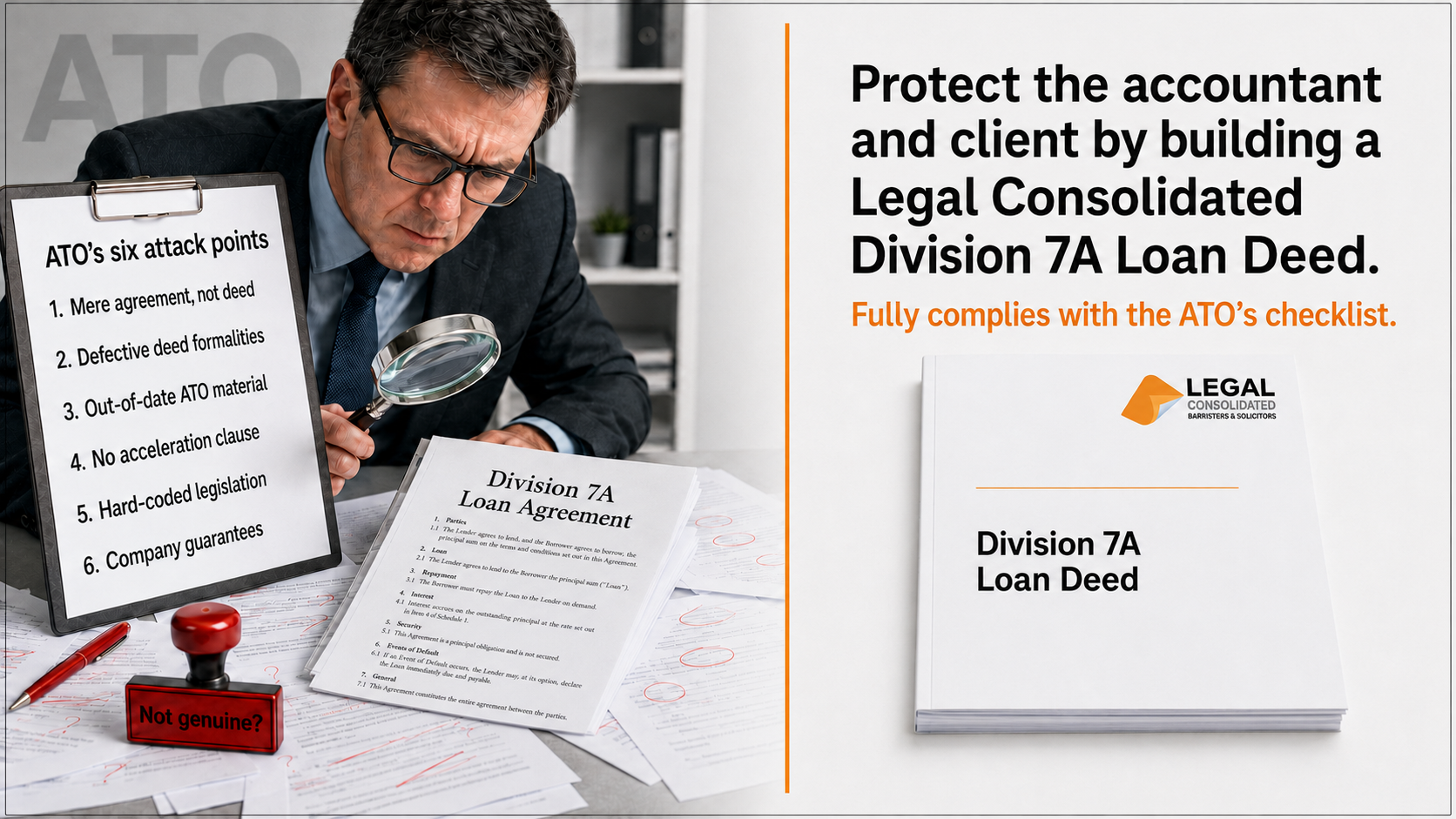

ATO’s 6 problems with Division 7A Loan Agreements

A Division 7A Loan Deed is not safe merely because it mentions section 109N. The ATO looks past the label. It tests whether the deed governs the actual advances, was signed on time and contains the machinery of a genuine commercial loan.

These are seven attack points that hand the ATO litigation bait:

1. Why prepare a Division 7A Loan Agreement as a Deed?

A lawyer did not prepare my Division 7A loan agreement

Only accountants can prepare tax returns, and only financial planners can provide financial planning advice. In the same way, only lawyers can prepare deeds and legal documents.

