operations. You may need to build two separate Deeds of Variation:

- Foreigner Deed of Variation Update, and then build

- the second document, which is called a Change Trustee, Appointors and excludes a Beneficiary Deed of Variation

In summary, simply using a deed of variation to remove foreigners does not resolve the issue of a ‘foreign person’ who also occupies these key positions.

Is the Deed of Variation to exclude foreigners the right document for my Family Trust?

Legal Consolidated Barristers and Solicitors does not provide legal advice. This Deed of Variation is designed to apply across all Australian states and the Australian Capital Territory (it does not apply to Northern Territory land as the NT does not impose these surcharges).

However, not all jurisdictions require excluding all such persons, and some may not require this Deed of Variation. Requirements can be less stringent in some states.

Moreover, the type of land your Family Trust intends to acquire might not necessitate excluding foreigners.

Do not sign this legal document until you have consulted with your accountant and lawyer to confirm its suitability for your Family Trust.

Additionally, before signing, ensure the local revenue office in the state where your family trust will own land has approved the Deed through a written private ruling.

Is the Family Trust Deed to remove foreigners set and forget?

Australia comprises eight distinct jurisdictions, each with its own legal system. Each jurisdiction’s laws are constantly in flux, adapting to new legal interpretations and international agreements.

NSW’s Tax Treaty Adjustments in 2023

In 2023, NSW changed its surcharge laws following a court decision that found the previous regulations violated international tax treaties, including agreements with Finland, Germany, India, Japan, New Zealand, Norway, South Africa, and Switzerland. These treaties incorporate non-discrimination clauses prohibiting higher taxation on foreigners compared to Australians.

As a result of the court’s ruling, Revenue NSW was required to refund the excess tax collected from nationals of these treaty countries. However, some states decided against implementing similar refund measures. This variation in response highlights the differing approaches to international tax treaty obligations across Australian jurisdictions.

At NSW’s request, the Commonwealth government asked for the laws to be changed. But the changes may not have worked.

This is just one of many war stories reported to us by the 4,600 accountants, lawyers, and financial planners who build legal documents on our website.

The eight payroll systems were aligned, so why do not these foreign rules?

Many accounting houses, financial planning groups and law firms, including Legal Consolidated, lobbied for many years for consistency in the state payroll taxes.

By 2010, all eight jurisdictions had aligned their payroll tax provisions. This major step simplified the tax landscape for cross-border employers, with NSW, VIC, TAS, NT, and SA adopting nearly identical payroll tax legislation. This alignment has significantly eased the administrative burden across state lines.

Legal Consolidated advocates for foreign penalty taxes to be unified across Australia

As a national law firm, Legal Consolidated actively lobbies state governments (and the Commonwealth) to align various areas of tax law, including the land tax and stamp duty foreigner surcharge. This alignment would significantly benefit investors and trust structures operating across Australia.

Grima Family Trust case: a warning for all trusts – no more conditional clauses

A decision in the NSW Civil and Administrative Tribunal highlights a critical flaw in many family trust deeds. A commonly used ‘foreign person exclusion clause’ is found to be ineffective. This exposes trusts to significant surcharge stamp duty and land tax.

The case is N & G Grima Family Trust Pty Ltd v Chief Commissioner of State Revenue [2025] NSWCATAD 149. The decision shows how even carefully drafted clauses can fail.

Some states have a special requirement as to ‘no amendment’

The fatal flaw in Grima: The foreign person exclusion was not permanent, exposing the trust to surcharge taxes.

The decision in Grima is a direct consequence of the stringent ‘no amendment’ provisions contained in the NSW legislation. Unlike other states, NSW requires that the exclusion of foreign beneficiaries from a trust be permanent and irrevocable. The legislation was specifically designed to prevent trusts from temporarily complying with the rules to avoid surcharge taxes, only to later amend the deed or have the exclusion fall away. The Tribunal’s focus on any mechanism that could alter the exclusion, even without a formal amendment, stems directly from this strict legislative intent.

The Grima Family Trust Decision

The Chief Commissioner assessed the trustee for surcharge land tax for the 2024 tax year. The assessment was based on the trust deed as it stood on the relevant date of 31 December 2023.

The deed contained clauses intended to exclude foreign persons. The definition of “Beneficiaries” excluded any “Excluded Person”, which in turn included any “Foreign Person”. The critical failure was found in the definition of a “Foreign Person”. It contained a ‘temporal limit’. The definition included:

(l) any potential Beneficiary of this Trust who would or might cause this Trust to be or become a foreign person or a foreign trust for the purposes of any other statute, and who, by being a Beneficiary, would or might cause this Trust to be assessed to additional or increased duty or land tax… but only while:

(m) the foreign person, corporation or trust continues to be so classified under the relevant provision; and

(n) the Trust acquires or holds, any direct or indirect interest in real property…

Clause 3 of the deed then stated this exclusion was irrevocable:

“3 EXCLUSION FROM BENEFITS … 3.3 Irrevocable This clause 3 is irrevocable and is not capable of being amended”.

Why the Grima Trust Clause Failed the ‘No Amendment’ Test

The Tribunal found the ‘temporal’ nature of the definition breached the ‘no amendment’ rule. The exclusion of foreign persons only applied while the trust held real property. This is not permanent. If the trust sells all its real estate, the exclusion ceases to operate. A foreign person could then ‘spring back’ into being a potential beneficiary.

Senior Member MacIntyre clarified the core issue, stating that the focus must be on what the deed allows for in the future. At paragraph 49, the Senior Member noted:

The critical question is not whether the class of beneficiaries has, in fact, been altered. It is whether the terms of the Deed, as they stood on the taxing date, contained a mechanism by which the composition of the beneficiary class could be altered at a later time. The self-executing nature of the definition provides for exactly such a mechanism.

