What is a Northern Territory Advance Personal Plan (APP)?

The Northern Territory does not give you a clean, standalone “Enduring Power of Attorney” in the way most other jurisdictions do. Instead, since 2014, it operates under the Advance Personal Planning Act 2013 (NT). That Act created a single instrument: the Advance Personal Plan (APP).

That is the theory.

In practice, if you follow that theory blindly, you will create delay, confusion, and disclosure problems every time the document is used.

What the NT APP law actually says about economic powers

Under the NT Act, you appoint a ‘decision maker’ (attorney) for financial matters and a decision maker for personal matters in the same document.

Section 4 defines a “decision maker” broadly. Section 13 then allows appointment for:

- financial matters; and

- personal matters (which include health care and lifestyle).

The Act states:

“A person may, by an advance personal plan, appoint one or more decision makers for financial matters and personal matters.”

— Advance Personal Planning Act 2013 (NT) s 13

Financial matters are also defined widely:

“Financial matter means a matter relating to the person’s property or financial affairs…”

— Advance Personal Planning Act 2013 (NT) s 3

That includes:

- bank accounts

- real estate

- debts

- investments

So yes, legally, one document can do everything.

That is exactly the problem.

The Legal Consolidated position: split the NT Advance Personal Plan, or suffer

At Legal Consolidated, we split the NT APP into:

- financial only

- Medical / Personal Plan (health and lifestyle) only

The NT legislation allows a combined document. But it does not force you to use one.

And if you do combine them, expect friction.

Why splitting the NT Advance Person Plan is best practical approach

1. Privacy is not optional

If your decision maker (attorney) goes to a bank, the bank needs to see financial authority.

They do not need to see:

- your resuscitation instructions

- your palliative care views

- your nursing home preferences

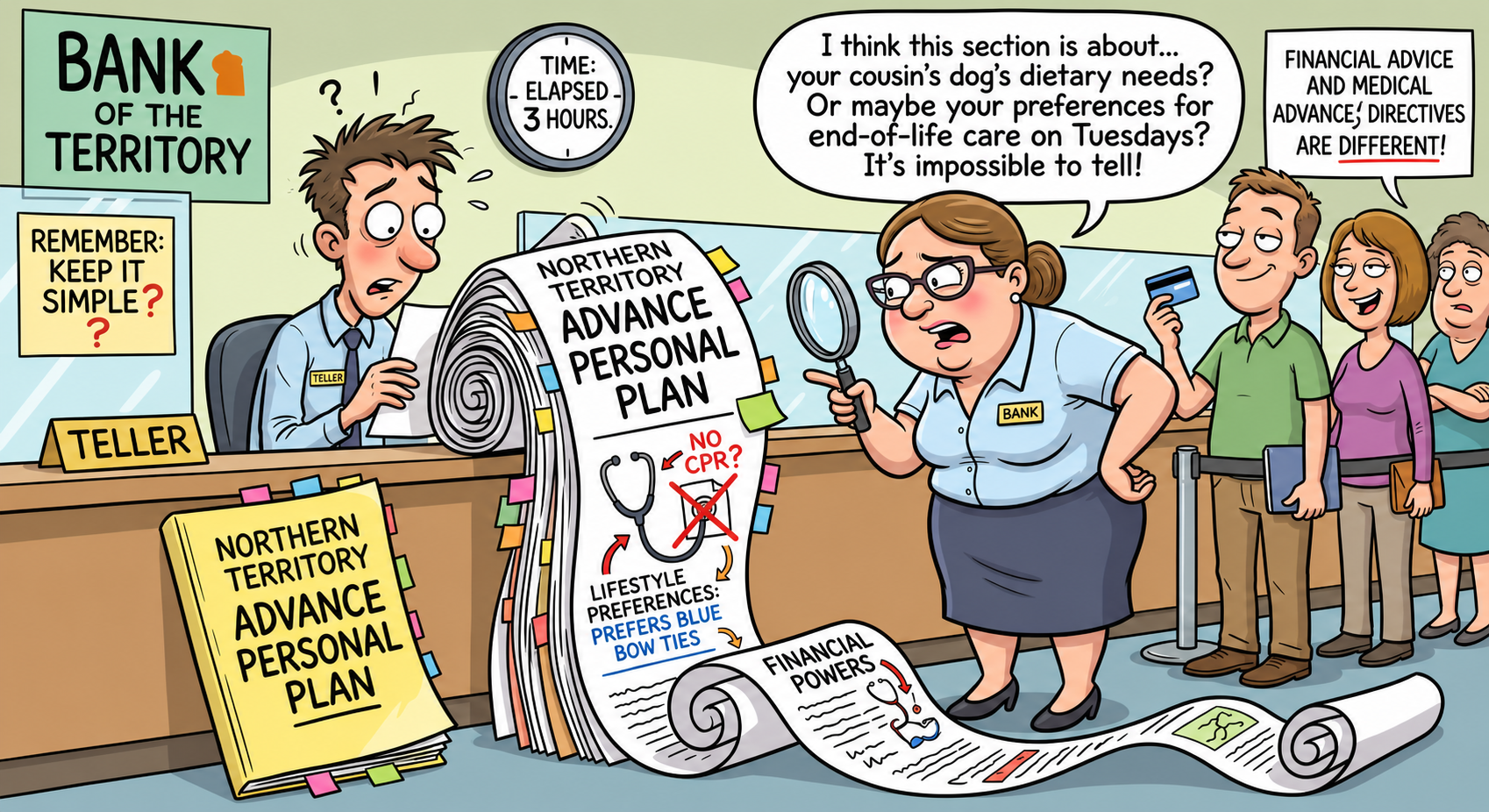

Yet under a single APP, all of that sits in one document.

You hand over everything. It causes delays as the bank gets confused.

2. Institutions do not read the NT POA properly

Banks, land titles offices, and other institutions want simple authority.

Give them a 25-page APP covering medical and lifestyle issues, and you get:

- delays

- refusals

- “legal team review required”

That leads to one outcome: your attorney cannot act when needed.

3. Operational failure is common

In practice, combined documents lead to:

- clerks misunderstanding authority

- unnecessary escalations

- requests for certified copies of irrelevant sections

That is not a theory. That is a daily experience that we have found, having worked in this area across Australia since 1988.

Do not mix a finance NT Advance Personal Plan with a lifestyle/medical APP. Keep your financial affairs strictly separate from your health and end-of-life directives to avoid the administrative nightmare!

What your Northern Territory Enduring POA actually does

Your financial Advance Personal Plan is an economic instrument.

It allows your decision maker to:

- operate bank accounts

- buy and sell real estate

- pay debts

- manage investments

The legal test is simple. The decision maker must act in your best interests.

The Act is blunt:

“A decision maker must exercise decision-making authority in the best interests of the represented person.”

— Advance Personal Planning Act 2013 (NT) s 22

Limits on a Northern Territory Advanced Personal Plan

Even with broad financial authority, there are hard limits.

Your decision maker cannot:

- vote in elections

- make or change your Will

- create another power of attorney for you

- make personal or medical decisions (if you split documents)

Can my NT decision maker make a Will for me?

The law is settled.

In Re Edwards; Application of the Public Trustee, the Court confirmed that testamentary power is personal:

“The making of a will is an exercise of a personal discretion which cannot be delegated.”

Your attorney cannot step into that role. Ever.

SMSFs and trusts: do not get this wrong

Your POA does not automatically make your attorney a trustee.

This is where people get into serious trouble.

Under the Superannuation Industry (Supervision) Act 1993 (Cth):

“Each trustee of the fund must be an individual who is a member of the fund…”

— SIS Act s 17A(1)

There is a narrow exception allowing an attorney to act, but only if:

- the trust deed allows it; and

- the appointment is properly documented

If you ignore this, your SMSF becomes non-compliant. That leads to tax penalties.

How the NT POA works in real life

Example 1 – Bank transaction

Your attorney attends the bank.

They produce:

- your account details

- your Northern Territory Enduring POA

The bank officer hesitates. That is normal.

A competent manager will recognise the legal effect:

Your attorney stands in your shoes.

They can do anything you could legally do with that account.

The bank will:

- take a copy

- verify identity

- process the transaction

If they ask for the original, refuse. Provide a certified copy. Keep control of the original.

Example 2 – Signing documents with a NT POA

Your attorney signs a lease for you.

The correct execution block is:

Signed as attorney for [Name] under a Northern Territory Enduring Power of Attorney dated [Date]

That binds you fully.

There is no “I did not see it” argument later.

Final position

The Northern Territory system is legally neat and practically flawed.

One document for everything sounds efficient. It is not.

If you want:

then split your documents.

Financial authority in one. Medical authority in another.

Anything else leads to legal complications.

Money POAs: NSW, VIC, QLD, WA, SA, TAS, ACT & NT

Money POAs: NSW, VIC, QLD, WA, SA, TAS, ACT & NT