A law firm must prepare a Division 7A Loan Agreement. If a non-law firm provided you with a Division 7A Loan Agreement, even as an MS Word document, they have broken the law. See Legal Practice Board v Computer Accounting and Tax Pty Ltd [2007] WASC 184.

Worse still, a law firm’s Professional Indemnity insurance does not cover the document, so there is a high risk that it will not work. The accountant or financial adviser who gave you the MS Word document is liable for the loss.

Is the Division 7A Loan agreement for single use?

Q: Is the Legal Consolidated Div7A Loan Deed a single-use template, or is there an accountant’s version that can be reused for clients in my practice?

A: Legal Consolidated does not sell templates. When you build a document on our website, Legal Consolidated is responsible for the document. They are finished with legal documents. Each comes with a cover letter confirming that Legal Consolidated prepared the document. That protects the accountant. If you reuse a Div7A template, you are engaging in legal work. And that is illegal.

3. Out-of-date ATO material contaminates a Division 7A Loan Agreement

Some Division 7A Loan Agreements sold on non-law firm websites still refer to:

-

-

- Law Administration Practice Statement PS LA 2007/20; and

- Taxation Determination TD 2018/14.

-

PS LA 2007/20 is withdrawn. TD 2018/14 set the benchmark interest rate only for the 2018–19 income year. Neither belongs in a Division 7A Loan Deed. Out-of-date ATO material gives the ATO another attack point.

4. A genuine Division 7A Loan Deed needs an acceleration clause

An acceleration clause makes the whole debt immediately payable after the borrower defaults. Banks insist on it. A genuine commercial lender does not sit politely while the borrower breaches the deed. Without an acceleration clause, the loan is commercially weak and hands the ATO another attack point. We agree with the ATO on this one.

Why the ATO attacks non-commercial Division 7A loans

The ATO’s position is that a Div 7A loan must be on a genuine, arm’s-length commercial basis. Otherwise, it is a disguised distribution of profits rather than a loan. A loan agreement without a strong penalty for default is not a commercial agreement. A real lender, like a bank, never tolerates non-payment without severe consequences.

Section 109N requirements for a Division 7A Loan Agreement and the auditor’s checklist

A complying loan agreement must meet the minimum standards in section 109N of the Income Tax Assessment Act 1936 (Cth). This includes a written agreement, a maximum term, and a minimum interest rate. However, experienced ATO auditors operate with a checklist that goes beyond these bare minimums. They actively test the commerciality of the agreement.

Build a commercially robust Div7A Deed

Many cheap templates, especially from non-law firm websites pretending to be a law firm, fail this test. They are missing essential commercial clauses.

When you build a Division 7A Loan Deed on our law firm’s website, you get a commercially robust deed. Our lawyers draft the document to include these essential clauses. This hardens your loan agreement against this specific ATO attack point.

See an acceleration clause in our Sample Div 7A Deed above.

5. Hard-coded legislation makes a Division 7A Loan Agreement brittle

Division 7A of the Income Tax Assessment Act 1936 (Cth) is designed to stop private companies distributing profits tax-free to shareholders and associates through payments, loans, forgiven debts and the use of company assets. It is not one static rule. It is interlocking machinery spread across the 1936 Act, the 1997 Act, the Taxation Administration Act 1953 (Cth), regulations and ATO material.

Some Division 7A Loan Agreements hard-code s 109E(5), a particular repayment formula, a fixed benchmark interest rate or an old ATO ruling. Referring to s 109E(5) is not necessarily wrong today. The drafting fault is assuming that today’s subsection number and wording will survive a seven-year loan unchanged.

Parliament amends, re-enacts, rewrites and replaces provisions. The ATO publishes a benchmark interest rate for each income year. A brittle agreement can end up pointing to a dead section, an old formula or a year-specific ATO determination. Yesterday’s drafting then becomes tomorrow’s ATO attack point.

The Legal Consolidated Division 7A Loan Deed is built differently. Its definition of “Income Tax Law” includes the Income Tax Assessment Act 1936 (Cth), the Income Tax Assessment Act 1997 (Cth), the Taxation Administration Act 1953 (Cth), related legislation and regulations made under those Acts from time to time.

Clause 1.6 of our Div 7A Deed treats a reference to an Act or provision as including that Act or provision as amended, re-enacted, rewritten or replaced from time to time. Clause 1.9 also directs attention to binding rulings issued by the Commissioner when interpreting the tax law. The deed moves with the law. It does not fossilise on the day it is signed.