This potential for the beneficiary class to change automatically is a ‘self-executing change’. The Tribunal found that this is no different from a formal power of amendment. At paragraph 54, the Tribunal stated:

This alteration to cl 3 what does, occurs not by reason of an amendment to the provision pursuant to the power to amend given to the Applicant under cl 19. It is an alteration, nevertheless, resulting from a change in circumstances. It is a self- executing change.

The Tribunal also commented on how this drafting circumvents the policy of the surcharge legislation. At paragraph 57, it noted:

“…if the Applicant were, at a future date, to dispose of the real property held subject to the trust… the proceeds of sale of the real property will form part of the fund from which they may now take, even though they previously could not take. The result would be to allow “foreign persons” to obtain a benefit from real property previously held within a trust, without having paid the higher rates of tax applicable to them. Such an outcome does not sit easily with the statutory purpose.”

The Tribunal’s comment highlights the ultimate flaw in the temporal clause: a trust could hold NSW residential property, sell it for a capital gain, and, because it no longer has real estate, the foreign beneficiary exclusion would fall away. The trust could then distribute the tax-free proceeds from the sale of that very same NSW property to the now-reinstated foreign beneficiaries. This defeats the entire purpose of the surcharge regime. The Tribunal has signalled that this pathway to circumvent the surcharge is unacceptable.

Foreign Person exclusion fails if the Definitions can be changed

The Commissioner argued that making only the operative exclusion clause (Clause 3) irrevocable was insufficient. Because the definitions of “Excluded Person” and “Foreign Person” in Clause 1.1 were still capable of being amended under the deed’s general amendment power, the exclusion could be undone indirectly by simply changing the meaning of who was to be excluded.

Therefore, the Trustee could also change the definitions at a later date.

While the Tribunal did not need to decide on this point, it serves as a crucial warning: for a deed to be compliant, not only must the exclusion clause itself be irrevocable, but so too must all definitions and related clauses that are essential to its permanent operation.

Your Trust is ‘Guilty Until Proven Innocent’

The starting position under the NSW surcharge rules is that a discretionary trust is treated as foreign by default.

The Chief Commissioner does not require identification of an actual foreign person who is a beneficiary of your trust. The onus is entirely on you, the trustee, to prove that your trust is not foreign. You can only satisfy this burden by having a trust deed that contains a clause that irrevocably and permanently prevents any foreign person from ever becoming a beneficiary.

The decision in Grima confirms that any flaw, loophole, or potential for future change in that exclusion clause will cause you to fail this test. The default ‘guilty’ status is reinstated, and the surcharge taxes will apply.

Solution after Grima: Amending Your Family Trust Deed

This ‘temporal’ wording is common in many trust deeds. This judgment places all such trusts at immediate risk of assessment for NSW surcharge taxes.

The only solution is to review your trust deed. Where necessary, amend it to remove the temporal limitation. The exclusion of foreign persons must be absolute and permanent. For both stamp duty and land tax, best practice is to amend the family trust before signing a contract to purchase real estate.

How the Grima decision impacts Victorian trusts

Currently, Victoria’s foreign duty rules, like those of most other states, do not have the same strict ‘no amendment’ test as New South Wales. The Victorian State Revenue Office has not, to date, required the foreign person exclusion clause to be irrevocable.

However, the Grima decision serves as a powerful reminder of how specifically legislation in this area can be interpreted. The prudent course of action is to ensure that all family trust deeds, regardless of which state the property is in, contain a robust and permanent foreign person exclusion clause. Adopting the higher NSW standard provides the best protection against future legislative changes or shifts in interpretation by revenue authorities in other states.

Are the foreigner removal laws for Trusts likely to keep changing?

Legal Consolidated believes this area of law is unsettled. We expect State and ACT government changes and court interpretations for the next few years. Join our free weekly newsletter to stay abreast of the changes as they unfold.

Do I need to amend my Unit Trust to escape foreigner land tax and stamp duty?

Generally, no.

Exclude Foreigners from a Family Trust

Why update a Family trust to get rid of Foreigners?

- Family Trust Deed – watch the free training course

- Family Trust Updates:

- Everything – Appointor, Trustee & Deed Update

- Deed ONLY – only update the Deed for tax

- Guardian and Appointor – only update the Guardian & Appointor

- Change the Trustee – change human Trustees and Company Trustees

- The company as Trustee of Family Trust – only for assets protection?

- Bucket Company for Family Trust – tax advantages of a corporate beneficiary

How to clean up a Unit Trust structure

- Unit Trust

- Unit Trust Vesting Deed – wind up your Unit Trust

- Change Unit Trust Trustee – replace the trustee of your Unit Trust

- Company as Trustee of Unit Trust – how to build a company designed to be a trustee of a Unit Trust

Fixing up partnerships and company structures

- Partnership Agreement – but what about joint liability?

- Incorporate an Australian Company – best practice with the Constitution

- Upgrade the old Company Constitution – this is why

- Replace lost Company Constitution – about to get an ATO Audit?

How to structure Service trusts and Independent Contractor Agreements

- Independent Contractor Agreement – make sure the person is NOT an employee

- Service Trust Agreement – operate a second business to move income and wealth

- Law firm Service Trust Agreement – how a law firm runs the backend of its practice

- Medical Doctor Service Trust Agreement – complies with all State rules, including New South Wales

- Dentist Service Trust Agreement – how dentists move income to their family

- Engineering Service Trust Agreement – commonly, engineers set up the wrong structure

- Accountants Service Trust Agreement – complies with ATO’s new view on the Phillips case