The deed also defines the applicable interest rate by reference to the statutory benchmark interest rate for the relevant income year. The rate moves automatically. You do not build a new deed merely because the benchmark percentage changes. Your accountant still applies the correct rate and calculates the interest and minimum yearly repayment each year.

6. Company guarantees: a genuine Division 7A Loan Deed matters

Taxation Determination TD 2025/6 confirms the breadth of the ATO’s attack. The guaranteed lender can be a bank, public company or any other entity. It does not need to be another private company.

A company guarantee is not automatically a Division 7A problem. Section 109U of the Income Tax Assessment Act 1936 (Cth) applies only when all four conditions are present:

-

-

- a private company guarantees a loan made by another entity;

- a reasonable person concludes that the guarantee was given solely or mainly as part of an arrangement involving a payment or loan to a shareholder or associate;

- an interposed private company makes that payment or loan; and

- the payment or loan exceeds the interposed private company’s distributable surplus after the statutory adjustments.

-

Taxpayer Alert TA 2024/2 identifies the structure the ATO is hunting. A profitable company guarantees a bank loan to a related company with little or no distributable surplus. The related company then funnels the money to the profitable company’s shareholders or associates. The bank sits in the middle. The ATO looks through it.

But the ATO also supports our position. It says it will not have cause to devote section 109U compliance resources where there is evidence of a genuine section 109N complying loan agreement. The ATO wants to see the genuine loan, not merely a convenient label in the accounts.

The Legal Consolidated Division 7A Loan Deed provides that written legal machinery. It must be signed on time and govern the actual advances. It is protective machinery, not camouflage. It does not turn a contrived guarantee arrangement into a genuine loan.

Where a private company guarantees a bank or group loan and money reaches a shareholder or associate, ask your accountant and lawyer to review the whole arrangement before the money moves.

Does an unpaid present entitlement require a Division 7A Loan Deed after Bendel?

No. Not merely because the entitlement remains unpaid.

In Commissioner of Taxation v Bendel [2026] HCA 18, [6], [72]–[74], the High Court majority held that a company does not provide financial accommodation merely because it does nothing to collect an unpaid present entitlement. Division 7A requires the company to do something that transfers value. Mere inactivity is not a loan.

The ATO has now accepted the result. Which is very good of them! Its Decision Impact Statement confirms that an unpaid present entitlement, without more, is not a Division 7A loan. Taxation Determination TD 2022/11 records the ATO view rejected by the High Court. It is no longer a drafting standard for a Division 7A Loan Deed.

But Bendel is not a free pass. It killed one ATO argument. It did not kill Division 7A. Division 7A may still apply if:

- the unpaid present entitlement is later converted into or satisfied by an actual loan;

- the trustee makes a payment or loan to, or forgives a debt of, a shareholder or associate and Subdivision EA applies; or

- section 100A or Part IVA applies to the wider arrangement.

Your accountant first determines whether the arrangement involves an actual Division 7A loan. If it does, at Legal Consolidated, you then build the written Division 7A Loan Deed for that loan. Do not build a deed merely because a company has an unpaid present entitlement. A deed documents a loan. It does not invent one.

Why did the government introduce Division 7A?

Private companies often pay tax at a lower rate than their shareholders. Without Division 7A, shareholders and associates (e.g. children and spouses) take company profits as loans, payments or forgiven debts and postpone or avoid the additional tax normally payable on a dividend.

Division 7A closes that door. It treats the benefit as an unfranked dividend, subject to the company’s distributable surplus and statutory exceptions. The accounts may call it a loan. The tax law may call it income.

Division 7A does not ban genuine loans. Section 109N stops a qualifying loan from being treated as a dividend where, before the company’s lodgment day, a written agreement sets the required maximum term and benchmark interest rate. Section 109E then requires minimum yearly repayments. At Legal Consolidated, you build the Division 7A Loan Deed that supplies that written legal machinery.

See Income Tax Assessment Act 1936 (Cth) ss 109B, 109D, 109E, 109N, 109Y.

What is the Division 7A benchmark interest rate?

The Division 7A benchmark interest rate resets each income year. Under the Income Tax Assessment Act 1936 (Cth) s 109N(2), it is tied to the bank variable housing loan interest rate last published by the Reserve Bank of Australia before the income year starts, unless the regulations prescribe another method.

The rate may rise, fall or remain unchanged. Your accountant applies the correct rate and calculates the interest and minimum yearly repayment. The ATO publishes the current and historical Division 7A benchmark interest rates.

The Legal Consolidated Division 7A Loan Deed does not hard-code today’s percentage. It adopts the statutory benchmark interest rate from time to time. The rate moves. The deed survives.

Your accountant is then able to apply the current rate and calculate the interest and minimum yearly repayment for each income year.

Can I use company money for personal expenses?

No. Company money is not your money. The company is a separate legal person. Even if you own every share, its bank account is not your wallet.

Subject to statutory exclusions and the company’s distributable surplus, Division 7A may treat a private payment, loan, forgiven debt or private use of a company asset as an unfranked dividend. See Income Tax Assessment Act 1936 (Cth) ss 109C, 109CA, 109D, 109F, 109Y. The final tax treatment depends on the facts and other tax rules, including fringe benefits tax.

A Division 7A Loan Deed is not a magic eraser. It helps only where the transaction is a genuine loan, or an amount is validly converted into a loan before the company’s lodgment day. It cannot simply relabel every salary, dividend, fringe benefit, private payment or use of an asset as a loan.

Is money taken from a company a loan, salary or dividend?

Every payment or benefit needs its correct legal and tax character. Depending on the facts, company money received or used by a shareholder or associate may be:

- salary, wages or director fees;

- a dividend;

- reimbursement of a genuine company expense;

- a fringe benefit;

- repayment of money the company already owes;

- a genuine loan; or

- an amount Division 7A treats as an unfranked dividend.

The label in the accounting software is not decisive. A journal entry records a transaction that has already happened. It does not create a salary, dividend, repayment or loan. The ATO tells private companies to keep records explaining transactions with shareholders, associates and related trusts.

Your accountant determines the correct category and tax reporting. If the transaction is a genuine loan requiring section 109N compliance, at Legal Consolidated you build the Division 7A Loan Deed. The deed documents the genuine loan. It does not turn a bookkeeping label into legal reality.

What does a Legal Consolidated Division 7A Loan Deed cover?

The deed legally documents: a genuine loan from a company to one borrower. It provides the written commercial framework for advances, interest, repayments, default and recovery.

The Legal Consolidated deed adopts the ATO statutory benchmark interest rate from time to time. It also contains minimum yearly repayment, default and acceleration machinery. In contrast a non-law firm website provides a template often lacking these control levers.

The deed does not turn a private payment, use of a company asset, debt forgiveness, salary, dividend, fringe benefit or unpaid present entitlement into a loan. Your accountant first determines that the transaction is an actual loan. At Legal Consolidated, you then build the deed for that loan relationship.

Build a separate Division 7A Loan Deed for each borrower

Do not use one Division 7A Loan Deed for the whole family group. Each borrower has a separate legal relationship with the company. Each borrower needs a separate deed with the company.

For example, separate deeds are required where the company lends money or provides financial accommodation to:

- a shareholder;

- the shareholder’s spouse;

- an adult child;

- the trustee of a Family Trust;

- a related company or bucket company; or

- another associate of a shareholder.

A human and a company are both legal persons. However, a Family Trust is not a legal person. The borrower is the trustee in its capacity as trustee of the Family Trust. Name the trustee correctly in the deed.

Sign each deed before the first advance. Keep the signed deed with the company records. Maintain a separate loan account for each borrower.

Can a Company Constitution replace a Division 7A Loan Deed?

No. In Botella and Commissioner of Taxation (Taxation and business) [2026] ARTA 604, the company relied on Division 7A loan terms contained in its Constitution. The Tribunal held that this was not enough.

The loans were advanced and recorded through book entries. However, they were not made under a separate written agreement between the company and the shareholder. The constitutional clause could not turn loans made by conduct into loans made under a written agreement.

Section 109N of the Income Tax Assessment Act 1936 (Cth) requires the agreement under which the loan is made to be in writing before the company’s lodgment day. A Company Constitution does not, by itself, record a separate bilateral agreement governing the actual advances.

A book entry records a transaction. It does not create the agreement.

Do not rely on Division 7A terms contained in a Company Constitution. Build a separate Division 7A Loan Deed between the company and each borrower. The safest course is to sign the Deed before the first advance and keep a written record of every advance made under it.

![Botella and Commissioner of Taxation (Taxation and business) [2026] ARTA 604 Div 7A vs Constitution](https://legalconsolidated.com.au/wp-content/uploads/Botella-and-Commissioner-of-Taxation-Taxation-and-business-2026-ARTA-604-Div-7A-vs-Constitution.png)

Is a Division 7A Loan Agreement a revolving line of credit and cover multiple advances?

Yes. The Legal Consolidated Division 7A Loan Deed is a revolving loan facility between one company and one borrower. It covers multiple advances and repayments. You do not need a new deed each financial year, provided the parties remain the same and the deed remains in force.

The deed does not need to state a fixed loan amount. Taxation Determination TD 2008/8 [35] accepts that the amount drawn down does not need to appear in the formal written agreement.

However, before the company’s lodgment day, there must be written evidence that each payment or crediting was made under the revolving loan facility.

Botella [82] shows the danger. The advances and book entries were not sufficiently connected to the written terms in the Company Constitution.

For each advance, keep a written record showing:

- the date;

- the amount;

- the lending company;

- the borrower; and

- the date of the Division 7A Loan Deed governing the advance.

The loan account should record:

Advance made under the Division 7A Loan Deed dated [insert date].

A journal entry or minute merely records a transaction. It does not create the transaction or the loan agreement. Do not rely on a year-end journal entry alone.

At the end of each financial year, your accountant calculates the outstanding balance, benchmark interest and minimum yearly repayment.

Can a journal entry make a Division 7A minimum yearly repayment?

A journal entry records a transaction. It does not create one. Writing ‘dividend set-off against Division 7A loan’ into the accounts after 30 June does not make a repayment happen by 30 June.

Cash is the simplest and safest repayment. However, a genuine mutual set-off can discharge both debts without money moving through bank accounts. This is the principle in Re Harmony and Montague Tin and Copper Mining Co (Spargo’s Case) (1873) LR 8 Ch App 407, 414.

For a mutual set-off to work:

- the company and the borrower must owe each other presently due and certain amounts;

- the same legal parties must appear on both sides;

- the dividend or other company debt must validly exist before 30 June under the company’s Constitution and the Corporations Act 2001 (Cth) ss 254T–254V; and

- the parties must agree to the set-off before 30 June and keep written records proving that it happened.

A dividend owed to a shareholder does not, by itself, repay a separate debt owed by a spouse, Family Trust or other associate. The parties are different.

Do not repay the loan and then borrow the same or a similar amount from the company. Section 109R may disregard that repayment. TD 2025/5 confirms that the rule can also apply through interposed entities and notional loans.

At Legal Consolidated, you build the Division 7A Loan Deed on our Australian law firm’s website. Legal Consolidated provides the finished legal document under the law firm’s letterhead. The deed legally documents the loan.

Are the accounts of a debtor company enough to create an acknowledgment by a debtor? VL Finance Pty Ltd v Legudi

Q: The ATO has concerns regarding Deeds and ‘journal entries’. But are the accounts of a debtor company enough to create an acknowledgment by a debtor? Surely, the annual company return of the creditor company is sufficient to create the relevant acknowledgment?

A: You are playing with fire here. I am not sure why you are looking for trouble.

Your argument fails under VL Finance Pty Ltd v Legud [2003] VSC 57. Your question about the annual company returns of the creditor company being enough to create the acknowledgment is rejected by the Court. This is the case, even though:

- The returns are signed by the directors, who are the actual debtors!

- And the accounts identified the debts.

The annual returns are not:

A statement ‘made’ by the directors in their capacity as debtors to the company in its capacity as the creditor. As your accountant will tell you, the annual return is merely a statement ‘by’ the company.

One of my students, who helped with the research for this article, dug up the case of Lonsdale Sand & Metal v FCT 38 ATR 384. In this case, the statement in the accounts of a debtor company is accepted as evidence of an acknowledgment by a debtor. However, this case relates to the old Section 108 loans, which predate Div7A. I would not rely on this case.

My family trust has no ‘spare’ cash. How can it pay back the money it owes the bucket company?

Q: I distribute money to my bucket company. This is so that we pay the lower corporate tax rate.

However, how will the discretionary trust ever be able to repay the loan if all income (including capital gain) must be distributed every year?

How can I repay the money if I only distribute it to a bucket company? If I were distributing also to human beneficiaries, I would get them to sign Deeds of Debt Forgiveness. This would free up cash.

A: The terror of Division 7A was introduced in 1997. Since then, my own Family Trust has never been distributed to our bucket company. It is too complex. I would rather pay the tax.

Your question reflects the complexity. First, you need to distribute the trust income and realised capital gains. Otherwise, the trustee of the Family Trust pays tax at the highest human marginal tax rate. Div 7A is designed to prevent you from permanently taking advantage of the lower constant company tax rate.

(You only pay capital gains if you dispose of an asset. If your family trust has shares in BHP and they triple in price, but you do not sell them, then you do not pay capital gains. You trigger the CGT liability only when you sell or dispose of the BHP shares.)

With a Div 7A Loan, you pay back one-seventh of the debt plus the statutory interest rate each financial year.

You claim that your Family Trust has no ready cash lying around to pay that 1/7th of the debt. Well, like all of us, you have to pay your debts. Sell Family Trust assets. The Family Trust can borrow. Or the Family Trust can declare insolvency, allowing the bucket company to sell the Family Trust assets to try to claw back the debt.

You mention that if you distribute to human beneficiaries, they can just forgive the debt. I agree. But I do not see how that frees up any ready cash. You were not going to hand over any cash to them anyway!

Can a sub-trust replace a Division 7A Loan Deed?

Q: Why not set aside the money the Family Trust owes the bucket company on a sub-trust? The money is then held solely for the bucket company. Surely that satisfies Division 7A without a Division 7A Loan Deed?

A: The old sub-trust shortcut is dead. The sub-trust itself is not. That distinction matters.

Under the ATO’s view in Taxation Determination TD 2022/11, [7]–[12], a bucket company provides financial accommodation when it knows it can demand payment of an unpaid present entitlement but allows the Family Trust to keep using the money. This is a loan under s 109D(3)(b) of the Income Tax Assessment Act 1936 (Cth).

Moving the number into an account labelled ‘sub-trust’ does not change the commercial reality. A label is not a force field.

A genuine sub-trust is different. The amount is removed from the assets of the main Family Trust and held exclusively for the bucket company. The bucket company receives the sole benefit and can call for payment of the whole sub-trust fund.

The ATO’s example uses a separate bank sub-account. The money is not mixed with the Family Trust’s money. The Family Trust cannot use it, pledge it as security or offset it against another loan. In those circumstances, merely leaving the money on sub-trust does not provide financial accommodation: TD 2022/11, [13]–[14], [32]–[38].

However, the moment the Family Trust, a shareholder or an associate uses or benefits from the sub-trust money with the bucket company’s knowledge, the position changes. The bucket company provides financial accommodation. Paying a commercial rate of interest does not save the arrangement: TD 2022/11, [15]–[16], [39]–[45].

The sub-trust that avoids this Division 7A problem is therefore the sub-trust the Family Trust cannot use. That rather spoils the reason most people wanted one.

TD 2022/11 applies to trust entitlements arising on or after 1 July 2022. The old Taxation Ruling TR 2010/3 and Practice Statement PS LA 2010/4 were withdrawn for those new entitlements. The ATO continues its former compliance approach for qualifying entitlements arising on or before 30 June 2022. Practical Compliance Guideline PCG 2017/13 remains relevant to some old seven-year and ten-year sub-trust arrangements. It is not a safe harbour for new entitlements.

Legal Consolidated has never built sub-trust arrangements. We have always considered the investment-back versions brittle, complicated and litigation bait.

If the Family Trust intends to retain and use the bucket company’s money, stop dressing the debt as a sub-trust. Before the bucket company’s lodgment day, either pay the entitlement or place the financial accommodation under a complying Division 7A loan.

At Legal Consolidated, you build the Division 7A Loan Deed for that genuine loan relationship. Legal Consolidated then provides the finished legal document under the Australian law firm’s letterhead. Your accountant determines the amount of the entitlement and the applicable tax treatment.

Your new, correctly drafted Div7A Loan Deed operates from the day you sign it. It applies only to new loans and advances made in that time period and, of course, future loans by the company.

Can a new Division 7A Loan Deed fix an old faulty agreement?

Q: My client bought a Division 7A Loan Agreement from a non-law firm website. I telephoned the website. The seller agreed that the document was faulty and apologised.

She explained that she was reselling an old template prepared by a commercial lawyer who did not practise in tax. To add insult to injury, the lawyer had retired!

The document had travelled from a retired commercial lawyer, through a non-law firm website and into my client’s file. It had more handlers than legal supervision.

The faulty agreement is dated 30 June last year. If my client builds a correct Legal Consolidated Division 7A Loan Deed one year later, does that repair the problem?

A: Possibly. But stop counting anniversaries. Find the company’s lodgment day.

Under the Income Tax Assessment Act 1936 (Cth) ss 109D(6), 109N(1), the relevant deadline is the company’s lodgment day for the income year in which the loan was made. This is the earlier of the company’s actual lodgment date and its due date for lodgment.

The first anniversary of the loan tells you nothing. Division 7A does not celebrate birthdays.

1. Before the company’s lodgment day

The ATO accepts that a written loan document may be completed after the advances were made—even after the end of the income year—provided the essential elements are in writing before the company’s lodgment day.

The ATO gives an example involving several advances recorded in a shareholder’s drawings account. A later written agreement, signed before the lodgment day and properly linked to those advances, satisfied the written-agreement requirement: Australian Taxation Office, Taxation Determination TD 2008/8, paras 4, 6–11, 30–36.

Therefore, if the lodgment day has not passed, there may still be time to document the existing advances properly. The deed must identify or link to the advances and record the amount, repayment obligation, interest and loan term.

Sign the deed using the actual signing date. Never backdate it. A defective document is one problem. A false signing date is a fresh problem wearing a tie.

2. After the company’s lodgment day

Once the lodgment day has passed, a new deed cannot travel back through time and satisfy a requirement that was missed for the earlier income year.

The new deed may protect genuinely new advances. However, the tax treatment of the existing balance and any proposed refinancing, replacement or restatement must be reviewed separately.

A new deed does not automatically “override” an earlier agreement. The documents must expressly state whether the old arrangement is replaced, restated or continues alongside the new deed. Legal documents do not fight to the death after everyone leaves the room.

Can the ATO disregard an honest Division 7A mistake?

Q: My accountant calculated the minimum yearly repayment incorrectly. The repayment was $100 short. Does the entire Division 7A loan become an unfranked dividend?

A: No. If the loan otherwise complies with Division 7A, the deemed dividend is generally the amount of the repayment shortfall.

Under the Income Tax Assessment Act 1936 (Cth) s 109E(2), a $100 minimum yearly repayment shortfall produces a $100 deemed dividend, subject to the company’s distributable surplus. It does not turn the entire outstanding loan into a dividend.

Division 7A has enough genuine traps. We do not need to invent a larger one.

This is different from failing to place the original loan under a complying written agreement before the company’s lodgment day. That failure may expose the unpaid loan amount to section 109D. A $100 calculation error and a missing deed are different species of trouble.

What relief is available for an honest Division 7A mistake?

Under the Income Tax Assessment Act 1936 (Cth) s 109RB, the Commissioner may disregard a Division 7A result or allow a deemed dividend to be franked where the result arose because of an honest mistake or inadvertent omission.

The word is “may”. Relief is discretionary. Honesty opens the door. It does not force the Commissioner to invite you inside.

The Commissioner considers:

- the circumstances that caused the mistake or omission;

- what corrective action was taken;

- how quickly that action was taken;

- whether Division 7A has applied previously to the parties; and

- any other relevant matter.

The Commissioner may also impose conditions. These include requiring payments to the company or requiring specified Division 7A steps to be completed within a fixed time.

The ATO explains its approach in Australian Taxation Office, Practice Statement Law Administration PS LA 2011/29 and Taxation Ruling TR 2010/8, paras 10–13.

Is relying on my accountant enough to prove an honest mistake for the Div7A?

Merely saying, “My accountant handles all that”, does not prove an honest mistake.

The taxpayer must explain what happened, who made the mistake and why the mistake caused Division 7A to operate. Contemporaneous emails, calculations, financial records and advice help. A shrug does not.

Your accountant determines the minimum yearly repayment, maintains the loan balance and advises on the tax consequences. If relief is required, your accountant prepares the facts and calculations supporting the application.

The Legal Consolidated Division 7A Loan Deed supplies the written legal framework. It adopts the statutory benchmark interest rate from time to time and contains repayment, default, acceleration and recovery machinery.

The deed does not sit up on 30 June, open the ledger and calculate the repayment. Your accountant does that.

Section 109RB is a fire escape. It is not the front entrance. Proper documentation and yearly administration remain cheaper, calmer and far more reliable.

Is a genuine commercial loan exempt from Division 7A?

No. Calling a loan “genuine and commercial” does not, by itself, switch off Division 7A.

The Income Tax Assessment Act 1936 (Cth) contains specific exceptions. For example, s 109M protects a loan made in the ordinary course of the private company’s business on the usual terms on which that company makes similar loans to parties at arm’s length.

That is a narrow test. A family trading company does not become a bank merely because its director writes “commercial loan” in the ledger.

Other statutory exceptions cover specific payments and loans. These include genuine debts owed by the company, certain inter-company loans, amounts otherwise included in assessable income and loans satisfying section 109N: Income Tax Assessment Act 1936 (Cth) ss 109J–109N.

There is also no general exception for an unpaid present entitlement merely because the arrangement has a genuine commercial purpose. Its treatment depends on its legal character and the particular Division 7A provisions that apply.

The Act wants a section. It is not persuaded by an adjective.

Does a Division 7A breach trigger a 100% tax penalty?

The combined tax, penalties and interest can exceed the money taken from the company.

The Division 7A punishment comes in four blows:

- the loan is treated as an unfranked dividend;

- the shareholder receives no credit for company tax already paid;

- penalties and interest may be added; and

- the shareholder may still owe the company every dollar borrowed.

The ATO taxes you as though the company gave you the money. Company law requires you to pay it back if the company is insolvent.

Example of a Div7A breach

Assume a company lends its shareholder $100,000. The loan is not repaid, there is no complying s 109N agreement before the company’s lodgment day and the company has sufficient distributable surplus. Section 109D of the Income Tax Assessment Act 1936 (Cth) treats the $100,000 as an unfranked dividend. At the 45% top marginal rate plus the 2% Medicare levy, the personal tax bill reaches $47,000. The legal debt does not disappear. The shareholder may owe $47,000 to the ATO and still owe $100,000 to the company. The boat may be gone. The tax bill and company debt remain.

If the deemed dividend was omitted from the tax return, the ATO may also impose a shortfall penalty. The base penalty rates are commonly 25%, 50% or 75%, depending on the taxpayer’s conduct. A 25% penalty on the $47,000 tax shortfall adds $11,750. Interest sits on top.

How does the combined punishment reach 100%?

If a company paying 25% tax retains $100,000, it first earned about $133,333 and paid about $33,333 in company tax. Add the $47,000 personal tax and a 25% penalty of $11,750. The combined cash cost reaches about $92,083 before interest. If the company pays tax at 30%, it paid about $42,857 to retain the same $100,000. Add the personal tax and penalty. The combined cost reaches about $101,607 before interest. The company tax is not another Division 7A assessment. The sting is that the deemed dividend is unfranked. The shareholder receives no credit for tax already paid by the company.

This is why Division 7A is described as an almost 100% tax punishment. It is not a statutory rate. It is the combined economic damage.

Your accountant determines the actual tax consequences. Where the transaction is a genuine loan and s 109N is available, at Legal Consolidated you build the Division 7A Loan Deed before the company’s lodgment day. The deed is protective machinery. It is cheaper to put it in place before the ATO arrives.

What documents do you receive with a Legal Consolidated Division 7A Loan Deed?

Within 2 minutes of finishing the building process, Legal Consolidated emails you:

- the finished Division 7A Loan Deed tailored to your answers;

- company minutes approving the loan and deed; and

- a letter on our Australian law firm’s letterhead confirming that Legal Consolidated prepared the legal documents.

This is not a reusable template from a non-law firm website. You build the deed for one named company and one named borrower. Legal Consolidated provides the finished legal documents and takes responsibility for the legal drafting.

Keep the three documents together with the company records. Give a copy to the company’s accountant. As per our cover letter, sign the deed before the first advance or, at the latest, before the company’s lodgment day.

Further reading about Division 7A Loan agreements:

ATO says ‘loans’ from a company were not loans

Business Structures for Personal Services Income, tax and asset protection

Family Trust v Division 7A Loan Deed

- Family Trust Deed – watch the free training course

- Family Trust Updates:

- Everything – Appointor, Trustee & Deed Update

- Deed ONLY – only update the Deed for tax

- Guardian and Appointor – only update the Guardian & Appointor

- Change the Trustee – change human Trustees and Company Trustees

- Is the company a Trustee of a Family Trust, only for asset protection?

- Bucket Company for Family Trust – tax advantages of a corporate beneficiary

Unit trust vs Division 7A Loan Deed

- Unit Trust

- Unit Trust Vesting Deed – wind up your Unit Trust

- Change Unit Trust Trustee – replace the trustee of your Unit Trust

- Company as Trustee of Unit Trust – how to build a company designed to be a trustee of a Unit Trust

Corporate Structures and Division 7A Loan Deed

- Partnership Agreement – but what about joint liability?

- Incorporate an Australian Company – best practice with the Constitution

- Upgrade the old Company Constitution – this is why

- Replace lost Company Constitution – about to get an ATO Audit?

Service trust and Independent Contractors Agreements

- Independent Contractor Agreement – make sure the person is NOT an employee

- Service Trust Agreement – operate a second business to move income and wealth

- Law firm Service Trust Agreement – how a law firm runs the back end of its practice

- Medical Doctor Service Trust Agreement – complies with all State rules, including New South Wales

- Dentist Service Trust Agreement – how dentists move income to their family

- Engineering Service Trust Agreement – commonly, engineers set up the wrong structure

- Accountants Service Trust Agreement – complies with ATO’s new view on the Phillips case